|

市場調查報告書

商品編碼

1959642

血液處理及儲存設備市場機會、成長要素、產業趨勢分析及2026-2035年預測Blood Processing and Storage Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

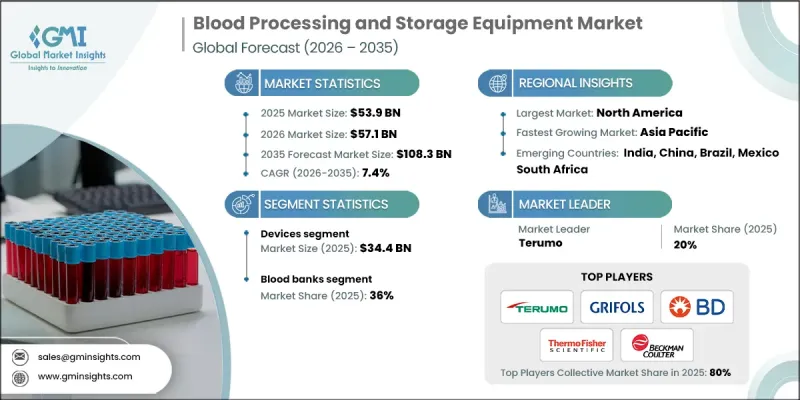

2025年全球血液處理和儲存設備市場價值為539億美元,預計到2035年將以7.4%的複合年成長率成長至1083億美元。

慢性病發病率上升、血液管理系統技術的不斷進步以及需要輸血的創傷相關急診病例增加,是推動市場擴張的主要因素。人們對自願捐血的認知不斷提高,也對產業成長起到了重要作用。政府主導的措施、醫療宣傳活動和非營利計畫正在加強全球捐血網路,從而提高了血液採集量。採集量的激增對可靠的基礎設施提出了更高的要求,包括先進的製冷系統、血漿儲存裝置、低溫冷凍庫以及相關耗材,以確保血液產品的完整性。現代化的設備能夠幫助醫療機構維持血液品質、簡化庫存管理並最大限度地減少產品損耗。隨著全球醫療系統將輸血安全和營運效率置於優先地位,對先進血液處理和儲存技術的投資正在加速,醫院和血液採集中心也積極建構擴充性且合規的血液管理框架。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 539億美元 |

| 預測金額 | 1083億美元 |

| 複合年成長率 | 7.4% |

血液處理和儲存設備包含一系列專門的醫療技術,旨在嚴格控制溫度和安全標準,對血液及其成分進行採集、分離、分析、儲存和管理。這些系統包括離心機、可控制冷系統、冷凍庫、過濾平台以及相關的處理技術,以確保輸血所需的無菌性,防止污染,並維持產品的有效性。精確的溫度控制和監測對於維持臨床標準、延長儲存期以及滿足監管合規要求至關重要。

預計到2025年,設備市場規模將達到344億美元,佔市佔率的63.8%。此類別包括專為血液採集、分離、儲存和監測而設計的高性能系統。血漿儲存設備、血庫冷藏系統、實驗室冷凍冷凍庫、低溫系統、快速冷凍設備、血型分析儀、熱療系統、血球比容離心機和自動化細胞處理設備等,構成了輸血服務的基礎。這些設備在整個處理和儲存週期內保護血液質量,並符合嚴格的安全標準。醫院、診斷檢查室和血液採集中心的需求不斷成長,推動了對技術先進、節能高效的設備平台的持續投資。

到2025年,血庫將佔據36%的市場佔有率,這反映了其在輸血醫學中的核心角色。血庫是血液製品採集、檢測、處理、儲存和分發的關鍵樞紐。為確保安全合規,這些機構依賴先進的冷凍系統、血漿儲存設備、低溫儲存方案和專業的離心技術。隨著外科手術的增加、急診醫療需求的成長以及慢性病管理項目的擴展,血液成分的需求不斷成長,血庫不得不擴大基礎設施,並部署能夠維持嚴格環境控制標準的下一代儲存系統。

預計到2025年,北美血液處理和儲存設備市場佔有率將達到40.5%,這得益於先進的醫療基礎設施和技術的快速普及。該地區擁有健全的法規結構、完善的輸血網路以及對醫療創新持續不斷的投資。持續成長的輸血治療和慢性病管理計畫需求,使得可靠的儲存和處理系統至關重要。高性能冷凍設備、低溫冷凍庫、細胞處理技術及相關耗材對於醫療機構維持合規性和保障病人安全至關重要。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 慢性病發生率呈上升趨勢

