|

市場調查報告書

商品編碼

1959645

先進生質燃料市場機會、成長要素、產業趨勢分析及2026年至2035年預測Advanced Biofuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

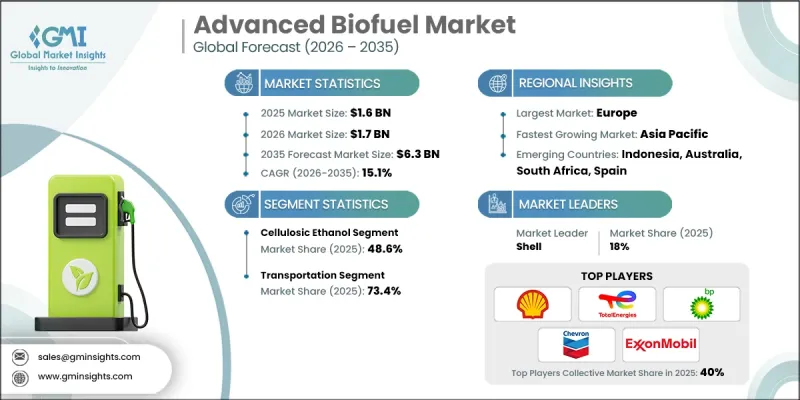

2025 年全球先進生質燃料市場價值 16 億美元,預計到 2035 年將達到 63 億美元,年複合成長率為 15.1%。

這一成長得益於各國政府致力於減少對進口原油的依賴並加強國家能源安全的努力。各國優先發展國內生產的可再生燃料,以降低供應鏈脆弱性、避險價格波動風險並增強能源獨立性。先進生質燃料對於已開發經濟體和新興經濟體建構韌性能源系統至關重要,因為它們提供了可擴展的、與現有燃料基礎設施相容的可再生替代燃料。支持永續生質燃料生產的政策獎勵、財政津貼和監管要求正在推動市場發展。農業殘餘物、藻類、廢油和木質纖維素材料等非糧食生質能原料供應量的增加,提高了整個生物燃料價值鏈的永續性,並最大限度地減少了與糧食生產的競爭。技術進步、扶持政策和公私合營的結合正在加速全球的推廣應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 16億美元 |

| 預測金額 | 63億美元 |

| 複合年成長率 | 15.1% |

先進生質燃料利用非食用生質能生產,例如農業殘餘物、林業廢棄物、藻類和廢油。這些燃料具有卓越的溫室氣體減排效果、更高的能源效率,並且與現有的交通運輸、發電和工業燃料基礎設施高度相容。政府的各項措施和財政獎勵正在加速先進生物燃料的推廣應用,降低商業化風險,並提升新興技術計劃的資金籌措潛力。擴大原料來源符合循環經濟原則,有助於減少對石化燃料的依賴,並增強國家能源安全。此外,該行業還受益於製程改進,例如更高效的生質能預處理、酶水解和發酵技術,這些改進正在推動成本降低和生產規模擴大。

預計到2025年,纖維素乙醇的市佔率將達到48.6%,並將在2035年之前以14.8%的複合年成長率持續成長。預處理製程、酵素水解和發酵技術的進步提高了轉化效率、酵素性能和原料利用率,從而提升了其經濟效益。對非食用生物生質燃料的監管支持也推動了其應用。纖維素乙醇符合燃料混合要求,減少了與糧食作物的競爭,並在其整個生命週期中顯著減少了溫室氣體排放。其與現有燃料基礎設施的兼容性使其成為交通燃料脫碳的重要解決方案。

預計到2025年,交通運輸領域將佔據73.4%的市場佔有率,並在2035年之前以14.7%的複合年成長率成長。各國和企業為實現淨零排放目標而加大力度,推動了先進生質燃料的普及應用。與傳統燃料相比,這些燃料可顯著減少二氧化碳排放,並為電氣化程度較低的產業提供實際的脫碳途徑。先進生質燃料正日益融入長期永續性和排放策略,幫助車輛營運商、公共運輸業者和物流營運商實現監管和環境目標。

