|

市場調查報告書

商品編碼

1959648

LED燈市場機會、成長要素、產業趨勢分析及2026年至2035年預測LED Lamp Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025年全球LED燈市場價值400億美元,預計2035年將以11.6%的複合年成長率成長,達到1,280億美元。

在節能照明需求、成本降低、政府扶持政策、快速都市化以及智慧連網照明系統日益普及的推動下, LED燈的能源效率遠高於傳統照明技術,能夠為家庭、企業和公共機構帶來長期的成本節約和環境影響降低。世界各國政府正在實施能源效率標準,以促進LED的普及、減少溫室氣體排放並降低電力成本。整合感測器和控制系統的智慧聯網LED照明解決方案正擴大應用於商業設施、公共建築和智慧城市計劃中,從而最佳化能源消耗並提升用戶舒適度。隨著工業、商業和住宅領域的廣泛應用, LED燈正成為現代基礎設施和永續舉措的關鍵組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 400億美元 |

| 預測金額 | 1280億美元 |

| 複合年成長率 | 11.6% |

預計到2025年,A型LED燈具市場規模將達141.4億美元。由於政府法規強制淘汰白熾燈和低效照明設備,A型LED燈正被廣泛採用。這些燈具具有使用壽命更長、維護成本更低、能耗更低等優點,適用於住宅和商業場所。節能計畫、建築規範和維修舉措正在推動A型LED燈具的普及,製造商也正致力於開發高效節能、易於維修的A型LED燈具,以滿足監管合規性和永續性目標。

預計2025年,室內照明市場規模將達到145.4億美元。住宅、辦公和公共空間需求的成長是推動市場成長的主要動力。與傳統照明相比,室內LED照明具有更高的效率、更長的使用壽命和更低的運作成本。各地對能源效率法規和建築規範的遵守進一步加速了LED照明的普及。製造商正優先開發功能多樣、品質卓越的室內LED解決方案,並配備改裝套件和智慧控制功能,以確保大規模部署。

預計到2025年,北美LED燈市佔率將達到38.5%。這項區域成長主要得益於嚴格的能源效率標準、永續性舉措以及政府激勵措施,這些措施旨在促進公共基礎設施、住宅維修和商業計劃中採用固體照明。電力公司補貼計畫、連網照明系統和智慧控制系統在提升營運效率的同時降低了能源成本,推動了LED燈具在新建和維修計劃中的應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 提高能源效率和降低成本

- 政府監理與能源政策

- 快速的都市化和基礎建設

- 對智慧互聯照明的需求日益成長

- 擴大商業和工業領域的招聘

- 挑戰與困難

- 在價格敏感的市場中,初始安裝成本較高。

- 品質參差不齊以及仿冒品的存在

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 供應鏈韌性

- 地緣政治分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 產品系列比較

- 2022-2025 年重大發展

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張和投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依產品類型分類,2022-2035年

- A型

- T型

- 裝飾燈

- 反射鏡

- 其他

第6章 市場估計與預測:依技術分類,2022-2035年

- 主要趨勢

- 標準LED

- 智慧LED

- 有機發光二極體(OLED)

第7章 市場估價與預測:依通路分類,2022-2035年

- 主要趨勢

- 線上零售商

- 專賣店

- 超級市場/大賣場

- 直銷

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 主要趨勢

- 室內照明

- 戶外照明

- 汽車照明

- 其他(例如,園藝、標誌)

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 住宅

- 商業的

- 產業

- 政府/公共部門

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第11章:公司簡介

- 主要企業

- Philips Lighting(Signify)

- Osram

- GE Lighting

- Samsung Electronics

- Cree, Inc.

- Nichia Corporation

- Panasonic Corporation

- Lumileds Holding BV

- 按地區分類的主要企業

- 北美洲

- Acuity Brands

- Eaton Corporation

- Hubbell Incorporated

- Bridgelux, Inc.

- 歐洲

- Zumtobel Group

- Dialight plc

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- 亞太地區

- LG Innotek

- Seoul Semiconductor

- Everlight Electronics

- MLS Co., Ltd.(Forest Lighting)

- Toshiba Lighting &Technology Corporation

- Lumens Co., Ltd.

- 北美洲

- 小眾/顛覆者

- Epistar Corporation

- Sharp Corporation

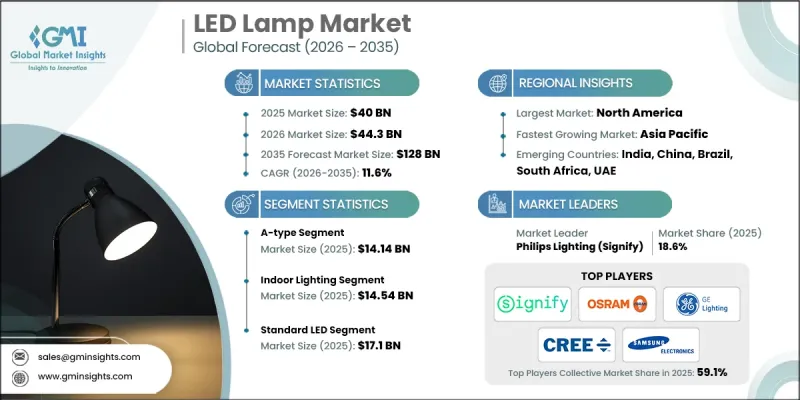

The Global LED Lamp Market was valued at USD 40 billion in 2025 and is estimated to grow at a CAGR of 11.6% to reach USD 128 billion by 2035.

