|

市場調查報告書

商品編碼

1959612

抗發炎藥物市場機會、成長要素、產業趨勢分析及2026年至2035年預測Anti-inflammatory Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

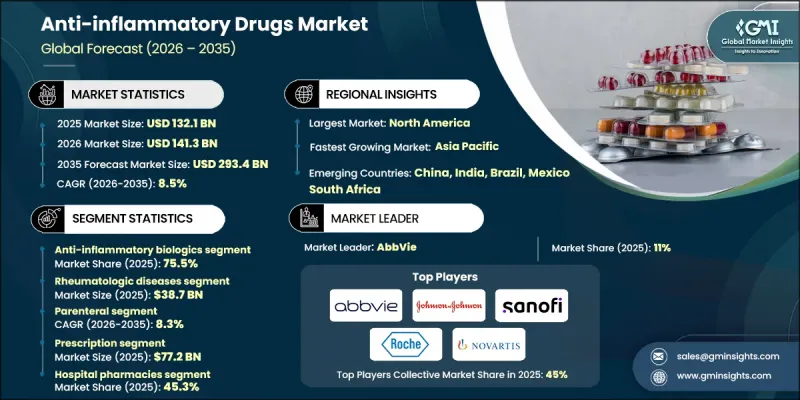

2025 年全球抗發炎藥物市場價值 1,321 億美元,預計到 2035 年將達到 2,934 億美元,年複合成長率為 8.5%。

免疫學研究和分子科學的持續進步推動了市場成長,從而促進了更精準、更有效治療方法的開發。治療方法正穩步從傳統的非類固醇消炎劑(NSAIDs) 和皮質類固醇轉向生物目標、單株抗體和先進的小分子抑制劑。這些創新正在改善疾病管理,減少副作用,並為患者帶來更好的長期治療效果。該市場透過多種治療層級,針對多種急性和慢性發炎性疾病,旨在控制發炎、緩解症狀和延緩疾病進展。強力的健保報銷機制和對免疫標靶藥物研發的持續投入正在推動治療方法的廣泛應用。口服療法、緩釋注射劑和低頻給藥生物製藥等先進給藥平台的出現,提高了患者的用藥便利性和依從性。整體而言,在創新法規環境和不斷擴展的臨床研發管線的支持下,市場正朝著以患者為中心、以精準醫療為基礎的療法方向發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 1321億美元 |

| 預測金額 | 2934億美元 |

| 複合年成長率 | 8.5% |

預計到2025年,抗發炎生物製藥市場佔有率將達到75.5%,並在2026年至2035年間以8.6%的複合年成長率成長。其主導地位得益於其高臨床療效、對發炎路徑的選擇性標靶化以及對中重度疾病的有效治療。這些治療方法在高級治療中備受青睞,因為它們既能緩解症狀,又能緩解疾病。

預計到2025年,處方藥市場銷售額將達到772億美元,繼續維持其主導地位。處方藥治療方法對於需要醫生監督和特殊治療通訊協定的發炎性和自體免疫疾病的長期管理仍然至關重要。生物製藥和標靶口服藥物的廣泛應用,以及健全的醫保報銷體系和以醫院為中心的配送網路,都將繼續支持該市場的發展。

預計到2025年,北美抗發炎藥市場將佔據全球39.1%的佔有率,從而推動全球需求成長。高疾病盛行率、完善的醫療保健基礎設施、早期獲得創新療法的機會以及有利的報銷政策,都支撐著該市場的強勁發展。持續的臨床研究活動和實力雄厚的製藥公司進一步鞏固了該地區的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 慢性發炎性疾病和自體免疫疾病的盛行率增加

- 標靶免疫學和生物製藥研發的進展

- 支持性的監管途徑和快速核准

- 公眾意識提高、診斷率提高、以及獲得專科醫療服務的途徑擴大。

- 產業潛在風險與挑戰

- 高昂的醫療成本和對長期經濟永續性的擔憂

- 安全隱憂和長期耐受性風險

- 市場機遇

- 新一代口服療法和更方便的患者體驗

- 生物相似藥和聯合治療的生命週期管理

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 未來市場趨勢

- 價格分析

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估計與預測:依藥物類別分類,2022-2035年

- 抗發炎生物製藥

- 非類固醇消炎劑(NSAIDs)

- 皮質類固醇

- 其他藥物分類

第6章 市場估計與預測:依適應症分類,2022-2035年

- 風濕性疾病

- 類風濕性關節炎

- 骨關節炎

- 乾癬性關節炎

- 僵直性脊椎炎

- 其他發炎性關節炎

- 皮膚病

- 銀屑病

- 異位性皮膚炎

- 化膿性汗腺炎

- 其他發炎性皮膚病

- 消化系統疾病

- 發炎性腸道疾病(IBD)