美國先進生質燃料市場預計2025年將佔據93.4%的市場佔有率,到2035年將成長至20億美元。豐富的農業原料、日益成長的氣候變遷擔憂以及強勁的國內生物技術創新正在推動先進生物燃料的普及。主要企業正專注於纖維素和藻類燃料的生產,以擴大營運規模並實現更顯著的排放目標,同時充分利用政策支援、研發激勵措施和先進的生產技術。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系統

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 成本結構分析

- 價格趨勢分析(美元/噸)

- 按燃料類型

- 波特五力分析

- PESTEL 分析

- 新機會與趨勢

- 數位化和物聯網整合

- 進入新興市場

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 戰略儀錶板

- 策略舉措

- 企業標竿管理

- 創新與科技趨勢

第5章 市場規模及預測:依燃料類型分類,2022-2035年

- 纖維素基乙醇

- 生質柴油

- 生物丁醇

- 其他

第6章 市場規模及預測:依原料分類,2022-2035年

- 農業

- 林業

- 廢棄物

- 其他

第7章 市場規模及預測:依應用領域分類,2022-2035年

- 運輸

- 航空領域

- 其他

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 西班牙

- 英國

- 義大利

- 亞太地區

- 中國

- 印度

- 印尼

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第9章:公司簡介

- Advance Biofuel

- Aemetis

- Blue Biofuels

- Borregaard

- BP

- Byogy Renewables

- Chevron

- Clariant

- Enerkem

- ExxonMobil

- Gevo

- GranBio

- Green Plains

- Galp

- Indian Oil Corporation Limited

- Logen

- Praj Industries

- Shell

- TotalEnergies

- Votion Biorefineries

The Global Advanced Biofuel Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 15.1% to reach USD 6.3 billion by 2035.

Growth is driven by governments' focus on reducing reliance on imported crude oil and strengthening national energy security. Countries are prioritizing domestically produced renewable fuels to reduce supply chain vulnerabilities, hedge against price volatility, and enhance energy independence. Advanced biofuels offer scalable, renewable alternatives compatible with existing fuel infrastructure, making them critical for both developed and emerging economies seeking resilient energy systems. The market is benefiting from policy incentives, financial grants, and regulatory mandates that support sustainable fuel production. Increasing availability of non-food biomass feedstocks such as agricultural residues, algae, waste oils, and lignocellulosic materials is improving sustainability across the biofuel value chain while minimizing competition with food production. The combination of technological progress, supportive policies, and public-private collaborations is accelerating adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 15.1% |

Advanced biofuels are derived from non-food biomass, including agricultural residues, forestry waste, algae, and waste oils. These fuels offer superior greenhouse gas reductions, improved energy efficiency, and high compatibility with existing transport, power generation, and industrial fuel infrastructure. Government initiatives and fiscal incentives are accelerating adoption, mitigating commercialization risks, and enhancing project bankability for emerging technologies. Expanding feedstock availability supports circular economy principles, reduces reliance on fossil fuels, and strengthens national energy security. The industry is also benefiting from process improvements, such as more efficient biomass pretreatment, enzymatic hydrolysis, and fermentation techniques, which are driving cost reductions and increasing production scalability.

The cellulosic ethanol segment held 48.6% share in 2025 and is expected to grow at a CAGR of 14.8% through 2035. Technological advancements in pretreatment processes, enzymatic hydrolysis, and fermentation are improving economic feasibility by enhancing conversion efficiencies, enzyme performance, and feedstock utilization. Regulatory support for non-food-based biofuels is further boosting adoption, as cellulosic ethanol meets blending mandates, reduces competition with food crops, and achieves deeper lifecycle greenhouse gas reductions. Its compatibility with existing fuel infrastructure positions it as a key solution for decarbonizing transport fuels.

The transportation applications segment accounted for 73.4% share in 2025 and is projected to grow at a CAGR of 14.7% through 2035. Rising national and corporate commitments to achieve net-zero targets are driving advanced biofuel adoption. These fuels deliver significant CO2 reductions over conventional fuels and serve as a practical decarbonization pathway in sectors where electrification remains limited. Advanced biofuels are increasingly integrated into long-term sustainability and emission reduction strategies, supporting fleet operators, public transport authorities, and logistics providers in meeting regulatory and environmental targets.

