|

市場調查報告書

商品編碼

1959609

軍事及國防半導體市場機會、成長要素、產業趨勢分析及2026年至2035年預測Military and Defense Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球軍用和國防半導體市場價值 129 億美元,預計到 2035 年將達到 366 億美元,年複合成長率為 11.2%。

隨著世界各國政府將增加國防費用和確保技術優勢列為優先事項,該市場展現出強勁的成長動能。預算撥款的增加正在加速先進半導體解決方案的研發和部署,這些解決方案應用於通訊網路、資訊系統、雷達平台、電子戰和精確導引系統等領域。現代國防基礎設施越來越依賴高效能半導體組件,以實現高速資料處理、安全連接、即時分析和系統互通性。用於軍事和國防應用的半導體是具有可控導電性的關鍵電子材料,是微處理器、積體電路、感測器和電源管理裝置的基礎。這些組件對於先進國防電子設備的性能、效率和可靠性至關重要。隨著各國軍隊不斷提升其空中、陸地、海洋和太空能力,對穩健、安全且節能的半導體技術的需求持續成長,從而支撐著全球國防生態系統中半導體市場的長期持續擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 129億美元 |

| 預測金額 | 366億美元 |

| 複合年成長率 | 11.2% |

另一方面,出口限制和地緣政治緊張局勢為軍工半導體市場帶來了結構性挑戰。嚴格的貿易法規和國家安全政策限制了敏感技術的跨境轉移,阻礙了全球供應鏈的柔軟性。各國政府正在實施保障措施以保護其戰略半導體能力,這可能導致採購週期延長和採購受限。地緣政治的不確定性進一步加劇了供應鏈的波動性,使得本地生產和安全的供應來源對國防應用日益重要。

預計到2025年,陸地系統市場規模將達到58億美元,並在2026年至2035年間以11.8%的複合年成長率成長。隨著國防機構將自主導航、先進感測和安全通訊技術整合到戰術系統中,地面平台的半導體整合度也不斷提高。即時數據處理、任務協調和容錯通訊網路是推動該領域半導體應用的關鍵需求。在惡劣環境下,對耐用、低功耗和高可靠性組件的需求,確保了作戰的連續性,這也再次凸顯了專為陸基軍事應用設計的專用半導體裝置的重要性。

預計到2025年,處理器和微控制器市佔率將達到28.9%。國防平台對高效能運算日益成長的需求正在加速先進處理技術的應用。現代國防系統需要嵌入式智慧、加密、安全通訊和人工智慧驅動的分析功能,而這些功能都由先進的處理器提供支援。此外,穩健且節能的微控制器正擴大應用於緊湊型國防電子設備、無人系統和攜帶式軍事裝備。這些技術能夠提升多個關鍵任務應用的指揮控制、自動化和作戰效率。

預計到2025年,北美軍工半導體市場將佔據45.1%的全球佔有率。空中、陸地、海上和太空平台的持續現代化計畫支撐了該地區的成長。對人工智慧、自主系統、網路安全和先進通訊基礎設施日益成長的關注,也持續推動對高效能半導體技術的需求。定期的升級、系統維修和維護計劃也為長期採購活動提供了支援。此外,政府為加強國內半導體製造能力所做的努力,正在增強區域自主性,並降低對外國供應商關鍵國防零件的依賴。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 政府增加對軍事領域的投資

- 利用耐輻射半導體元件

- 飛機升級和現代化計劃的增加

- 對先進半導體技術的需求不斷成長

- 擴大人工智慧(AI)和機器學習(ML)在軍事行動中的應用

- 產業潛在風險與挑戰

- 高成本,開發週期長

- 出口限制和地緣政治緊張局勢

- 市場機遇

- 電子戰和通訊系統的進步

- 用於國防模擬和指揮系統的高效能運算

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 國防預算分析

- 全球國防費用趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要國防現代化項目

- 預算預測(2025-2034 年)

