|

市場調查報告書

商品編碼

1959653

速凍冷卻器市場機會、成長要素、產業趨勢分析及2026年至2035年預測。Blast Chillers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

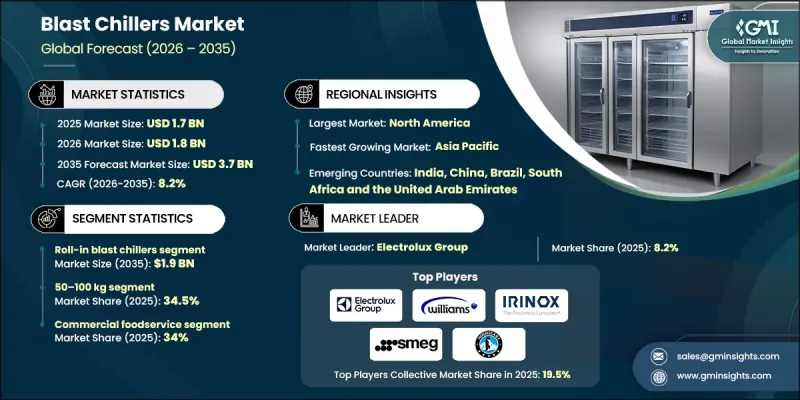

2025 年全球速凍冷卻器市場價值為 17 億美元,預計到 2035 年將達到 37 億美元,年複合成長率為 8.2%。

市場成長的促進因素包括:全球食品安全標準的不斷完善、餐飲服務和加工行業對快速冷卻技術的日益普及,以及在保持低溫運輸完整性的同時最大限度減少食物浪費的重要性日益凸顯。包括嚴格的溫度控制指南在內的法規結構,正鼓勵企業採用現代化的冷卻解決方案。食品加工商和商用廚房越來越依賴冷卻器來快速降低已烹調產品的溫度,抑制病原體的生長,並符合政府規定的食品安全標準。特別是家禽、肉類和即食食品生產商,高度依賴這些系統來滿足即時冷卻和防止污染的建議。速凍冷卻器技術的進步也有助於提高大批量加工環境中的營運效率、一致性和操作安全性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 17億美元 |

| 預測金額 | 37億美元 |

| 複合年成長率 | 8.2% |

預計2035年,滾入式冷卻器市場規模將達19億美元。由於滾入式速凍機能夠容納全尺寸移動式貨架,因此在中央廚房、機構餐飲服務和工業食品加工等大型應用中越來越受歡迎。這些設備支援批量烹飪工作流程,同時提供均勻且穩定的冷卻,滿足日益嚴格的食品安全標準和溫度控制要求。其高效的運作性能使其成為在尖峰時段維持產品品質的理想選擇。

到2025年,50-100公斤容量的冷藏設備將佔據34.5%的市場。這項容量的冷藏設備正受到中型餐廳、麵包店和雲端廚房的青睞,這些企業需要高冷凍能力,但又不想投資購買大型工業設備。隨著產量增加,平衡空間、速度和能源效率對企業至關重要。這些中等容量的冷藏設備能夠快速冷卻產品,同時保持產品的新鮮度、均勻性和嚴格的溫度控制,從而支援日常運作並滿足監管要求。

預計到2025年,北美速凍冷卻器市佔率將達到37.7%。該地區市場擴張的促進因素包括嚴格的食品安全法規、低溫運輸基礎設施的現代化以及商業廚房和餐飲服務行業的規模化發展。速凍冷卻器廣泛應用於大批量生產環境中,以確保產品品質、減少廢棄物並符合當地的溫度控制標準。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 食品加工設施對快速冷卻解決方案的需求不斷成長

- 嚴格的食品安全法規和合規要求

- 全球低溫運輸基礎設施擴張

- 商用廚房、飯店和快餐店 (QSR) 的成長

- 產業潛在風險與挑戰

- 較高的初始投資和維護成本

- 對能源消耗和運作效率的擔憂

- 市場機遇

- 採用節能環保的冷凍技術

- 來自速食和包裝食品行業的需求增加

- 促進因素

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年重大發展

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 滾入式速凍冷卻器

- 直立式速凍冷卻器

第6章 市場估計與預測:依產能分類,2022-2035年

- 體重低於50公斤

- 50~100kg

- 101-200kg

- 超過200公斤

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 商用食品服務業

- 餐廳和快餐店

- 飯店和度假村

- 餐飲公司

- 麵包店和糖果甜點

- 設施廚房

- 醫院和醫療設施

- 學校和大學

- 懲教設施

- 食品加工/製造

- 肉類、水產品和家禽加工公司

- 即食食品 (RTE) 和冷凍食品製造商

- 乳製品加工

- 物流和低溫運輸

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 主要企業

- Alto Shaam, Inc

- Electrolux Group

- 星崎歐洲 BV(星崎株式會社)

- Williams Refrigeration

- 按地區分類的主要企業

- 北美洲

- Traulsen &Co., Inc.

- Victory Refrigeration LLC

- Foster Refrigerator

- 歐洲

- 冷靜的歐洲

- IRINOX SpA

- SMEG SpA

- 亞太地區

- Infrico

- Lainox

- Friginox

- 北美洲

- 特殊玩家/干擾者

- Fulgor Milano

- TEFCOLD(UK)

The Global Blast Chillers Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 3.7 billion by 2035.

