|

市場調查報告書

商品編碼

1959615

住宅電氣管道市場機會、成長要素、產業趨勢分析及2026年至2035年預測Residential Electrical Conduit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

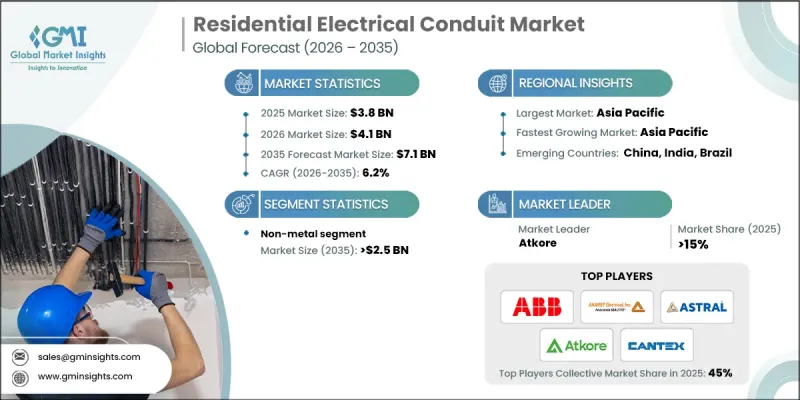

2025 年全球住宅電線導管市場價值為 38 億美元,預計到 2035 年將達到 71 億美元,年複合成長率為 6.2%。

這一成長主要得益於住宅電氣化、家用電動車充電的日益普及以及住宅中低壓電路和保護電氣管槽的廣泛應用。個人電動車充電器的普及推動了對車庫、車道和屋頂等場所新增分支電路、導管和符合標準的安裝的需求。節能型住宅維修,例如熱泵、電磁爐和改進的隔熱材料,進一步提升了對管道和電纜管理的需求。分散式屋頂太陽能發電和電錶後能源儲存系統為住宅佈線開闢了新的路徑,增加了對耐用導管和配件的需求。歐洲更嚴格的建築法規、加拿大的強制性維修以及英國住宅住宅脫碳舉措也在加速市場普及。隨著屋主和建築商將安全、能源效率和麵向未來的電氣基礎設施放在首位,全球對高品質住宅導管、彎頭和膨脹接頭的需求持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 38億美元 |

| 預測金額 | 71億美元 |

| 複合年成長率 | 6.2% |

預計到2025年,非金屬管道市場將佔據34.6%的市場佔有率,到2035年市場規模將達到25億美元。非金屬管道,例如PVC和認證聚合物系統,因其耐腐蝕、輕量和經濟高效等優點,尤其在潮濕和沿海地區備受青睞。這些管道簡化了安裝,降低了人事費用,並為現代住宅設計增添了簡潔美觀的視覺效果,同時易於切割、溶劑焊接,並適用於長距離管道鋪設。其優異的介電和熱性能使其能夠滿足屋頂太陽能發電系統、游泳池系統和灌溉設施等戶外迴路的需求。對紫外線穩定配件、黏合劑和套管等配件日益成長的需求,為經銷商和承包商提供了穩定的收入來源。

隨著電氣化計劃的推進,對1 1/4吋至2吋導管的需求不斷成長。這是因為二級電動車充電器、熱泵和電磁爐等設備需要更高電流容量、更強散熱性能和麵向未來的佈線路徑的導線。承包商正在車庫、屋頂和室外安裝空間擴容導管,以容納備用線路、負載管理設備和未來的儲能設施,從而最佳化填充密度、熱性能和勞動生產率。這種做法導致每個計劃的導管用量增加、配件使用量增加以及彎頭和直管體等部件的標準化,進而增加了批發商和承包商對中型導管的需求。

預計2025年,美國住宅電線導管市場規模將達5.614億美元。市場擴張的主要驅動力是電氣化維修、電動車充電樁安裝、熱泵部署、屋頂太陽能發電系統以及相關服務升級。這些活動增加了導管的長度和直徑需求,並提高了配件的使用率,從而為供應商和安裝商拓展業務創造了機會。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 電線導管成本結構分析