- 對產業成長的影響

- 國防預算

- 按部門分類的國防預算分配

- 人員

- 運作/維護

- 採購

- 研究與發展/測試與評估

- 基礎設施和建築

- 技術與創新

- 供應鏈韌性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 併購和策略聯盟的趨勢

- 風險評估與管理

- 重大合約授予情況(2022-2025 年)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年重大發展

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 處理器和微控制器

- 通用處理器

- 人工智慧/機器學習處理器

- 加密處理器

- 數位訊號處理器

- 微控制器

- 儲存裝置

- 靜態隨機存取記憶體(SRAM)

- DRAM(動態隨機存取記憶體)

- 快閃記憶體(NAND、NOR)

- 磁阻記憶體(MRAM)

- EEPROM/NVRAM

- 邏輯裝置

- ASIC(專用積體電路)

- FPGA(現場可程式化閘陣列)

- PLD(可程式邏輯裝置)

- CPLD(複雜可程式邏輯裝置)

- 射頻和微波組件

- MMIC(單晶微波積體電路)

- 收發模組(T/R模組)

- 射頻功率放大器

- 其他

- 電源管理積體電路

- DC-DC轉換器(降壓型、升壓型、降壓/升壓型、隔離型)

- LDO(低壓差穩壓器)

- 功率 MOSFET 和閘極驅動器

- 其他

- 類比和混合訊號積體電路

- 運算放大器

- 比較器

- 類比開關和多工器

- 其他

- 資料轉換器(ADC/DAC)

- 光電子學

- 離散半導體

- 其他

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 陸基系統

- 作戰車輛(戰車、步兵戰車、裝甲運兵車)

- 戰術車輛(悍馬、防地雷反伏擊車、卡車)

- 火砲系統

- 地面防空系統

- 其他

- 海軍系統

- 水面作戰艦艇

- 航空母艦

- 潛水艇

- 兩棲船

- 其他

- 航空系統

- 戰鬥機

- 運輸機及加油機

- 直升機

- 無人駕駛飛行器(UAV)

- 其他

- 空間系統

- 軍事通訊衛星

- 偵察/監視衛星

- 導航衛星

- 飛彈預警衛星

- 空間情境察覺

- 其他

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- 主要企業

- Lockheed Martin

- Raytheon Technologies

- Northrop Grumman

- Boeing

- 按地區分類的主要企業

- 北美洲

- General Dynamics

- L3Harris Technologies

- Analog Devices

- 歐洲

- BAE Systems

- Thales Group

- Infineon Technologies

- 北美洲

- 特殊玩家/干擾者

- Microchip Technology

- Texas Instruments

- STMicroelectronics

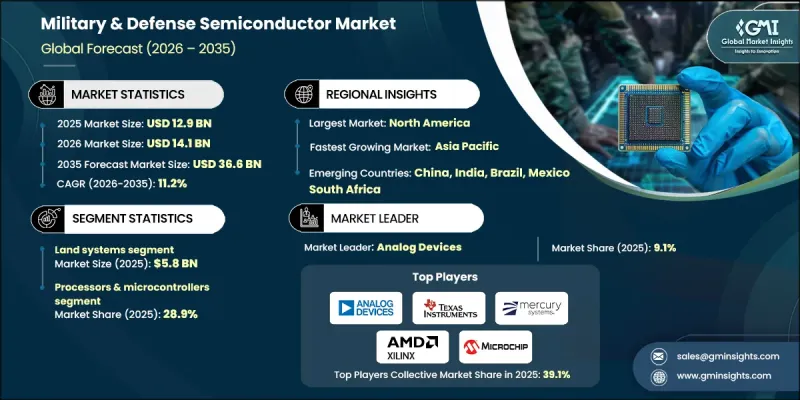

The Global Military & Defense Semiconductor Market was valued at USD 12.9 billion in 2025 and is estimated to grow at a CAGR of 11.2% to reach USD 36.6 billion by 2035.

