|

市場調查報告書

商品編碼

1959657

非球面透鏡市場機會、成長要素、產業趨勢分析及2026年至2035年預測Aspherical Lens Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

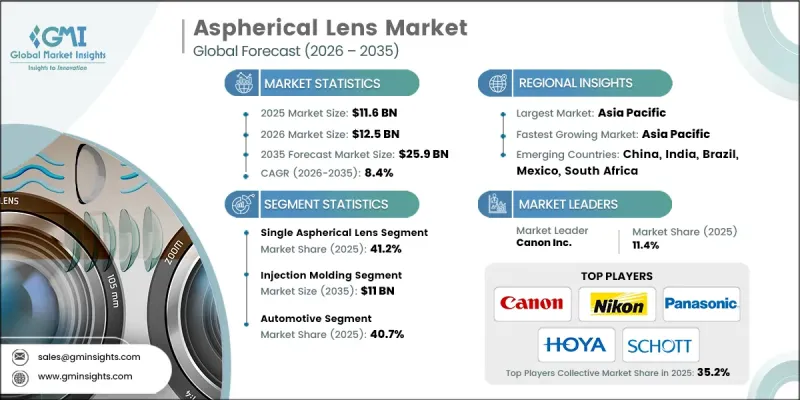

2025 年全球非球面透鏡市場價值為 116 億美元,預計到 2035 年將達到 259 億美元,年複合成長率為 8.4%。

市場成長主要得益於策略聯盟,這些聯盟使企業能夠獲得新技術、分銷網路和客戶群體,尤其是在汽車攝影機和擴增實境(XR) 設備等新興領域。政府加強促進半導體製造業發展也推動了市場擴張,國家補貼、獎勵計畫和晶圓廠擴建政策加速了晶圓消耗,並促進了晶圓回收等成本效益高的製造方法。汽車先進駕駛輔助系統(ADAS) 和雷射雷達 (LiDAR) 的應用是關鍵促進因素。高精度非球面透鏡透過精確聚焦光線和減少光學畸變來提高攝影機和感測器的性能。對智慧安全汽車的需求,以及對 ADAS 的監管支持,進一步推動了先進光學元件在汽車應用中的使用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 116億美元 |

| 預測金額 | 259億美元 |

| 複合年成長率 | 8.4% |

預計到2025年,單片非球面透鏡的市佔率將達到41.2%。這反映了其低成本、結構簡單且易於整合等優點,使其廣受歡迎。單片透鏡廣泛應用於家用電子電器、智慧型手機、輕便型相機和微型光學儀器等領域,在這些應用中,輕巧且高精度的光學元件至關重要。其緊湊的設計和優異的性能使其成為需要在小型外形規格下實現高解析度成像的應用的理想選擇。

2025年,拋光和研磨產業的市場規模達到38億美元,預計2026年至2035年將以7.4%的複合年成長率成長。這些工藝對於製造用於醫療設備、科學儀器和航太系統等高要求應用領域的高精度鏡片至關重要。自動化拋光和電腦控制研磨技術的進步正在提升鏡片的品質、精度和生產效率,使製造商能夠滿足市場對高階光學儀器日益成長的需求。

預計到2025年,北美非球面透鏡市佔率將達到27.6%。這主要得益於家用電子電器、汽車、醫療和工業應用領域對非球面透鏡的強勁需求。高精度光學儀器的早期應用,以及技術的創新,推動了先進鍍膜技術、小型化透鏡和緊湊型光學系統的發展。汽車產業對相機、影像感測器和光學儀器的需求不斷成長,進一步刺激了該地區對非球面透鏡的需求,使北美成為重要的成長中心。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對小型輕量光學設備的需求日益成長

- 透過策略聯盟和夥伴關係擴大市場影響

- 汽車ADAS和LiDAR系統的擴展

- 工業應用中對高性能光學系統的需求不斷成長

- 監控和安全系統的發展

- 產業潛在風險與挑戰

- 高昂的製造和生產成本

- 優質原料供應有限

- 市場機遇

- 光學元件正變得越來越小、越來越精確。

- 醫療影像診斷設備的擴展

- 促進因素

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線廣度

- 科技

- 創新

- 地理位置比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 財務績效比較

- 2022-2025 年重大發展

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估價與預測:依鏡片類型分類,2022-2035年

- 單非球面透鏡

- 雙面非球面透鏡

- 多面非球面透鏡

第6章 市場估算與預測:依材料類型分類,2022-2035年

- 玻璃

- 塑膠

- 混合

第7章 市場估算與預測:依製造技術分類,2022-2035年

- 射出成型

- 拋光和研磨

- 其他

第8章 市場估計與預測:依波長範圍分類,2022-2035年

- 紫外光(<400奈米)

- 可見光(400-700奈米)

- 近紅外線(700-1400奈米)

- 短波/中波紅外線(1400奈米或更長)

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 車

- 家用電子電器

- 數位相機

- 智慧型手機

- 其他

- 醫療及醫療設備

- 眼科光學

- 工業與測量

- 航太/國防

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 主要企業

- Canon Inc.