- 新機會和趨勢

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 戰略儀錶板

- 策略舉措

- 重要合作夥伴關係和合作

- 主要併購活動

- 產品創新和新產品發布

- 市場擴大策略

- 競爭性標竿分析

- 創新與永續發展趨勢

第5章 市場規模及預測:以交易量計算,2022-2035年

- 1/2~1

- 1又1/4到2

- 2.5~3

- 3~4

- 5~6

- 其他

第6章 市場規模及預測:依分類,2022-2035年

- 金屬

- 非金屬

- 靈活的

- 地下

- 其他

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 法國

- 德國

- 義大利

- 英國

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第8章:公司簡介

- ABB

- Anamet Electrical

- Astral

- Atkore

- Austro Pipes

- CANTEX

- Champion Fiberglass

- Electri-Flex

- Guangdong Ctube Industry

- HellermannTyton

- Hubbell

- IPEX Electrical

- JM Eagle

- Legrand

- Liberty Electric Products

- Robroy Industries

- Schneider Electric

- Tubecon

- Wienerberger

- Zekelman Industries

The Global Residential Electrical Conduit Market was valued at USD 3.8 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 7.1 billion by 2035.

The growth is driven by the electrification of homes, increased adoption of at-home EV charging, and rising deployment of low-voltage circuits and protective raceways in residential properties. The proliferation of private EV chargers is fueling demand for additional branch circuits, conduits, and code-compliant installations in garages, driveways, and rooftops. Energy-efficient home upgrades, including heat pumps, induction appliances, and improved insulation, are further boosting conduit and cable management requirements. Distributed rooftop solar and behind-the-meter energy storage systems are creating additional pathways for residential wiring, increasing the need for durable conduit and fittings. Stricter building policies in Europe, retrofitting mandates in Canada, and initiatives to decarbonize social housing in the UK are further accelerating market adoption. As homeowners and builders prioritize safety, energy efficiency, and future-ready electrical infrastructure, demand for high-quality residential conduits, elbows, and expansion fittings continues to rise globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.8 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 6.2% |

The non-metallic segment captured a 34.6% share in 2025 and is expected to reach USD 2.5 billion by 2035. Non-metallic conduits, such as PVC and listed polymer systems, are preferred for their corrosion resistance, lightweight design, and cost efficiency, particularly in moisture-prone or coastal regions. These conduits simplify installation with easy cutting, solvent welding, and long-sweep runs, reducing labor costs while providing a clean aesthetic for modern residential designs. Their dielectric and thermal properties support outdoor circuits for rooftop PV, pool systems, and irrigation. Rising demand for accessories such as UV-stabilized fittings, adhesives, and bushings ensures consistent revenue streams for distributors and contractors.

The electrification projects are increasingly driving demand for 11/4-2 inch conduits, as Level 2 EV chargers, heat pumps, and induction appliances require higher ampacity conductors, enhanced heat dissipation, and future-ready pathways. Installers are upsizing runs in garages, rooftops, and exterior pads to accommodate spares, load management hardware, and potential energy storage, optimizing fill, thermal performance, and labor productivity. This practice also boosts conduit footage per project, increases fitting counts, and standardizes components like elbows and LB bodies, strengthening mid-size conduit pull-through for wholesalers and contractors.

U.S. Residential Electrical Conduit Market was valued at USD 561.4 million in 2025. Market expansion is largely fueled by electrification retrofits, EV charger installations, heat pump deployment, rooftop PV systems, and related service upgrades. These activities increase conduit footage, diameter requirements, and accessory utilization, creating opportunities for suppliers and installers to scale their operations.