Market growth is fueled by rising global food safety standards, increasing adoption of rapid cooling technologies in foodservice and processing sectors, and growing emphasis on minimizing food waste while maintaining cold chain integrity. Regulatory frameworks, including strict guidelines on temperature control, are pushing operators to adopt modern cooling solutions. Food processors and commercial kitchens are increasingly relying on blast chillers to quickly reduce the temperature of cooked products, reducing pathogen growth and complying with government-mandated food safety standards. Producers of poultry, meat, and ready-to-eat foods are particularly dependent on these systems to meet recommendations for immediate chilling and contamination prevention. Advancements in blast chiller technology are also improving workflow efficiency, consistency, and operational safety in high-volume environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 8.2% |

The roll-in blast chillers segment is expected to reach USD 1.9 billion by 2035. Roll-in units are increasingly favored for large-scale applications, including central kitchens, institutional food service, and industrial food processing, due to their ability to accommodate full mobile racks. These units support batch preparation workflows while ensuring uniform and consistent cooling, aligning with stricter food safety and temperature control requirements. Their operational efficiency makes them ideal for maintaining quality in peak production periods.

The 50-100 kg capacity segment accounted for 34.5% share in 2025. This segment is growing in popularity among mid-sized restaurants, bakeries, and cloud kitchens that require higher cooling capabilities without investing in full-scale industrial equipment. Balancing space, speed, and energy efficiency is crucial for operators as production volumes increase. These mid-capacity units allow kitchens to cool products quickly while preserving freshness, consistency, and strict temperature control, supporting daily operations and regulatory compliance.

North America Blast Chillers Market held a 37.7% share in 2025. Market expansion in the region is driven by stringent food safety regulations, modernization of cold chain infrastructure, and the growing scale of commercial kitchens and foodservice operations. Blast chillers are widely adopted to maintain product quality, reduce spoilage, and ensure compliance with regional temperature-control standards across high-volume environments.

Key players in the Global Blast Chillers Market include Foster Refrigerator, Hoshizaki Europe B.V., Electrolux Group, IRINOX S.p.A., Lainox, TEFCOLD (UK), Cool Head Europe, Alto Shaam, Inc., Traulsen & Co., Inc., Victory Refrigeration LLC, Infrico, Friginox, SMEG S.p.A., Williams Refrigeration, and Fulgor Milano. Companies in the blast chillers market are focusing on strengthening their presence by investing in research and development to enhance cooling efficiency, durability, and user-friendly features. Many are expanding product lines with roll-in and mid-capacity units to cater to different commercial and industrial needs. Strategic partnerships with foodservice chains, catering businesses, and institutional kitchens ensure early adoption and long-term contracts. Firms are also emphasizing energy-efficient technologies, IoT-enabled monitoring, and smart cold chain integration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Capacity trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for rapid cooling solutions in food processing facilities

- 3.2.1.2 Stringent food safety regulations and compliance requirements

- 3.2.1.3 Expansion of the global cold chain infrastructure

- 3.2.1.4 Growth of commercial kitchens, hotels, and quick-service restaurants (QSRs)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and maintenance costs

- 3.2.2.2 Energy consumption and operational efficiency concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of energy-efficient and eco-friendly refrigeration technologies

- 3.2.3.2 Increasing demand from ready-to-eat and packaged food industries

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Million and Units)

- 5.1 Key trends

- 5.2 Roll In Blast Chillers

- 5.3 Reach-In Blast Chillers

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 ($ Million and Units)

- 6.1 Key trends

- 6.2 Below 50KG

- 6.3 50 - 100KG

- 6.4 101-200KG

- 6.5 More than 200KG

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Million and Units)

- 7.1 Key trends

- 7.2 Commercial foodservice

- 7.2.1 Restaurants & QSR

- 7.2.2 Hotels & resorts

- 7.2.3 Catering companies

- 7.2.4 Bakeries & confectioneries

- 7.3 Institutional kitchens

- 7.3.1 Hospitals & healthcare facilities

- 7.3.2 Schools & universities

- 7.3.3 Correctional facilities

- 7.4 Food processing & manufacturing

- 7.4.1 Meat, seafood, poultry processors

- 7.4.2 Ready-to-eat (RTE) and frozen food manufacturers

- 7.4.3 Dairy processing

- 7.5 Logistics & cold chain

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Million and Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Alto Shaam, Inc

- 9.1.2 Electrolux Group

- 9.1.3 Hoshizaki Europe B.V. (Hoshizaki Corporation)

- 9.1.4 Williams Refrigeration

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Traulsen & Co., Inc.

- 9.2.1.2 Victory Refrigeration LLC

- 9.2.1.3 Foster Refrigerator

- 9.2.2 Europe

- 9.2.2.1 Cool Head Europe

- 9.2.2.2 IRINOX S.p.A.

- 9.2.2.3 SMEG S.p.A.

- 9.2.3 APAC

- 9.2.3.1 Infrico

- 9.2.3.2 Lainox

- 9.2.3.3 Friginox

- 9.2.1 North America

- 9.3 Niche Players / Disruptors

- 9.3.1 Fulgor Milano

- 9.3.2 TEFCOLD (UK)

2026年全球快速冷凍庫市場報告

2026年全球快速冷凍庫市場報告 黃銅箱市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、最終用戶、地區和競爭對手分類,2021-2031年

黃銅箱市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、最終用戶、地區和競爭對手分類,2021-2031年 全球冷卻器市場

全球冷卻器市場 速凍冷卻器市場:按產品類型、按容量、按最終用戶、按應用、按地區

速凍冷卻器市場:按產品類型、按容量、按最終用戶、按應用、按地區