The market is witnessing strong momentum as governments worldwide continue to increase defense spending and prioritize technological superiority. Higher budget allocations are accelerating research, development, and deployment of advanced semiconductor solutions across communication networks, intelligence systems, radar platforms, electronic warfare, and precision-guided equipment. Modern defense infrastructure increasingly depends on high-performance semiconductor components that enable faster data processing, secure connectivity, real-time analytics, and system interoperability. Semiconductors used in military and defense applications function as critical electronic materials with controlled conductivity, forming the foundation of microprocessors, integrated circuits, sensors, and power management devices. These components are central to the performance, efficiency, and reliability of advanced defense electronics. As armed forces modernize air, land, naval, and space capabilities, demand for rugged, secure, and energy-efficient semiconductor technologies continues to rise, supporting sustained long-term market expansion across global defense ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.9 Billion |

| Forecast Value | $36.6 Billion |

| CAGR | 11.2% |

At the same time, export controls and geopolitical tensions present structural challenges for the military & defense semiconductor market. Strict trade regulations and national security policies limit the cross-border transfer of sensitive technologies, restricting global supply chain flexibility. Governments are implementing protective measures to safeguard strategic semiconductor capabilities, which can slow procurement cycles and create sourcing constraints. Geopolitical uncertainties further intensify supply chain volatility, making localized production and secure sourcing increasingly important for defense applications.

The land systems segment generated USD 5.8 billion in 2025 and is expected to grow at a CAGR of 11.8% between 2026 and 2035. Semiconductor integration within ground-based platforms is expanding as defense organizations incorporate autonomous navigation, advanced sensing, and secure communication technologies into tactical systems. Real-time data processing, mission coordination, and resilient communication networks are essential requirements driving semiconductor adoption in this segment. Durable, low-power, and high-reliability components are being deployed to ensure operational continuity in demanding environments, reinforcing the importance of specialized semiconductor design for land-based military applications.

The processors & microcontrollers segment accounted for 28.9% share in 2025. Rising demand for high-performance computing in defense platforms is accelerating the adoption of advanced processing technologies. Modern defense systems require embedded intelligence, encryption capability, secure communications, and AI-enabled analytics, all supported by sophisticated processors. In addition, ruggedized and power-efficient microcontrollers are gaining traction for deployment in compact defense electronics, unmanned systems, and portable military equipment. These technologies enhance command control, automation, and operational efficiency across multiple mission-critical applications.

North America Military & Defense Semiconductor Market held a 45.1% share in 2025. Regional growth is supported by ongoing modernization programs across air, ground, naval, and space platforms. Increased emphasis on artificial intelligence, autonomous systems, cybersecurity, and advanced communications infrastructure continues to fuel demand for high-performance semiconductor technologies. Recurring upgrade cycles, system retrofitting, and maintenance programs also sustain long-term procurement activity. Furthermore, government initiatives aimed at strengthening domestic semiconductor manufacturing capacity are enhancing regional self-reliance and reducing dependence on foreign suppliers for critical defense components.

Key companies operating in the Global Military & Defense Semiconductor Market include Texas Instruments, Lockheed Martin, Analog Devices, Northrop Grumman, Microchip Technology, Raytheon Technologies, Infineon Technologies, General Dynamics, STMicroelectronics, L3Harris Technologies, Boeing, and BAE Systems. Companies in the military & defense semiconductor market strengthen their competitive position by investing heavily in research and development focused on secure, rugged, and high-performance chip architectures. Strategic partnerships with defense contractors and government agencies help align product development with mission-specific requirements. Many firms are expanding domestic manufacturing capabilities to address supply chain security and comply with national security regulations. Portfolio diversification across processors, sensors, power devices, and communication chips enhances cross-platform integration opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing government investments in military

- 3.2.1.2 Utilization of radiation-tolerant semiconductor components

- 3.2.1.3 Increasing aircraft upgrades and modernization programs

- 3.2.1.4 Growing demand for advanced semiconductor technologies

- 3.2.1.5 Increasing use of Artificial Intelligence (AI) and Machine Learning (ML) in military operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and long development cycles

