|

市場調查報告書

商品編碼

1959617

聚乙烯袋市場機會、成長要素、產業趨勢分析及2026年至2035年預測。Polybags Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

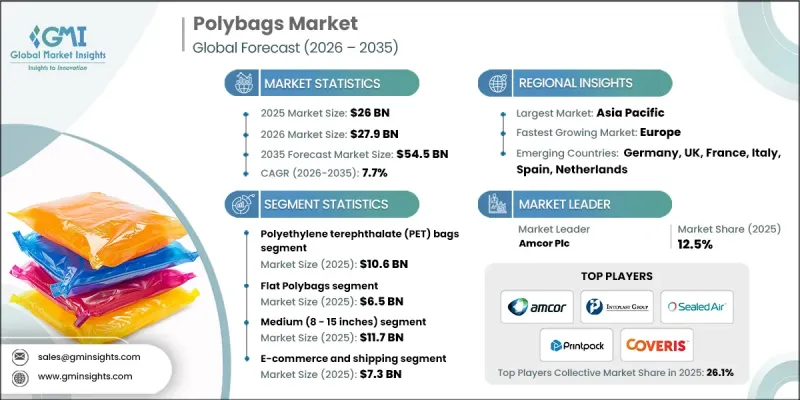

2025年全球塑膠袋市場價值為260億美元,預計2035年將達到545億美元,年複合成長率為7.7%。

聚乙烯袋主要由聚乙烯製成,是用途廣泛、靈活且便利的包裝解決方案,從家庭到工業領域都有應用。它們可用於儲存、運輸和保護貨物,其輕巧、耐用和經濟實惠的特性使其廣受歡迎。聚乙烯袋有透明和彩色兩種類型,採用低密度聚乙烯 (LDPE)、高密度聚苯乙烯(HDPE) 和線性低密度聚乙烯 (LLDPE) 等聚合物製造。強度、厚度和柔軟性取決於材料的品質。先進的擠出和吹塑成型技術是主流的生產流程,通常會添加添加劑以提高抗紫外線性能、印刷品質和機械耐久性。這些技術標準確保了聚乙烯袋性能的一致性和可靠性。聚乙烯袋用於包裝食品、消費品和服裝,可有效阻隔潮氣、灰塵和物理損傷。其低成本、便利性和廣泛的適用性持續推動全球市場的擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 260億美元 |

| 預測金額 | 545億美元 |

| 複合年成長率 | 7.7% |

預計到2025年,聚對苯二甲酸乙二醇酯(PET)包裝袋市場規模將達106億美元。 PET包裝袋以其高拉伸強度、透明度和抗張伸、抗收縮性能而著稱,深受需要耐用且外觀精美包裝的行業的青睞。它們在零售和食品行業,例如冷藏和冷凍食品包裝領域,尤其受歡迎。其他類型的聚乙烯包裝袋包括複合材料、層壓材料、生物分解性塑膠或專為滿足特定行業性能要求而設計的特殊薄膜。

預計到2025年,中型聚乙烯包裝袋(8-15吋)的市場規模將達到117億美元,佔據最大的市場佔有率。其尺寸適中,非常適合包裝消費品、文件、服裝和食品。中等尺寸既保證了充足的容量,又便於操作,因此特別適用於零售後的分銷、物流和電子商務應用。

預計到2025年,美國塑膠袋市場規模將達到59億美元。零售、電商和食品包裝行業的強勁成長,以及旨在減少一次性塑膠使用的法規,正在推動市場需求。永續性措施正在加速向可回收、可重複使用和生物基塑膠袋的轉變,尤其是在二級和三級包裝領域。物流和服飾包裝領域的高消耗量正在提振國內需求,而各州對塑膠袋的禁令和課稅則促使製造商開發可堆肥和環保的替代品。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 包裝產業需求增加

- 電子商務與物流的擴張

- 製造成本和材料成本低

- 產業潛在風險與挑戰

- 回收基礎設施的限制因素

- 原物料價格波動

- 市場機遇

- 開發可生物分解塑膠袋

- 製造業的技術進步

- 對客製化和品牌化的需求

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 材料

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估計與預測:依材料分類,2022-2035年

- 聚乙烯(PE)袋

- 聚丙烯(PP)袋

- 聚對苯二甲酸乙二醇酯(PET)袋

- 其他

第6章 市場估算與預測:依產品分類,2022-2035年

- 扁平塑膠袋

- 有側邊撐片的塑膠袋

- 自封式塑膠袋

- 帶孔塑膠袋

- 聚合物郵寄袋

- 氣泡郵袋

- 其他塑膠袋

第7章 市場規模估算與預測(2022-2035年)

