|

市場調查報告書

商品編碼

1959659

抗生素抗藥性市場:機會、成長要素、產業趨勢分析及2026年至2035年預測Antibiotic Resistance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

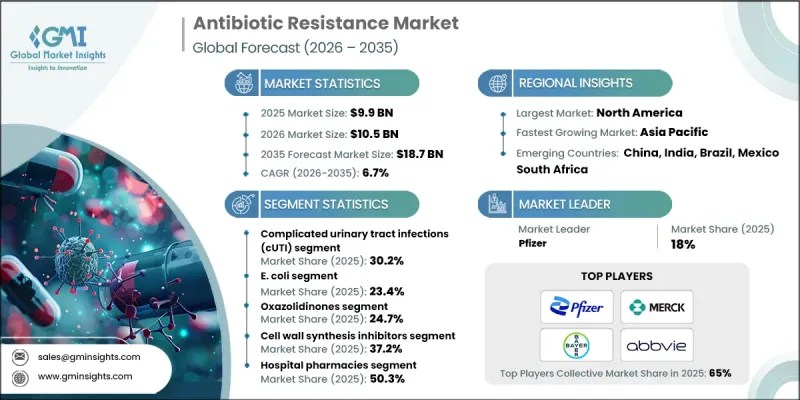

2025 年全球抗生素抗藥性市場價值為 99 億美元,預計到 2035 年將達到 187 億美元,年複合成長率為 6.7%。

抗菌素抗藥性(AMR)的日益惡化是推動這一市場成長的主要因素,而抗菌素抗藥性已成為全球醫療保健系統面臨的主要挑戰。多重抗藥性感染疾病的不斷增加,使得人們迫切需要新型抗生素、快速診斷方案和創新治療方法。抗生素的濫用和過度使用、醫院感染的蔓延以及抗藥性病原體的出現,都在推動新治療方法的研究和投資。人口老化、外科手術的增加以及慢性病盛行率的上升,都增加了感染風險,凸顯了病人安全和醫療成本控制的重要性。各國政府、衛生部門和製藥公司正在積極推行抗菌藥物管理計畫、監管獎勵和資金籌措舉措,意識提升也促進了市場擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 99億美元 |

| 預測金額 | 187億美元 |

| 複合年成長率 | 6.7% |

預計到2025年,複雜性尿道感染(cUTI)將佔泌尿道感染總數的30.2%,反映了其高發生率和臨床複雜性。患有糖尿病和腎臟病等潛在疾病的患者尤其容易感染cUTI,這也推高了對先進抗生素治療的需求。 cUTI通常與多重抗藥性病原體相關,需要頻譜治療以縮短住院時間並最大限度地減少併發症。臨床指南和研究舉措不斷推動有效治療通訊協定的製定,並促進能夠有效對抗抗藥性菌株的新療法的引入。

預計到2025年,大腸桿菌(E. coli)市佔率將達到23.4%,呈現顯著成長趨勢。大腸桿菌感染疾病構成重大的公共衛生挑戰,常導致嚴重的胃腸道疾病和併發症,進而增加醫療成本。感染率的上升及其帶來的醫療保健負擔,特異性推動著針對多重抗藥性大腸桿菌菌株的治療方法和診斷方法的投資增加,凸顯了該細分市場在更廣泛的抗生素抗藥性市場中的關鍵作用。

預計到2025年,美國抗生素抗藥性市場規模將達37億美元。憑藉完善的醫療基礎設施、嚴格的監測系統以及對抗生素使用計畫的巨額投資,美國已成為全球最先進的市場之一。抗藥性病原體(例如抗藥性金黃色葡萄球菌和銅綠假單胞菌)的高盛行率持續推動對快速診斷和創新治療方法的需求,使美國成為全球市場的主要驅動力。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 抗生素抗藥性感染疾病發生率增加