- 3.2.2.2 Export restrictions and geopolitical tensions

- 3.2.3 Market opportunities

- 3.2.3.1 Advancements in electronic warfare and communication systems

- 3.2.3.2 High-performance computing for defense simulation and command systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.14.3 Defense budget allocation by segment

- 3.14.3.1 Personnel

- 3.14.3.2 Operations and maintenance

- 3.14.3.3 Procurement

- 3.14.3.4 Research, development, test and evaluation

- 3.14.3.5 Infrastructure and construction

- 3.14.3.6 Technology and innovation

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2022-2025)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.1.1 Processors & microcontrollers

- 5.1.2 General-purpose processors

- 5.1.3 AI/ML processors

- 5.1.4 Cryptographic processors

- 5.1.5 Digital signal processors

- 5.1.6 Microcontrollers

- 5.2 Memory devices

- 5.2.1 SRAM (static RAM)

- 5.2.2 DRAM (dynamic RAM)

- 5.2.3 Flash memory (NAND, NOR)

- 5.2.4 MRAM (magnetoresistive RAM)

- 5.2.5 EEPROM/NVRAM

- 5.3 Logic devices

- 5.3.1 ASICs (application-specific integrated circuits)

- 5.3.2 FPGAs (field-programmable gate arrays)

- 5.3.3 PLDs (programmable logic devices)

- 5.3.4 CPLDs (complex programmable logic devices)

- 5.4 RF & microwave components

- 5.4.1 MMICs (monolithic microwave ICs)

- 5.4.2 T/R modules (transmit/receive modules)

- 5.4.3 RF power amplifiers

- 5.4.4 Others

- 5.5 Power management ICs

- 5.5.1 DC-DC converters (buck, boost, buck-boost, isolated)

- 5.5.2 LDOs (low-dropout regulators)

- 5.5.3 Power MOSFETs & gate drivers

- 5.5.4 Others

- 5.6 Analog & mixed-signal ICs

- 5.6.1 Operational amplifiers

- 5.6.2 Comparators

- 5.6.3 Analog switches & multiplexers

- 5.6.4 Others

- 5.7 Data converters (ADC/DAC)

- 5.8 Optoelectronics

- 5.9 Discrete semiconductors

- 5.10 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Land systems

- 6.2.1 Combat vehicles (tanks, IFVs, APCs)

- 6.2.2 Tactical vehicles (HMMWVs, MRAPs, trucks)

- 6.2.3 Artillery systems

- 6.2.4 Ground-based air defense

- 6.2.5 Others

- 6.3 Naval systems

- 6.3.1 Surface combatants

- 6.3.2 Aircraft carriers

- 6.3.3 Submarines

- 6.3.4 Amphibious warfare ships

- 6.3.5 Others

- 6.4 Airborne systems

- 6.4.1 Fighter aircraft

- 6.4.2 Transport & tanker aircraft

- 6.4.3 Helicopters

- 6.4.4 UAVs

- 6.4.5 Others

- 6.5 Space systems

- 6.5.1 Military communications satellites

- 6.5.2 Reconnaissance & surveillance satellites

- 6.5.3 Navigation satellites

- 6.5.4 Missile warning satellites

- 6.5.5 Space situational awareness

- 6.5.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Global Key Players

- 8.1.1 Lockheed Martin

- 8.1.2 Raytheon Technologies

- 8.1.3 Northrop Grumman

- 8.1.4 Boeing

- 8.2 Regional Key Players

- 8.2.1 North America

- 8.2.1.1 General Dynamics

- 8.2.1.2 L3Harris Technologies

- 8.2.1.3 Analog Devices

- 8.2.2 Europe

- 8.2.2.1 BAE Systems

- 8.2.2.2 Thales Group

- 8.2.2.3 Infineon Technologies

- 8.2.1 North America

- 8.3 Niche Players / Disruptors

- 8.3.1 Microchip Technology

- 8.3.2 Texas Instruments

- 8.3.3 STMicroelectronics