- 小號(小於 8 吋)

- 中號(8-15吋)

- 大號(15吋或更大)

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 零售和包裝

- 小號(小於 8 英吋)

- 中號(8-15吋)

- 大號(15吋或更大)

- 食品包裝

- 小號(小於 8 吋)

- 中號(8-15吋)

- 大號(15吋或更大)

- 醫療保健

- 小號(小於 8 英吋)

- 中號(8-15吋)

- 大號(15吋或更大)

- 工業/製造業

- 小號(小於 8 吋)

- 中號(8-15吋)

- 大號(15吋或更大)

- 農業

- 小號(小於 8 英吋)

- 中號(8-15吋)

- 大號(15吋或更大)

- 電子商務和配送

- 小號(小於 8 英吋)

- 中號(8-15吋)

- 大號(15吋或更大)

- 其他

- 小號(小於 8 英吋)

- 中號(8-15吋)

- 大號(15吋或更大)

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Amcor Plc

- Sealed Air Corporation

- Novolex

- Coveris AG

- Inteplast Group

- Huhtamaki Group

- Printpack, Inc.

- Winpak Ltd.

- A-Pac Manufacturing Co., Inc.

- Arihant Packers

- PPC Flex

The Global Polybags Market was valued at USD 26 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 54.5 billion by 2035.

Polybags, primarily made from polyethylene, are versatile, flexible packaging solutions widely used across households and industries for the storage, transport, and protection of goods. Their lightweight, durable, and cost-effective nature makes them highly popular. Available in both transparent and colored variants, polybags are manufactured using polymers such as LDPE, HDPE, and LLDPE, with strength, thickness, and flexibility determined by material quality. Advanced extrusion and blowing techniques dominate manufacturing processes, often supplemented with additives to improve UV resistance, print quality, and machine durability. These technical standards ensure uniform performance and reliability. Polybags are used for packaging food, consumer products, and apparel, offering a barrier against moisture, dust, and physical damage. Their low cost, convenience, and wide applicability continue to drive market expansion globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26 Billion |

| Forecast Value | $54.5 Billion |

| CAGR | 7.7% |

The polyethylene terephthalate (PET) bags segment accounted for USD 10.6 billion in 2025. Known for high tensile strength, clarity, and resistance to stretching and shrinking, PET bags are favored in industries requiring durable and visually appealing packaging. They are particularly popular in retail and food sectors for applications including refrigerated and frozen goods. Other types of polybags include composite materials, laminates, biodegradable plastics, or specialty films designed to meet specific performance requirements in certain industries.

The medium-sized polybags, measuring 8 to 15 inches, generated USD 11.7 billion in 2025 and held the largest market share. Their balanced size makes them ideal for packaging consumer products, documents, apparel, and food items. The medium dimensions allow for convenient handling while offering sufficient capacity, making them especially suitable for post-retail, logistics, and e-commerce applications.

U.S. Polybags Market reached USD 5.9 billion in 2025. Demand is fueled by strong growth in retail, e-commerce, and food packaging sectors, alongside regulations aimed at reducing single-use plastics. Sustainability initiatives have prompted a shift toward recyclable, reusable, and biobased polybags, particularly in secondary and tertiary packaging. High consumption in logistics and apparel packaging reinforces domestic demand, while state-level bans and taxes on plastic bags push manufacturers to innovate with compostable and environmentally friendly alternatives.

Major companies operating in the Global Polybags Market include Novolex, Sealed Air Corporation, Winpak Ltd., Inteplast Group, A-Pac Manufacturing Co., Inc., Coveris AG, Huhtamaki Group, Printpack, Inc., Amcor Plc, PPC Flex, and Arihant Packers. Leading players in the polybags market focus on innovation, sustainability, and market expansion to strengthen their presence. Companies are investing in R&D to develop recyclable, biodegradable, and reusable packaging options that meet regulatory and consumer demands. Advanced material technologies enhance durability, flexibility, and print quality to differentiate products. Strategic partnerships with retailers and e-commerce platforms expand distribution networks, while competitive pricing supports adoption across diverse markets. Sustainability initiatives, branding, and marketing campaigns emphasize environmental responsibility and building consumer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material

