|

市場調查報告書

商品編碼

1959661

飛機防雷市場機會、成長要素、產業趨勢分析及2026年至2035年預測Aircraft Lightning Protection Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球飛機防雷市場價值 49 億美元,預計到 2035 年將達到 93 億美元,年複合成長率為 6.8%。

市場成長的驅動力來自飛機產量的增加、全球航空運輸量的擴張以及需要先進安全整合技術的新一代飛機平台的推出。隨著商用飛機機隊的擴張和旅行需求的增強,飛機製造商正致力於提升飛行安全系統,包括防雷技術。更嚴格的法規結構和認證標準進一步加速了能夠承受雷擊和突波的高可靠性組件的普及應用。各公司正投資研發低容量、高耐久性的暫態電壓抑制系統,以保護精密航空電子設備及結構元件。現代機身結構中先進複合材料的應用也增加了對專用保護系統的需求,以有效應對放電現象。飛機防雷涉及導電材料、連接網路和保護技術的整合。這些設計旨在安全地引導雷電能量,維持結構完整性,保護電氣架構,並確保飛機的持續適航性和運作安全性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 49億美元 |

| 預測金額 | 93億美元 |

| 複合年成長率 | 6.8% |

預計到2025年,直接效應防護產品市場規模將達到18億美元,並在2026年至2035年間以5.8%的複合年成長率成長。隨著飛機製造商擴大採用複合材料機身,對增強型屏蔽層的需求也隨之成長,以保護飛機免受雷擊的直接物理影響,這一細分市場正日益受到關注。直接效應防護解決方案旨在防止高能量放電造成的表面損傷、結構弱化和材料劣化。這些系統透過最大限度地減少維修頻率和因檢查造成的停機時間,有助於提高飛機的可靠性和全生命週期成本效益。日益嚴格的防雷認證要求也進一步推動了對先進結構防護技術的需求。

到2025年,飛機領域將佔據46.9%的市場佔有率,反映出固定翼飛機平台對防雷系統的日益普及。隨著飛機設計中複合材料的使用增加以及電子系統日益複雜,全面防護直接和間接雷擊至關重要。整合式防護架構將結構屏蔽與先進的接地和突波抑制機制結合,以確保系統級安全。飛機數量的成長、飛機使用壽命的延長以及技術的不斷升級,都強化了民航領域對防雷解決方案的長期需求。

預計到2025年,北美飛機防雷市場將佔據39.5%的市場佔有率,並繼續保持其作為主要區域市場的地位。該地區受益於成熟的航太製造生態系統和對先進飛機生產的重視。日益增多的、高度依賴複合材料的飛機平台推動了對輕質、高導電性防護材料的需求。法律規範和創新主導的發展持續影響競爭格局,製造商優先考慮重量最佳化、性能可靠性和符合嚴格的安全標準。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 飛機產量增加以及防雷技術的研究與開發

- 對低成本航空公司的需求不斷成長,以及經濟高效解決方案的開發。

- 航空客運量和國防飛機數量不斷增加

- 對單通道飛機的需求增加以及基礎設施建設的進展

- 產業潛在風險與挑戰

- 飛機製造中安裝防雷設備高成本。

- 維修工程的複雜性

- 市場機遇

- 大量使用複合材料的飛機結構的發展

- 售後改裝與MRO主導的升級

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 供應鏈韌性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 併購和策略聯盟的趨勢

- 風險評估與管理

- 重大合約採購範例(2022-2025 年)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年重大發展

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 直接作用防護產品

- 拉伸金屬箔

- 導電網

- 分流條和撞擊端子

- 其他

- 間接效應防護產品

- 暫態電壓抑制器

- Lightning專用屏蔽連接器

- 其他

- 連接和接地產品

- 黏合帶和套頭衫

- 接地帶和匯流排

- 靜電放電芯

第6章 市場估價與預測:依車型分類,2022-2035年

- 飛機

- 民用運輸飛機

- 軍用運輸機

- 其他

- 旋翼飛機

- 民用直升機

- 政府和軍用直升機

- 無人駕駛航空器系統(UAS)

- 戰術無人機

- 載人/無人飛行器(UAV)

- 商用無人機

- 電動和混合動力飛機

- 垂直起降飛機

- 滑翔機

- 其他

第7章 市場估計與預測:依應用類型分類,2022-2035年

- 新安裝

- 改裝

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- OEM(原始設備製造商)

- 一級和二級供應商

- MRO(維修、修理和大修)

- 售後市場和維修

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- BAE Systems plc

- Honeywell International Inc.