- Nikon Corporation

- Panasonic Holdings Corporation

- Hoya Corporation

- SCHOTT

- Carl Zeiss AG

- FUJIFILM Corporation

- Konica Minolta, Inc.

- KYOCERA Corporation

- 按地區分類的主要企業

- AGC Inc.

- ALPS ALPINE CO., LTD.

- Asahi Lite Optical Co., Ltd.

- Asia Optical Co., Inc.

- Shanghai Optics

- SUMITA OPTICAL GLASS, Inc.

- Tokai Optical Co. Ltd.

- Edmund Optics India Private Limited

- 特殊玩家/干擾者

- Asphericon GmbH

- Avantier Inc.

- Calin Technology Co. Ltd.

- Hyperion Optics

- Jenoptik AG

- Knight Optical

The Global Aspherical Lens Market was valued at USD 11.6 billion in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 25.9 billion by 2035.

Growth in this market is fueled by strategic partnerships, which allow companies to access new technologies, distribution networks, and customer segments, particularly in emerging areas such as automotive cameras and extended reality devices. Rising government initiatives to boost semiconductor manufacturing are also driving market expansion, with national subsidies, incentive programs, and fab expansion policies accelerating wafer consumption and promoting cost-efficient manufacturing practices like wafer reuse. The adoption of advanced driver assistance systems (ADAS) and LiDAR in vehicles is a critical driver, as high-precision aspherical lenses enhance camera and sensor performance by accurately focusing light and reducing optical distortions. Demand for intelligent, safe vehicles, coupled with regulatory support for ADAS, is further encouraging the adoption of advanced optical components in automotive applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.6 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 8.4% |

The single aspherical lens segment accounted for 41.2% share in 2025, reflecting its popularity due to low cost, simplicity, and ease of integration. Single lenses are widely used in consumer electronics, smartphones, compact cameras, and small optical devices where lightweight, precision optics are essential. Their compact design and performance advantages make them ideal for applications requiring high-resolution imaging in a small form factor.

The polishing & grinding segment was valued at USD 3.8 billion in 2025 and is expected to grow at a CAGR of 7.4% during 2026-2035. These processes are crucial for producing high-precision lenses used in demanding applications such as medical devices, scientific instruments, and aerospace systems. Technological advancements in automated polishing and computer-controlled grinding are enhancing lens quality, precision, and production efficiency, enabling manufacturers to meet the rising demand for premium optics.

North America Aspherical Lens Market held a 27.6% share in 2025, driven by robust adoption of aspherical lenses across consumer electronics, automotive, medical, and industrial applications. Early adoption of high-precision optics, coupled with technological innovation, is enabling companies to develop advanced coatings, miniaturized lenses, and compact optical systems. The growing use of cameras, image sensors, and optical devices in vehicles is further fueling demand for aspherical lenses in the region, making North America a key growth hub.

Leading companies operating in the Global Aspherical Lens Market include AGC Inc., ALPS ALPINE CO., LTD., Asahi Lite Optical Co., Ltd., Asia Optical Co., Inc., Asphericon GmbH, Avantier Inc., Calin Technology Co., Ltd., Canon Inc., Carl Zeiss AG, Edmund Optics India Private Limited, FUJIFILM Corporation, and Hoya Corporation. Key strategies adopted by companies to strengthen their Aspherical Lens Market presence include forming strategic alliances and partnerships to access emerging markets, advanced manufacturing technologies, and distribution channels. Companies are investing in R&D to improve lens quality, optical performance, miniaturization, and coating technologies. Expansion of production capacity, particularly for high-precision lenses used in automotive and industrial applications, is a priority. Firms are leveraging government incentives and subsidies to scale operations cost-effectively. Additionally, companies are focusing on product portfolio diversification, targeting new applications in automotive cameras, AR/VR devices, and scientific instruments, and collaborating with technology providers to integrate lenses into complex optical systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Lens type trends

- 2.2.2 Material type trends

- 2.2.3 Manufacturing technology trends

- 2.2.4 Wavelength range trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for compact and lightweight optical devices