Major companies in the Global Residential Electrical Conduit Market include Anamet Electrical, ABB, Astral, Atkore, Austro Pipes, CANTEX, Champion Fiberglass, Electri-Flex, Guangdong Ctube Industry, HellermannTyton, Hubbell, IPEX Electrical, JM Eagle, Legrand, Liberty Electric Products, Robroy Industries, Schneider Electric, Tubecon, Wienerberger, and Zekelman Industries. Companies in the residential electrical conduit market are strengthening their presence through several key strategies. They are investing in research and development to introduce conduits with enhanced durability, heat resistance, and corrosion protection. Expansion of distribution networks ensures timely delivery to contractors, builders, and wholesalers. Strategic partnerships with construction firms and electrical contractors enable integrated project support. Product standardization, modular fittings, and UV-stabilized accessories improve labor efficiency and adoption rates. Firms are also focusing on sustainability by developing recyclable and environmentally friendly materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Trade size trends

- 2.1.3 Classification trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of electrical conduits

- 3.8 Emerging opportunities & trends

- 3.9 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Trade Size, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 1/2 to 1

- 5.3 1 1/4 to 2

- 5.4 2 1/2 to 3

- 5.5 3 to 4

- 5.6 5 to 6

- 5.7 Others

Chapter 6 Market Size and Forecast, By Classification, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Non-metal

- 6.4 Flexible

- 6.5 Underground

- 6.6 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 France

- 7.3.2 Germany

- 7.3.3 Italy

- 7.3.4 UK

- 7.3.5 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Anamet Electrical

- 8.3 Astral

- 8.4 Atkore

- 8.5 Austro Pipes

- 8.6 CANTEX

- 8.7 Champion Fiberglass

- 8.8 Electri-Flex

- 8.9 Guangdong Ctube Industry

- 8.10 HellermannTyton

- 8.11 Hubbell

- 8.12 IPEX Electrical

- 8.13 JM Eagle

- 8.14 Legrand

- 8.15 Liberty Electric Products

- 8.16 Robroy Industries

- 8.17 Schneider Electric

- 8.18 Tubecon

- 8.19 Wienerberger

- 8.20 Zekelman Industries

磁性數據電纜市場報告:趨勢、預測和競爭分析(至2035年)

磁性數據電纜市場報告:趨勢、預測和競爭分析(至2035年) 軟性扁平電纜市場:依產品類型、材質、導體數量、間距尺寸、寬度及最終用途產業分類-2026-2032年全球市場預測音影片線市場:2026-2032年全球市場預測(依產品類型、線長、應用、最終用戶及通路分類)塑膠導管市場:按類型、材料、產業、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2026-2033 年)

軟性扁平電纜市場:依產品類型、材質、導體數量、間距尺寸、寬度及最終用途產業分類-2026-2032年全球市場預測音影片線市場:2026-2032年全球市場預測(依產品類型、線長、應用、最終用戶及通路分類)塑膠導管市場:按類型、材料、產業、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2026-2033 年) Thunderbolt 數據線市場分析及預測(至 2035 年):按類型、產品類型、技術、應用、材質、設備、最終用戶、功能、安裝類型和解決方案分類

Thunderbolt 數據線市場分析及預測(至 2035 年):按類型、產品類型、技術、應用、材質、設備、最終用戶、功能、安裝類型和解決方案分類 全球軟性電氣管道市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球中型金屬導管市場:按應用、最終用途、產品類型、交易規模、分銷管道、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032)

全球軟性電氣管道市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球中型金屬導管市場:按應用、最終用途、產品類型、交易規模、分銷管道、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032) 2026年全球非金屬預接線導管市場報告ITC測量電纜全球市場報告(2026年)6類屏蔽雙絞線市場(依導體材料、線對數、安裝方式、產品類型、屏蔽方式及最終用戶分類),全球預測,2026-2032年

2026年全球非金屬預接線導管市場報告ITC測量電纜全球市場報告(2026年)6類屏蔽雙絞線市場(依導體材料、線對數、安裝方式、產品類型、屏蔽方式及最終用戶分類),全球預測,2026-2032年