- 血液處理和儲存設備的技術進步

- 道路交通事故數量急劇增加。

- 人們對捐血的認知不斷提高

- 產業潛在風險與挑戰

- 血液處理設備高成本

- 嚴格的法規環境

- 市場機遇

- 在生物製藥和再生醫學領域不斷拓展應用。

- 促進因素

- 成長潛力分析

- 監管環境

- 技術進步

- 當前技術趨勢

- 新興技術

- 2024年價格分析

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 合作夥伴關係和合資企業

- 新產品發布

- 擴張計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 裝置

- 等離子冷凍庫

- 血庫用冷藏庫

- 實驗室冷藏庫

- 實驗室冷凍庫

- 超低溫冷凍庫

- 快速冷凍庫

- 血型鑑定裝置

- 保溫器

- 血球容積比離心機

- 細胞處理裝置

- 消耗品

- 輸血包

- 血袋

- 採血針

- 採血管

- 血液過濾器

- 採血採血針

- 血型檢測試劑

- 血液凝固試劑

- 血液學試劑

- 其他消耗品

第6章 市場估算與預測:依最終用途分類,2022-2035年

- 血庫

- 診斷檢查室

- 醫院和診所

- 其他最終用戶

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第8章:公司簡介

- Beckman Coulter, Inc.

- Thermogenesis Holdings, Inc.

- Maco Pharma International GmbH

- Immucor, Inc.

- Becton, Dickinson and Company

- Bio-Rad Laboratories, Inc.

- Grifols, SA

- Abbott Laboratories

- Sigma Laborzentrifugen GmbH

- Terumo BCT, Inc.

- Poly Medicure Ltd

- Thermo Fisher Scientific, Inc.

- Biomerieux

- F. Hoffmann-La Roche Ltd

The Global Blood Processing and Storage Equipment Market was valued at USD 53.9 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 108.3 billion by 2035.

Market expansion is supported by the growing burden of chronic diseases, continuous technological progress in blood management systems, and a rising number of trauma-related emergencies requiring transfusions. Increasing awareness surrounding voluntary blood donation is also playing a critical role in shaping industry growth. Government-led initiatives, healthcare campaigns, and nonprofit programs are strengthening donation networks worldwide, resulting in higher blood collection volumes. This surge in collection requires reliable infrastructure, including advanced refrigeration systems, plasma storage units, ultralow temperature freezers, and supporting consumables to maintain product integrity. Modern equipment enables healthcare facilities to preserve blood quality, streamline inventory management, and minimize product loss. As global healthcare systems prioritize transfusion safety and operational efficiency, investments in advanced blood processing and storage technologies are accelerating, reinforcing the development of scalable and compliant blood management frameworks across hospitals and collection centers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.9 Billion |

| Forecast Value | $108.3 Billion |

| CAGR | 7.4% |

Blood processing and storage equipment comprises specialized medical technologies designed to collect, separate, analyze, preserve, and manage blood and its components under tightly regulated temperature and safety parameters. These systems include centrifugation units, controlled refrigeration systems, deep freezers, filtration platforms, and related handling technologies that ensure sterility, prevent contamination, and maintain product viability for transfusion purposes. Precision temperature control and monitoring capabilities are essential to uphold clinical standards and extend shelf life while meeting regulatory compliance requirements.

The devices segment generated USD 34.4 billion in 2025, accounting for a 63.8% share. This category includes high-performance systems engineered for blood collection, separation, preservation, and monitoring. Equipment such as plasma storage units, blood bank refrigeration systems, laboratory-grade freezers, ultralow temperature systems, shock freezing units, blood grouping analyzers, warming systems, hematocrit centrifuges, and automated cell processors form the backbone of transfusion services. These devices safeguard blood quality throughout processing and storage cycles while meeting stringent safety benchmarks. Growing demand from hospitals, diagnostic laboratories, and blood collection centers continues to drive investments in technologically advanced and energy-efficient device platforms.

The blood banks segment held a 36% share in 2025, reflecting its central role in transfusion medicine. Blood banks function as primary hubs for the collection, testing, processing, storage, and distribution of blood products. To ensure safety and compliance, these facilities depend on advanced refrigeration systems, plasma preservation units, ultralow temperature storage solutions, and specialized centrifugation technologies. Rising surgical volumes, emergency care requirements, and chronic disease management programs are increasing demand for blood components, prompting blood banks to expand infrastructure and adopt next-generation storage systems capable of maintaining strict environmental control standards.

North America Blood Processing and Storage Equipment Market held 40.5% share in 2025, supported by its advanced healthcare infrastructure and rapid technology adoption. The region benefits from strong regulatory frameworks, well-established transfusion networks, and sustained investment in medical innovation. Continuous demand for transfusion therapies and chronic disease management programs requires dependable storage and processing systems. High-performance refrigeration units, ultralow temperature freezers, cell processing technologies, and supporting consumables are essential to maintain compliance and ensure patient safety across healthcare institutions.