- 加大對新型抗生素研發的投入

- 對新型抗生素療法的需求日益成長

- 全球公共衛生議題和意識日益增強

- 產業潛在風險與挑戰

- 對新藥的抗藥性迅速出現

- 複雜的法規和發展過程

- 市場機遇

- 開發下一代抗生素和替代療法

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 專利分析

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估算與預測:依疾病分類,2022-2035年

- 複雜性尿道感染

- 複雜性腹腔內感染疾病

- 血液感染疾病

- 急性細菌性皮膚及皮膚組織感染疾病

- 社區型細菌性肺炎

- 醫院獲得性細菌性肺炎

第6章 市場估算與預測:依病原體分類,2022-2035年

- 大腸桿菌

- 肺炎克雷伯菌

- 銅綠假單胞菌

- 金黃色葡萄球菌

- 鮑曼 -鮑氏靜止桿菌

- 肺炎鏈球菌

- 流感細菌

第7章 市場估計與預測:依藥物類別分類,2022-2035年

- Oxazolidinone系列

- 頭孢菌素

- 醣肽

- 聯合治療

- 四環黴素

- 其他藥物類別

第8章 市場估算與預測:依作用機制分類,2022-2035年

- 細胞壁合成抑制劑

- 蛋白質合成抑制劑

- DNA合成抑制劑

- RNA合成抑制劑

- 其他作用機制

第9章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- AbbVie

- Basilea Pharmaceutical

- Bayer AG

- Merck and Co.

- Melinta Therapeutics

- Johnson & Johnson

- Paratek Pharmaceuticals

- Pfizer

- Shionogi & Co., Ltd.

- Tetraphase Pharmaceuticals

- Wockhardt

The Global Antibiotic Resistance Market was valued at USD 9.9 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 18.7 billion by 2035.

The market is fueled by the escalating global crisis of antimicrobial resistance (AMR), which has become a major concern for healthcare systems worldwide. The increasing incidence of multidrug-resistant infections has created a pressing demand for novel antibiotics, rapid diagnostic solutions, and innovative treatment options. Misuse and overuse of antibiotics, the prevalence of hospital-acquired infections, and the emergence of resistant pathogens are driving research and investment into new therapies. The growing elderly population, higher surgical interventions, and the rising prevalence of chronic diseases are heightening infection risks, emphasizing patient safety and healthcare cost management. Governments, health authorities, and pharmaceutical firms are promoting stewardship programs, regulatory incentives, and funding initiatives, while increased awareness among healthcare professionals and patients supports the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.9 Billion |

| Forecast Value | $18.7 Billion |

| CAGR | 6.7% |

The complicated urinary tract infections (cUTIs) segment accounted for 30.2% share in 2025, reflecting their high prevalence and clinical complexity. Patients with underlying health conditions such as diabetes or kidney disorders are particularly vulnerable, which boosts the demand for advanced antibiotic therapies. cUTIs often involve multidrug-resistant pathogens, necessitating broad-spectrum treatments to reduce hospital stays and minimize complications. Clinical guidelines and research initiatives continue to shape effective treatment protocols, driving the adoption of newer therapies capable of addressing resistant strains efficiently.

The Escherichia coli (E. coli) segment captured 23.4% share in 2025 and is anticipated to see substantial growth. E. coli infections pose significant public health challenges, often resulting in severe gastrointestinal illness and complications that can escalate healthcare costs. Rising outbreaks and the associated healthcare burden are motivating increased investment in therapies and diagnostics that specifically target multidrug-resistant E. coli strains, highlighting the critical role of this segment within the broader antibiotic resistance market.

U.S Antibiotic Resistance Market reached USD 3.7 billion in 2025. The country represents one of the most advanced markets globally, supported by a robust healthcare infrastructure, stringent surveillance systems, and significant investment in antimicrobial stewardship programs. The high prevalence of multidrug-resistant pathogens, including resistant Staphylococcus aureus and Pseudomonas aeruginosa strains, continues to drive demand for rapid diagnostics and innovative therapies, positioning the U.S. as a key growth driver in the global market.

Major players in the Global Antibiotic Resistance Market include Wockhardt, Johnson & Johnson, AbbVie, Pfizer, Paratek Pharmaceuticals, Bayer AG, Melinta Therapeutics, Shionogi & Co., Ltd., Tetraphase Pharmaceuticals, and Basilea Pharmaceutical. Companies in the antibiotic resistance market are employing several strategies to strengthen their presence and market position. They are investing heavily in research and development to discover novel antibiotics and therapies capable of combating multidrug-resistant pathogens. Strategic partnerships and collaborations with healthcare institutions, academic organizations, and government bodies help accelerate clinical trials and regulatory approvals. Firms are also focusing on expanding their global footprint, particularly in regions with high AMR prevalence. Investments in rapid diagnostic technologies and companion therapies enhance treatment efficacy and patient outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Disease trends

- 2.2.2 Pathogen trends

- 2.2.3 Drug class trends

- 2.2.4 Mechanism of action trends

- 2.2.5 Distribution channel trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of antibiotic-resistant infections