- 嗜伊紅性食道炎

- 其他發炎性消化系統疾病

- 呼吸系統疾病

- 氣喘

- 慢性阻塞性肺病(COPD)

- 過敏性鼻炎

- 其他發炎性呼吸系統疾病

- 神經系統疾病

- 其他跡象

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 外用

- 注射藥物

- 其他給藥途徑

第8章 市場估算與預測:依類型分類,2022-2035年

- 處方箋

- 非處方藥

第9章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- AbbVie

- Abbott Laboratories

- AbbVie

- Amgen

- AstraZeneca

- Bristol-Myers Squibb

- Eli Lilly and Company

- GlaxoSmithKline

- Hoffmann-La Roche

- Johnson &Johnson

- Merck &Co.

- Novartis

- Pfizer

- Sanofi

- Sun Pharmaceutical Industries

- Teva Pharmaceutical

- UCB

The Global Anti-Inflammatory Drugs Market was valued at USD 132.1 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 293.4 billion by 2035.

Market growth is supported by continued progress in immunology research and molecular science, which is enabling the development of more precise and effective therapies. Treatment approaches are steadily shifting away from traditional nonsteroidal anti-inflammatory drugs and corticosteroids toward targeted biologics, monoclonal antibodies, and advanced small-molecule inhibitors. These innovations are improving disease control, reducing side effects, and delivering better long-term outcomes for patients. The market addresses a wide spectrum of acute and chronic inflammatory conditions through multiple therapeutic classes designed to manage inflammation, ease symptoms, and slow disease progression. Strong reimbursement structures and sustained investment in immune-focused drug discovery are reinforcing adoption. Emerging oral therapies and advanced delivery platforms, including extended-duration injectables and less frequent dosing biologics, are enhancing patient convenience and adherence. Overall, the market is evolving toward precision-based, patient-focused treatments supported by innovation-friendly regulatory environments and expanding clinical pipelines.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $132.1 Billion |

| Forecast Value | $293.4 Billion |

| CAGR | 8.5% |

The anti-inflammatory biologics segment accounted for 75.5% share in 2025 and is expected to grow at a CAGR of 8.6% during 2026-2035. Their leadership position is driven by high clinical effectiveness, selective targeting of inflammatory pathways, and their ability to manage moderate to severe disease states. These therapies deliver both symptom relief and long-term disease modification, making them a preferred option in advanced treatment settings.

The prescription segment generated USD 77.2 billion in 2025, maintaining its dominant position. Prescription-based therapies remain essential for long-term management of inflammatory and autoimmune conditions that require physician supervision and specialized treatment protocols. Broad uptake of biologics and targeted oral drugs, combined with strong reimbursement and hospital-centered distribution, continues to support this segment.

North America Anti-inflammatory Drugs Market held a share of 39.1% in 2025, leading global demand. Market strength is supported by high disease prevalence, well-developed healthcare infrastructure, early access to innovative therapies, and favorable reimbursement policies. Ongoing clinical research activity and a strong pharmaceutical presence further reinforce the region's leadership.

Key companies operating in the Global Anti-inflammatory Drugs Market include Pfizer, AbbVie, Johnson & Johnson, Novartis, Sanofi, AstraZeneca, Eli Lilly and Company, Bristol-Myers Squibb, Amgen, Hoffmann-La Roche, Merck & Co., GlaxoSmithKline, UCB, Abbott Laboratories, Teva Pharmaceutical, and Sun Pharmaceutical. Companies in the anti-inflammatory drugs market are strengthening their competitive position through sustained investment in research and development, particularly in targeted therapies and next-generation biologics. Many players are expanding their pipelines through strategic collaborations, licensing agreements, and acquisitions to access novel mechanisms of action. The focus on oral formulations and long-acting delivery systems is improving patient adherence and market reach. Firms are also prioritizing geographic expansion in high-growth regions while securing strong reimbursement positioning in mature markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Treatment trends

- 2.2.4 Route of administration trends

- 2.2.5 Type trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic inflammatory and autoimmune diseases

- 3.2.1.2 Advancements in targeted immunology and biologic drug development

- 3.2.1.3 Supportive regulatory pathways and accelerated approvals

- 3.2.1.4 Rising awareness, diagnosis rates, and access to specialty care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs and long-term affordability concerns

- 3.2.2.2 Safety concerns and long-term tolerability risks

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation oral therapies and improved patient convenience

- 3.2.3.2 Lifecycle management through biosimilars and combination therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pricing analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Anti-inflammatory biologics