The market is expanding rapidly, driven by the push for energy-efficient lighting, cost savings, favorable government regulations, rapid urbanization, and rising adoption of smart and connected lighting systems. LED lamps consume significantly less energy than traditional lighting technologies, offering long-term savings for households, businesses, and public institutions while reducing environmental impact. Governments worldwide are introducing efficiency standards that accelerate LED adoption, cut greenhouse gas emissions, and lower electricity expenses. Smart and networked LED lighting solutions, integrated with sensors and controls, are increasingly deployed in commercial, institutional, and smart city projects, optimizing energy consumption and enhancing user comfort. Industrial, commercial, and residential sectors are driving widespread adoption, making LED lamps a critical component in modern infrastructure and sustainable development initiatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40 Billion |

| Forecast Value | $128 Billion |

| CAGR | 11.6% |

The A-type segment generated USD 14.14 billion in 2025. A-type LED lamps are widely adopted due to government mandates phasing out incandescent and inefficient lighting. These lamps offer longer lifespans, lower maintenance, and reduced energy consumption across residential and commercial spaces. Energy efficiency programs, building codes, and retrofit initiatives are driving mainstream adoption, with manufacturers focusing on high-efficacy, retrofit-ready A-type lamps to align with regulatory compliance and sustainability targets.

The indoor lighting segment accounted for USD 14.54 billion in 2025. Rising demand in homes, offices, and institutional buildings is fueling the market. Indoor LED lighting provides high efficiency, extended durability, and lower operational costs compared to conventional lighting. Compliance with energy-efficiency regulations and building codes across regions further encourages adoption. Manufacturers are prioritizing versatile, high-quality indoor LED solutions with retrofit kits and smart control capabilities to capture large-scale deployments.

North America LED Lamp Market held a 38.5% share in 2025. The region's growth is supported by stringent energy efficiency standards, sustainability initiatives, and government incentives promoting solid-state lighting in public infrastructure, residential retrofits, and commercial projects. Utility rebate programs, connected lighting systems, and smart controls enhance operational performance while lowering energy costs, driving adoption across new constructions and retrofit projects.

Key players in the LED Lamp Market include Philips Lighting (Signify), Osram, GE Lighting, Cree, Inc., Samsung Electronics, LG Innotek, Acuity Brands, Eaton Corporation, Hubbell Incorporated, Zumtobel Group, Nichia Corporation, Seoul Semiconductor, Everlight Electronics, Lumileds Holding B.V., Dialight plc, MLS Co., Ltd. (Forest Lighting), Toshiba Lighting & Technology Corporation, Panasonic Corporation, Bridgelux, Inc., Lumens Co., Ltd., Epistar Corporation, Toyoda Gosei Co., Ltd., Citizen Electronics Co., Ltd., and Sharp Corporation. Companies in the Global LED Lamp Market are adopting strategies such as expanding R&D for high-efficacy and smart lighting solutions, developing retrofit-compatible products, and ensuring compliance with energy certification standards. Firms are forming strategic alliances, leveraging government incentives, and targeting commercial, industrial, and smart city projects to boost adoption. Geographic expansion, digital marketing, and distributor partnerships enhance market reach. Innovation in connected and energy-efficient lighting, combined with after-sales support, ensures customer loyalty, strengthens brand positioning, and addresses evolving sustainability and operational efficiency demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Technology trends

- 2.2.3 Distribution Channel trends

- 2.2.4 Application trends

- 2.2.5 End-user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Energy efficiency and cost savings

- 3.2.1.2 Government regulations and energy policies

- 3.2.1.3 Rapid urbanization and infrastructure development

- 3.2.1.4 Growing demand for smart and connected lighting

- 3.2.1.5 Rising adoption in commercial and industrial applications

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High initial installation costs in price-sensitive markets

- 3.2.2.2 Quality inconsistency and presence of counterfeit products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 A-type

- 5.3 T-type

- 5.4 Decorative lamps

- 5.5 Reflectors

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 6.1 Key Trends

- 6.2 Standard LED

- 6.3 Smart LED

- 6.4 OLED

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million & Units)

- 7.1 Key Trends

- 7.2 Online retailers

- 7.3 Specialty stores

- 7.4 Supermarkets/Hypermarkets

- 7.5 Direct sales

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 8.1 Key Trends

- 8.2 Indoor lighting

- 8.3 Outdoor lighting

- 8.4 Automotive lighting

- 8.5 Others (e.g., horticulture, signage)

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

- 9.5 Government/Public

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Philips Lighting (Signify)

- 11.1.2 Osram

- 11.1.3 GE Lighting

- 11.1.4 Samsung Electronics

- 11.1.5 Cree, Inc.

- 11.1.6 Nichia Corporation

- 11.1.7 Panasonic Corporation

- 11.1.8 Lumileds Holding B.V.

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Acuity Brands

- 11.2.1.2 Eaton Corporation

- 11.2.1.3 Hubbell Incorporated

- 11.2.1.4 Bridgelux, Inc.

- 11.2.2 Europe

- 11.2.2.1 Zumtobel Group

- 11.2.2.2 Dialight plc

- 11.2.2.3 Toyoda Gosei Co., Ltd.

- 11.2.2.4 Citizen Electronics Co., Ltd.

- 11.2.3 Asia Pacific

- 11.2.3.1 LG Innotek

- 11.2.3.2 Seoul Semiconductor

- 11.2.3.3 Everlight Electronics

- 11.2.3.4 MLS Co., Ltd. (Forest Lighting)

- 11.2.3.5 Toshiba Lighting & Technology Corporation

- 11.2.3.6 Lumens Co., Ltd.

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 Epistar Corporation

- 11.3.2 Sharp Corporation