- 2.2.2 Product

- 2.2.3 Size

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand from packaging industry

- 3.2.1.2 Expansion of e-commerce and logistics

- 3.2.1.3 Low manufacturing and material cost

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Recycling infrastructure limitations

- 3.2.2.2 Volatility in raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Development of biodegradable polybags

- 3.2.3.2 Technological advancements in manufacturing

- 3.2.3.3 Customization and branding demand

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene (PE) bags

- 5.3 Polypropylene (PP) bags

- 5.4 Polyethylene Terephthalate (PET) bags

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Product, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Flat polybags

- 6.3 Gusseted polybags

- 6.4 Ziplock polybags

- 6.5 Wicketed polybags

- 6.6 Poly mailers

- 6.7 Bubble mailers

- 6.8 Other polybags

Chapter 7 Market Estimates and Forecast, By Size, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Small (Below 8 Inches)

- 7.3 Medium (8 - 15 Inches)

- 7.4 Large (Above 15 Inches)

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Retail and packaging

- 8.2.1 Small (Below 8 Inches)

- 8.2.2 Medium (8 - 15 Inches)

- 8.2.3 Large (Above 15 Inches)

- 8.3 Food packaging

- 8.3.1 Small (Below 8 Inches)

- 8.3.2 Medium (8 - 15 Inches)

- 8.3.3 Large (Above 15 Inches)

- 8.4 Medical and healthcare

- 8.4.1 Small (Below 8 Inches)

- 8.4.2 Medium (8 - 15 Inches)

- 8.4.3 Large (Above 15 Inches)

- 8.5 Industrial and manufacturing

- 8.5.1 Small (Below 8 Inches)

- 8.5.2 Medium (8 - 15 Inches)

- 8.5.3 Large (Above 15 Inches)

- 8.6 Agriculture

- 8.6.1 Small (Below 8 Inches)

- 8.6.2 Medium (8 - 15 Inches)

- 8.6.3 Large (Above 15 Inches)

- 8.7 E-commerce and Shipping

- 8.7.1 Small (Below 8 Inches)

- 8.7.2 Medium (8 - 15 Inches)

- 8.7.3 Large (Above 15 Inches)

- 8.8 Others

- 8.8.1 Small (Below 8 Inches)

- 8.8.2 Medium (8 - 15 Inches)

- 8.8.3 Large (Above 15 Inches)

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Amcor Plc

- 10.2 Sealed Air Corporation

- 10.3 Novolex

- 10.4 Coveris AG

- 10.5 Inteplast Group

- 10.6 Huhtamaki Group

- 10.7 Printpack, Inc.

- 10.8 Winpak Ltd.

- 10.9 A-Pac Manufacturing Co., Inc.

- 10.10 Arihant Packers

- 10.11 PPC Flex

全球聚乙烯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚乙烯市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球聚乙烯市場

2026-2030年全球聚乙烯市場 2026年生物基聚乙烯全球市場報告聚乙烯市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測全球聚乙烯(PE)蠟市場規模、佔有率、趨勢和成長分析報告:2026-2034年

2026年生物基聚乙烯全球市場報告聚乙烯市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測全球聚乙烯(PE)蠟市場規模、佔有率、趨勢和成長分析報告:2026-2034年 聚乙烯市場:依產品類型、回收製程、應用和最終用戶分類-2026-2032年全球市場預測

聚乙烯市場:依產品類型、回收製程、應用和最終用戶分類-2026-2032年全球市場預測 聚乙烯(PE)母粒市場規模、佔有率和成長分析:按產品類型、載體樹脂等級、加工方法、最終用途產業和地區分類-2026-2033年產業預測

聚乙烯(PE)母粒市場規模、佔有率和成長分析:按產品類型、載體樹脂等級、加工方法、最終用途產業和地區分類-2026-2033年產業預測 聚乙烯市場規模、佔有率和趨勢分析報告:按產品、應用、最終用途、地區和細分市場分類(2026-2033 年)全球生物基聚乙烯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球供水聚乙烯(PE)管線市場報告

聚乙烯市場規模、佔有率和趨勢分析報告:按產品、應用、最終用途、地區和細分市場分類(2026-2033 年)全球生物基聚乙烯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球供水聚乙烯(PE)管線市場報告