Key companies operating in the Global Blood Processing and Storage Equipment Market include Thermo Fisher Scientific, Inc., Beckman Coulter, Inc., Grifols, Abbott Laboratories, Becton, Dickinson and Company, Terumo, F. Hoffmann-La Roche Ltd, Bio-Rad Laboratories, Inc., Maco Pharma International GmbH, Thermogenesis Holdings, Inc., Immucor, Inc., Sigma Laborzentrifugen, Poly Medicure Ltd, and Biomerieux. Companies in the Blood Processing and Storage Equipment Market are strengthening their competitive positioning through innovation, regulatory compliance, and global expansion strategies. Leading manufacturers are investing in energy-efficient refrigeration systems, automated processing platforms, and digital monitoring solutions that enhance traceability and quality control. Strategic partnerships with hospitals and blood collection networks help expand distribution reach and ensure recurring demand. Firms are also prioritizing research and development to introduce advanced temperature monitoring technologies and integrated data management systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Technological advancement in blood processing and storage equipment

- 3.2.1.3 Surge in the number of road traffic accidents

- 3.2.1.4 Growing awareness regarding blood donation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with blood processing devices

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Increased applications in biotherapy and regenerative medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Devices

- 5.2.1 Plasma freezers

- 5.2.2 Blood bank refrigerators

- 5.2.3 Lab refrigerators

- 5.2.4 Lab freezers

- 5.2.5 Ultralow temperature freezers

- 5.2.6 Shock freezers

- 5.2.7 Grouping analyzers

- 5.2.8 Warmers

- 5.2.9 Hematocrit centrifuges

- 5.2.10 Cell processors

- 5.3 Consumables

- 5.3.1 Blood administration sets

- 5.3.2 Blood bags

- 5.3.3 Blood collection needles

- 5.3.4 Blood collection tube

- 5.3.5 Blood filters

- 5.3.6 Blood lancets

- 5.3.7 Blood grouping reagents

- 5.3.8 Blood coagulation reagents

- 5.3.9 Hematology reagents

- 5.3.10 Other consumables

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Blood banks

- 6.3 Diagnostic laboratories

- 6.4 Hospitals & clinics

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Beckman Coulter, Inc.

- 8.2 Thermogenesis Holdings, Inc.

- 8.3 Maco Pharma International GmbH

- 8.4 Immucor, Inc.

- 8.5 Becton, Dickinson and Company

- 8.6 Bio-Rad Laboratories, Inc.

- 8.7 Grifols, S.A.

- 8.8 Abbott Laboratories

- 8.9 Sigma Laborzentrifugen GmbH

- 8.10 Terumo BCT, Inc.

- 8.11 Poly Medicure Ltd

- 8.12 Thermo Fisher Scientific, Inc.

- 8.13 Biomerieux

- 8.14 F. Hoffmann-La Roche Ltd

臍帶血處理產品市場:2026-2032年全球市場預測(依產品類型、處理方法、服務供應商、檢體類型、應用程式和最終用戶分類)臍帶血處理和儲存設備市場:按產品類型、技術、最終用戶和應用分類的全球市場預測,2026-2032年血液處理設備及耗材市場:按產品類型、技術、應用、最終用戶和分銷管道分類的全球市場預測,2026年至2032年血液處理用拋棄式產品市場:2026-2032年全球市場預測(依產品類型、血液成分、材料、應用、最終用戶和銷售管道)自動化血液處理設備市場:按產品類型、組件、操作模式、最終用戶和應用分類 - 全球預測(2026-2032 年)

臍帶血處理產品市場:2026-2032年全球市場預測(依產品類型、處理方法、服務供應商、檢體類型、應用程式和最終用戶分類)臍帶血處理和儲存設備市場:按產品類型、技術、最終用戶和應用分類的全球市場預測,2026-2032年血液處理設備及耗材市場:按產品類型、技術、應用、最終用戶和分銷管道分類的全球市場預測,2026年至2032年血液處理用拋棄式產品市場:2026-2032年全球市場預測(依產品類型、血液成分、材料、應用、最終用戶和銷售管道)自動化血液處理設備市場:按產品類型、組件、操作模式、最終用戶和應用分類 - 全球預測(2026-2032 年) 2026年全球血液處理設備及耗材市場報告2026年盧克血液分離機全球市場報告一次性冷凍袋市場:按冷凍袋材料、腔室數量、滅菌等級、容量、封口機制、應用和最終用戶分類,全球預測,2026-2032年血液處理和儲存設備市場(按產品類型、技術、最終用戶和分銷管道分類)—2026-2032年全球預測

2026年全球血液處理設備及耗材市場報告2026年盧克血液分離機全球市場報告一次性冷凍袋市場:按冷凍袋材料、腔室數量、滅菌等級、容量、封口機制、應用和最終用戶分類,全球預測,2026-2032年血液處理和儲存設備市場(按產品類型、技術、最終用戶和分銷管道分類)—2026-2032年全球預測 全球血液處理與儲存設備市場

全球血液處理與儲存設備市場