- 3.2.1.2 Strategic collaborations and partnerships to expand market presence

- 3.2.1.3 Expansion of automotive ADAS and LiDAR systems

- 3.2.1.4 Rising demand for high-performance optical systems in industrial applications

- 3.2.1.5 Growth in surveillance and security systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and production costs

- 3.2.2.2 Limited availability of high-quality raw materials

- 3.2.3 Market opportunities

- 3.2.3.1 Advancements in miniaturized and high-precision optical components

- 3.2.3.2 Expansion in medical imaging and diagnostic equipment

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Lens Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Single aspherical lens

- 5.3 Bi-aspherical lens

- 5.4 Multi aspherical lens

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Glass

- 6.3 Plastic

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Manufacturing Technology, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Injection molding

- 7.3 Polishing & grinding

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Wavelength Range, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Ultraviolet (<400 nm)

- 8.3 Visible (400-700 nm)

- 8.4 Near-infrared (700-1400 nm)

- 8.5 Shortwave/mid infrared (>1,400 nm)

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Consumer electronics

- 9.3.1 Digital cameras

- 9.3.2 Smartphones

- 9.3.3 Others

- 9.4 Healthcare & medical

- 9.5 Ophthalmic optics

- 9.6 Industrial & metrology

- 9.7 Aerospace & defense

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Canon Inc.

- 11.1.2 Nikon Corporation

- 11.1.3 Panasonic Holdings Corporation

- 11.1.4 Hoya Corporation

- 11.1.5 SCHOTT

- 11.1.6 Carl Zeiss AG

- 11.1.7 FUJIFILM Corporation

- 11.1.8 Konica Minolta, Inc.

- 11.1.9 KYOCERA Corporation

- 11.2 Regional Key Players

- 11.2.1 AGC Inc.

- 11.2.2 ALPS ALPINE CO., LTD.

- 11.2.3 Asahi Lite Optical Co., Ltd.

- 11.2.4 Asia Optical Co., Inc.

- 11.2.5 Shanghai Optics

- 11.2.6 SUMITA OPTICAL GLASS, Inc.

- 11.2.7 Tokai Optical Co. Ltd.

- 11.2.8 Edmund Optics India Private Limited

- 11.3 Niche Players / Disruptors

- 11.3.1 Asphericon GmbH

- 11.3.2 Avantier Inc.

- 11.3.3 Calin Technology Co. Ltd.

- 11.3.4 Hyperion Optics

- 11.3.5 Jenoptik AG

- 11.3.6 Knight Optical

非球面透鏡市場:依材料、價格範圍、應用、最終用途及通路分類-2026-2032年全球市場預測複消色差顯微鏡物鏡市場:按放大倍率、數值孔徑、穿透類型、鏡片鍍膜、波長範圍、最終用戶、應用和銷售管道,全球預測,2026-2032年全球復消色差物鏡市場:按產品組合、技術、材料、放大倍率範圍、分銷管道和最終用途行業分類的預測(2026-2032年)

非球面透鏡市場:依材料、價格範圍、應用、最終用途及通路分類-2026-2032年全球市場預測複消色差顯微鏡物鏡市場:按放大倍率、數值孔徑、穿透類型、鏡片鍍膜、波長範圍、最終用戶、應用和銷售管道,全球預測,2026-2032年全球復消色差物鏡市場:按產品組合、技術、材料、放大倍率範圍、分銷管道和最終用途行業分類的預測(2026-2032年) 2026年全球非球面透鏡市場報告

2026年全球非球面透鏡市場報告 非球面透鏡市場分析及預測(至2035年):依類型、產品類型、應用、技術、材質、最終用戶、組件、功能、安裝類型及製程分類

非球面透鏡市場分析及預測(至2035年):依類型、產品類型、應用、技術、材質、最終用戶、組件、功能、安裝類型及製程分類 非球面透鏡市場規模、佔有率和成長分析(按材質、最終用途、通路、應用、價格範圍和地區分類)-2026-2033年產業預測

非球面透鏡市場規模、佔有率和成長分析(按材質、最終用途、通路、應用、價格範圍和地區分類)-2026-2033年產業預測 非球面透鏡的全球市場

非球面透鏡的全球市場 非球面鏡頭市場,規模,佔有率,趨勢,產業分析報告:不同形狀,各材料,各用途,各地區,2025年~2034年的市場預測

非球面鏡頭市場,規模,佔有率,趨勢,產業分析報告:不同形狀,各材料,各用途,各地區,2025年~2034年的市場預測