- Collins Aerospace(Raytheon Technologies)

- Safran SA

- 按地區分類的主要企業

- 北美洲

- LORD Corporation

- Spirit AeroSystems, Inc.

- Triumph Group, Inc.

- 歐洲

- ATEC GmbH

- Meggitt PLC

- GKN Aerospace

- 亞太地區

- Elbit Systems Ltd.

- Moog Inc.

- Aero Vodochody AEROSPACE as

- 北美洲

- 特殊玩家/干擾者

- Ferrostaal GmbH

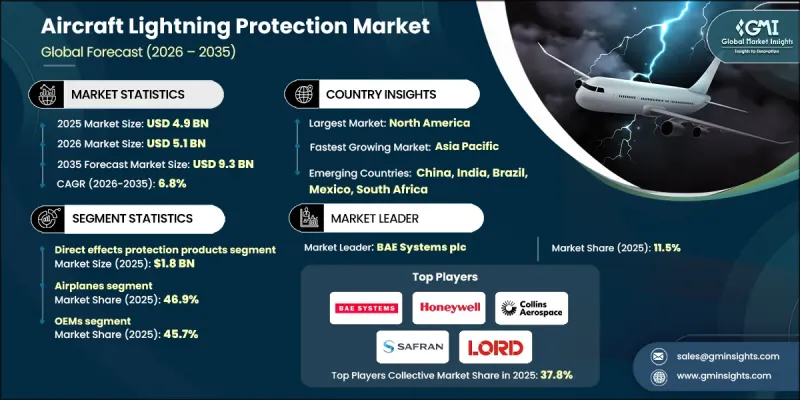

The Global Aircraft Lightning Protection Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 9.3 billion by 2035.

Market growth is fueled by rising aircraft production, increasing global air traffic, and the introduction of next-generation aircraft platforms that require advanced safety integration. As commercial fleets expand and travel demand strengthens, aircraft manufacturers are intensifying efforts to enhance onboard safety systems, including lightning protection technologies. Stricter regulatory frameworks and certification standards are further accelerating the adoption of high-reliability components capable of withstanding lightning strikes and electrical surges. Companies are investing in research and development to engineer low-capacitance, high-durability transient voltage suppression systems that safeguard sensitive avionics and structural elements. The incorporation of advanced composite materials in modern airframes has also elevated the need for specialized protection systems to manage electrical discharge effectively. Aircraft lightning protection involves the integration of conductive materials, bonding networks, and protective technologies designed to safely channel lightning energy, preserving structural integrity, protecting electrical architecture, and maintaining continuous airworthiness and operational safety.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 6.8% |

The direct effects protection products segment generated USD 1.8 billion in 2025 and is expected to grow at a CAGR of 5.8% between 2026 and 2035. This segment is gaining traction as aircraft manufacturers increasingly utilize composite airframes that require enhanced shielding from the immediate physical impact of lightning strikes. Direct effects protection solutions are engineered to prevent surface damage, structural weakening, and material degradation caused by high-energy electrical discharge. By minimizing repair frequency and inspection downtime, these systems contribute to improved fleet reliability and lifecycle cost efficiency. Rising certification requirements related to lightning strike resilience are further strengthening demand for advanced structural protection technologies.

The airplanes segment accounted for 46.9% share in 2025, reflecting widespread integration of lightning protection systems in fixed-wing aircraft platforms. As aircraft designs incorporate higher volumes of composite materials and more sophisticated electronic systems, comprehensive protection against both direct and indirect lightning effects has become essential. Integrated protection architectures combine structural shielding with advanced electrical grounding and surge suppression mechanisms to ensure complete system-level safety. Growing fleet sizes, extended service life of aircraft, and continuous technological upgrades are reinforcing long-term demand for lightning protection solutions across commercial aviation.

North America Aircraft Lightning Protection Market held 39.5% share in 2025, maintaining its position as the leading regional market. The region benefits from a well-established aerospace manufacturing ecosystem and a strong focus on advanced aircraft production. The increasing output of composite-intensive aircraft platforms has elevated demand for lightweight and highly conductive protection materials. Regulatory oversight and innovation-driven development continue to shape the competitive landscape, with manufacturers prioritizing weight optimization, performance reliability, and compliance with rigorous safety standards.