- 3.2.1.2 Increasing investments for research and development of novel antibiotics

- 3.2.1.3 Growing need for new antibiotic therapies

- 3.2.1.4 Increasing global public health concern and awareness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid emergence of resistance to new drugs

- 3.2.2.2 Complex regulatory and development process

- 3.2.3 Market opportunities

- 3.2.3.1 Development of next-generation antibiotics and alternative therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Disease, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Complicated urinary tract infections

- 5.3 Complicated intra-abdominal infections

- 5.4 Bloodstream infections

- 5.5 Acute bacterial skin and skin-structure infections

- 5.6 Community-acquired bacterial pneumonia

- 5.7 Hospital-acquired bacterial pneumonia

Chapter 6 Market Estimates and Forecast, By Pathogen, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 E. coli - Escherichia coli

- 6.3 K. pneumoniae - Klebsiella pneumoniae

- 6.4 P. aeruginosa - Pseudomonas aeruginosa

- 6.5 S. aureus - Staphylococcus aureus

- 6.6 Baumannii - Acinetobacter baumannii

- 6.7 S. pneumoniae - Streptococcus pneumoniae

- 6.8 H. influenzae

Chapter 7 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oxazolidinones

- 7.3 Cephalosporin

- 7.4 Lipoglycopeptides

- 7.5 Combination therapies

- 7.6 Tetracyclines

- 7.7 Other drug classes

Chapter 8 Market Estimates and Forecast, By Mechanism of Action, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Cell wall synthesis inhibitors

- 8.3 Protein synthesis inhibitors

- 8.4 DNA synthesis inhibitors

- 8.5 RNA synthesis inhibitors

- 8.6 Other mechanism of actions

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Basilea Pharmaceutical

- 11.3 Bayer AG

- 11.4 Merck and Co.

- 11.5 Melinta Therapeutics

- 11.6 Johnson & Johnson

- 11.7 Paratek Pharmaceuticals

- 11.8 Pfizer

- 11.9 Shionogi & Co., Ltd.

- 11.10 Tetraphase Pharmaceuticals

- 11.11 Wockhardt

抗生素抗藥性市場規模、佔有率和趨勢分析報告:按疾病、病原體、藥物類別、作用機制、分銷管道和細分市場預測(2026-2033 年)

抗生素抗藥性市場規模、佔有率和趨勢分析報告:按疾病、病原體、藥物類別、作用機制、分銷管道和細分市場預測(2026-2033 年) 抗菌藥物抗藥性市場:按藥物類別、疾病、分銷管道和地區分類

抗菌藥物抗藥性市場:按藥物類別、疾病、分銷管道和地區分類 抗生素抗藥性市場:依產品類型、病原體類型、感染疾病類型和最終用途分類-2026-2030年全球預測

抗生素抗藥性市場:依產品類型、病原體類型、感染疾病類型和最終用途分類-2026-2030年全球預測 全球抗生素抗藥性市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球抗生素抗藥性市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 抗生素抗藥性市場分析及預測(至2035年):類型、產品、服務、技術、應用、最終用戶、流程、組件、設備、解決方案

抗生素抗藥性市場分析及預測(至2035年):類型、產品、服務、技術、應用、最終用戶、流程、組件、設備、解決方案 抗生素抗藥性市場規模、佔有率和成長分析(按疾病、病原體、藥物類別、病原體類型、作用機制、分銷管道和地區分類)—產業預測(2026-2033 年)美國抗生素抗藥性市場規模、佔有率及趨勢分析報告:按疾病、病原體、藥物類別、作用機制、通路和細分市場預測,2025-2030 年全球銅綠病菌感染藥物市場規模(按類型、應用、地區、範圍和預測)

抗生素抗藥性市場規模、佔有率和成長分析(按疾病、病原體、藥物類別、病原體類型、作用機制、分銷管道和地區分類)—產業預測(2026-2033 年)美國抗生素抗藥性市場規模、佔有率及趨勢分析報告:按疾病、病原體、藥物類別、作用機制、通路和細分市場預測,2025-2030 年全球銅綠病菌感染藥物市場規模(按類型、應用、地區、範圍和預測) 抗生素抗性的全球市場 - 各治療藥:病原體,各治療類型:情形分析,附執行顧問指南(2025年~2029年)

抗生素抗性的全球市場 - 各治療藥:病原體,各治療類型:情形分析,附執行顧問指南(2025年~2029年)