U.S Advanced Biofuel Market held a 93.4% share in 2025 and is projected to generate USD 2 billion by 2035. Abundant agricultural feedstocks, growing climate change concerns, and strong domestic biotechnology innovation are driving adoption. Key players in the U.S. focus on cellulosic and algae-based fuels to achieve deeper emission reductions, leveraging policy support, research incentives, and advanced production technologies to scale operations.

Leading companies in the Global Advanced Biofuel Market include Advance Biofuel, Aemetis, Blue Biofuels, Borregaard, BP, Byogy Renewables, Chevron, Clariant, Enerkem, ExxonMobil, Gevo, GranBio, Green Plains, Galp, Indian Oil Corporation Limited, Logen, Praj Industries, Shell, TotalEnergies, and Votion Biorefineries. Key strategies employed by companies in the Global Advanced Biofuel Market to strengthen their presence include investing in R&D to improve conversion efficiency and feedstock utilization, forming joint ventures with agricultural and industrial partners to secure reliable biomass supply chains, and expanding production facilities globally to reduce delivery times and costs. Firms are leveraging government incentives, blending mandates, and sustainability certification programs to enhance market credibility. They are also deploying innovative process technologies for cellulosic ethanol and algae-based fuels to achieve higher yield and cost-effectiveness. Strategic acquisitions, partnerships, and licensing agreements enable companies to access new technologies, expand market reach, and accelerate commercialization.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Fuel type trends

- 2.4 Feedstock trends

- 2.5 Application trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Price trend analysis (USD/Tons)

- 3.6.1 By fuel type

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Fuel type, 2022 - 2035 (USD Million & MT)

- 5.1 Key trends

- 5.2 Cellulosic ethanol

- 5.3 Biodiesel

- 5.4 Biobutanol

- 5.5 Others

Chapter 6 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million & MT)

- 6.1 Key trends

- 6.2 Agriculture

- 6.3 Forestry

- 6.4 Waste

- 6.5 Others

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MT)

- 7.1 Key trends

- 7.2 Transportation

- 7.3 Aviation

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MT)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Spain

- 8.3.4 UK

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Indonesia

- 8.4.4 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Advance Biofuel

- 9.2 Aemetis

- 9.3 Blue Biofuels

- 9.4 Borregaard

- 9.5 BP

- 9.6 Byogy Renewables

- 9.7 Chevron

- 9.8 Clariant

- 9.9 Enerkem

- 9.10 ExxonMobil

- 9.11 Gevo

- 9.12 GranBio

- 9.13 Green Plains

- 9.14 Galp

- 9.15 Indian Oil Corporation Limited

- 9.16 Logen

- 9.17 Praj Industries

- 9.18 Shell

- 9.19 TotalEnergies

- 9.20 Votion Biorefineries

2026年全球先進生質燃料市場報告

2026年全球先進生質燃料市場報告 先進生質燃料市場:按類型、生產技術、原料類型和應用分類的先進生質燃料-2025-2032年全球預測

先進生質燃料市場:按類型、生產技術、原料類型和應用分類的先進生質燃料-2025-2032年全球預測 先進生質燃料市場-全球產業規模、佔有率、趨勢、機會及預測,依燃料類型、原料類型、加工技術、地區及競爭情況細分,2020-2030 年預測

先進生質燃料市場-全球產業規模、佔有率、趨勢、機會及預測,依燃料類型、原料類型、加工技術、地區及競爭情況細分,2020-2030 年預測 按燃料類型、原料、製程類型和地區分類的先進生質燃料市場

按燃料類型、原料、製程類型和地區分類的先進生質燃料市場 全球先進生質燃料市場

全球先進生質燃料市場 先進生質燃料市場規模、佔有率和成長分析(按發電、製程、燃料類型、原料、最終用途和地區)- 產業預測 2025-2032

先進生質燃料市場規模、佔有率和成長分析(按發電、製程、燃料類型、原料、最終用途和地區)- 產業預測 2025-2032 先進生質燃料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲先進生質燃料:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

先進生質燃料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲先進生質燃料:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)