- 5.3 Nonsteroidal anti inflammatory drugs (NSAIDS)

- 5.4 Corticosteroids

- 5.5 Other drug classes

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Rheumatologic diseases

- 6.2.1 Rheumatoid arthritis

- 6.2.2 Osteoarthritis

- 6.2.3 Psoriatic arthritis

- 6.2.4 Ankylosing spondylitis

- 6.2.5 Other inflammatory arthritis

- 6.3 Dermatological diseases

- 6.3.1 Psoriasis

- 6.3.2 Atopic dermatitis

- 6.3.3 Hidradenitis suppurativa

- 6.3.4 Other inflammatory skin diseases

- 6.4 Gastrointestinal diseases

- 6.4.1 Inflammatory bowel disease (IBD)

- 6.4.2 Eosinophilic esophagitis

- 6.4.3 Other inflammatory GI disorders

- 6.5 Respiratory diseases

- 6.5.1 Asthma

- 6.5.2 Chronic obstructive pulmonary disease (COPD)

- 6.5.3 Allergic rhinitis

- 6.5.4 Other inflammatory respiratory diseases

- 6.6 Neurological disorders

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Topical

- 7.4 Injectable

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Prescription

- 8.3 Over the counter (OTC)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Abbott Laboratories

- 11.3 AbbVie

- 11.4 Amgen

- 11.5 AstraZeneca

- 11.6 Bristol-Myers Squibb

- 11.7 Eli Lilly and Company

- 11.8 GlaxoSmithKline

- 11.9 Hoffmann-La Roche

- 11.10 Johnson & Johnson

- 11.11 Merck & Co.

- 11.12 Novartis

- 11.13 Pfizer

- 11.14 Sanofi

- 11.15 Sun Pharmaceutical Industries

- 11.16 Teva Pharmaceutical

- 11.17 UCB

非類固醇消炎劑(NSAIDs)市場規模、佔有率和成長分析:按藥物類型、給藥途徑、應用、分銷管道、最終用戶、劑型和地區分類 - 產業預測,2026-2033年

非類固醇消炎劑(NSAIDs)市場規模、佔有率和成長分析:按藥物類型、給藥途徑、應用、分銷管道、最終用戶、劑型和地區分類 - 產業預測,2026-2033年 非類固醇消炎劑市場:2026-2032年全球市場預測(依藥物類別、劑型、給藥途徑、處方狀態、上市方式、病患群體、適應症、最終用戶和分銷管道分類)

非類固醇消炎劑市場:2026-2032年全球市場預測(依藥物類別、劑型、給藥途徑、處方狀態、上市方式、病患群體、適應症、最終用戶和分銷管道分類) Mometasone市場:依劑型、適應症、給藥途徑、通路及地區分類。抗發炎治療市場:2026-2032年全球市場預測(依治療分類、作用機制、給藥途徑、適應症、通路及最終用戶分類)

Mometasone市場:依劑型、適應症、給藥途徑、通路及地區分類。抗發炎治療市場:2026-2032年全球市場預測(依治療分類、作用機制、給藥途徑、適應症、通路及最終用戶分類) 全球抗發炎治療藥物市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球抗發炎治療藥物市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 抗發炎治療市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、最終用戶、組件、部署模式、解決方案、開發階段全球牙科抗發炎藥物市場(按藥物分類、給藥途徑、劑型、應用、最終用途和分銷管道分類)預測(2026-2032年)類固醇MRA市場按產品類型、適應症、給藥途徑、最終用戶和分銷管道分類-2026-2032年全球預測

抗發炎治療市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、最終用戶、組件、部署模式、解決方案、開發階段全球牙科抗發炎藥物市場(按藥物分類、給藥途徑、劑型、應用、最終用途和分銷管道分類)預測(2026-2032年)類固醇MRA市場按產品類型、適應症、給藥途徑、最終用戶和分銷管道分類-2026-2032年全球預測 抗發炎治療藥物市場規模、佔有率和成長分析(按藥物類別、適應症、用途、通路和地區分類)-2026-2033年產業預測

抗發炎治療藥物市場規模、佔有率和成長分析(按藥物類別、適應症、用途、通路和地區分類)-2026-2033年產業預測 非類固醇抗發炎藥市場規模及預測(2021-2031年),全球及區域佔有率、趨勢和成長機會分析報告涵蓋:藥物類別、給藥途徑、適應症、配銷通路和地理

非類固醇抗發炎藥市場規模及預測(2021-2031年),全球及區域佔有率、趨勢和成長機會分析報告涵蓋:藥物類別、給藥途徑、適應症、配銷通路和地理