Key companies operating in the Global Aircraft Lightning Protection Market include Honeywell International Inc., BAE Systems plc, Collins Aerospace (Raytheon Technologies), Safran S.A., LORD Corporation, Spirit AeroSystems, Inc., Meggitt PLC, GKN Aerospace, Triumph Group, Inc., Elbit Systems Ltd., Moog Inc., Ferrostaal GmbH, ATEC GmbH, and Aero Vodochody AEROSPACE a.s. Companies in the Aircraft Lightning Protection Market are strengthening their competitive position through continuous technological advancement and strategic partnerships with airframe manufacturers. Investment in research and development remains a primary strategy, with firms focusing on lightweight conductive materials, advanced bonding techniques, and enhanced transient voltage suppression systems. Collaboration with OEMs during early aircraft design phases ensures system integration and long-term supply agreements. Businesses are also expanding manufacturing capabilities to meet rising aircraft production rates while maintaining strict compliance with aviation safety certifications. Portfolio diversification across direct and indirect protection systems enables companies to address evolving aircraft architecture requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Aircraft type trends

- 2.2.3 Protection type trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing aircraft production and R&D for lightning protection

- 3.2.1.2 Growing demand for low-cost carriers and development of cost-effective solutions

- 3.2.1.3 Growing air passenger traffic and defense aircrafts

- 3.2.1.4 Increasing demand for single aisle aircraft fleet coupled with infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with aircraft manufacturing set up for lightning protection

- 3.2.2.2 Complexity in retrofitting

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of composite-intensive aircraft structures

- 3.2.3.2 Aftermarket retrofitting and MRO-driven upgrades

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Supply chain resilience

- 3.11 Geopolitical analysis

- 3.12 Workforce analysis

- 3.13 Digital transformation

- 3.14 Mergers, acquisitions, and strategic partnerships landscape

- 3.15 Risk assessment and management

- 3.16 Major contract awards (2022-2025)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Direct effects protection products

- 5.2.1 Expanded metal foils

- 5.2.2 Conductive meshes

- 5.2.3 Diverter strips & strike terminals

- 5.2.4 Others

- 5.3 Indirect effects protection products

- 5.3.1 Transient voltage suppressors

- 5.3.2 Lightning-specific shielded connectors

- 5.3.3 Others

- 5.4 Bonding & grounding products

- 5.4.1 Bonding straps & jumpers

- 5.4.2 Grounding straps & bus bars

- 5.4.3 Static discharge wicks

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Airplanes

- 6.2.1 Commercial transport aircraft

- 6.2.2 Military transport

- 6.2.3 Others

- 6.3 Rotorcraft

- 6.3.1 Civil helicopters

- 6.3.2 Government & military helicopters

- 6.4 Unmanned aerial systems (UAS)

- 6.4.1 Tactical drones

- 6.4.2 Hale/male UAVs

- 6.4.3 Commercial drones

- 6.5 Electric & hybrid-electric aircraft

- 6.6 Powered-lift aircraft

- 6.7 Gliders

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Fit, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Line-fit

- 7.3 Retrofit

Chapter 8 Market Estimates and Forecast, By End User, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 OEMs (original equipment manufacturers)

- 8.3 Tier 1 & tier 2 suppliers

- 8.4 MRO (maintenance, repair & overhaul)

- 8.5 Aftermarket & retrofit

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 BAE Systems plc

- 10.1.2 Honeywell International Inc.

- 10.1.3 Collins Aerospace (Raytheon Technologies)

- 10.1.4 Safran S.A.

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 LORD Corporation

- 10.2.1.2 Spirit AeroSystems, Inc.

- 10.2.1.3 Triumph Group, Inc.

- 10.2.2 Europe

- 10.2.2.1 ATEC GmbH

- 10.2.2.2 Meggitt PLC

- 10.2.2.3 GKN Aerospace

- 10.2.3 APAC

- 10.2.3.1 Elbit Systems Ltd.

- 10.2.3.2 Moog Inc.

- 10.2.3.3 Aero Vodochody AEROSPACE a.s.

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Ferrostaal GmbH