|

市場調查報告書

商品編碼

1959570

免疫查核點抑制劑市場機會、成長要素、產業趨勢分析及2026年至2035年預測。Immune Checkpoint Inhibitors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

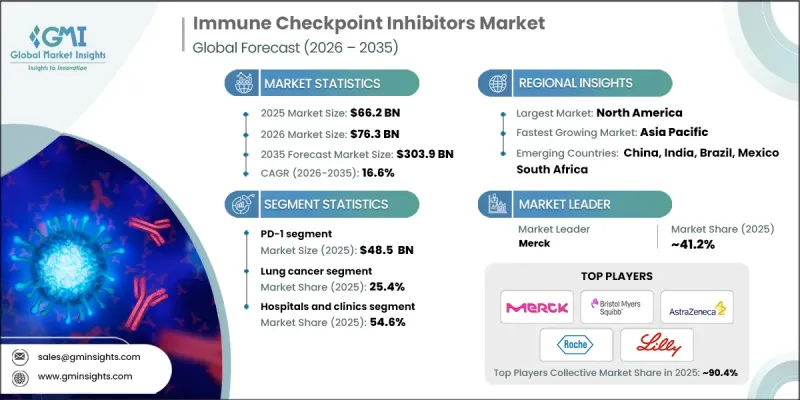

2025 年全球免疫查核點抑制劑市場價值為 662 億美元,預計到 2035 年將達到 3,039 億美元,年複合成長率為 16.6%。

市場擴張的驅動力在於這些治療方法在多種癌症類型中已證實的臨床療效,以及它們在腫瘤治療中日益普及並成為標準療法。隨著全球癌症發生率的持續上升,對強效標靶治療方法(例如免疫查核點抑制劑)的需求也日益成長。這些治療方法透過抑制PD-1、PD-L1和CTLA-4等免疫查核點蛋白發揮作用,進而活化人類免疫系統對抗癌細胞。癌細胞利用這些蛋白質來逃避免疫系統的檢測。抑制這些蛋白質可以恢復T細胞功能,使免疫系統能夠有效地靶向並清除惡性細胞。隨著晚期難治性癌症患者數量的增加,免疫療法的適用人群也在不斷擴大,而開發更有效、更精準、更安全的抑制劑的持續創新,仍然是推動市場成長的關鍵因素。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 662億美元 |

| 預測金額 | 3039億美元 |

| 複合年成長率 | 16.6% |

預計到2025年,PD-1抑制劑市場規模將達到485億美元,反映了其在癌症免疫療法中的關鍵作用。 PD-1抑制劑透過抑制PD-1路徑來增強免疫系統攻擊癌細胞的能力,而癌細胞通常利用PD-1路徑來逃避免疫系統的辨識。這些治療方法的成功,得益於顯著的臨床療效、不斷增加的核准適應症以及在腫瘤臨床實踐中的廣泛應用,已使PD-1抑制劑成為現代癌症治療的基石。它們在多種癌症類型中的療效正在鞏固其市場主導地位,並強化其在臨床腫瘤學中的重要性。

肺癌領域佔25.4%的市場佔有率,預計2035年將以16%的複合年成長率成長。這一主導地位源自於肺癌的高發生率以及免疫查核點抑制劑在提高存活率和改善患者預後方面所展現的臨床效益。免疫療法作為一線治療方法的日益普及,以及正在進行的探索其在不同肺癌階段療效的臨床試驗,進一步鞏固了其市場地位。沉重的疾病負擔和未被滿足的醫療需求推動了對這些治療方法的需求,從而維持了該領域的強勁成長。

預計到2025年,北美免疫查核點抑制劑市佔率將達48.3%。這一主導地位得益於許多大型製藥公司積極參與此類治療方法的研發和商業化。該地區擁有良好的法規環境,政府和非政府組織對癌症治療舉措的大力支持,以及癌症發病率上升帶來的日益成長的需求。加之先進的醫療基礎設施、對免疫療法的廣泛認知以及獲得創新治療方案的便利,北美正在鞏固其在全球市場的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 全球癌症發生率不斷上升

- 擴大核准,用於多種癌症適應症

- 免疫療法作為標準治療方案的轉變正在加速。

- 擴大投資和合作關係

- 產業潛在風險與挑戰

- 免疫相關不利事件風險增加

- 高昂的醫療費用

- 市場機遇

- 聯合免疫療法方案的成長

- 下一代免疫查核點靶點的開發

- 促進因素

- 成長潛力分析

- 監理情勢

- 救贖方案

- 管道分析

- 價格分析

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- PD-1

- PD-L1

- CTLA-4

- 其他類型

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 肺癌

- 乳癌

- 膀胱癌

- 惡性黑色素瘤

- 子宮頸癌

- 何傑金氏淋巴瘤

- 結腸癌

- 其他用途

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院和診所

- 癌症中心

- 學術研究機構

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- AstraZeneca

- BeiGene

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- F. Hoffmann-La Roche

- GlaxoSmithKline

- Incyte Corporation

- Immutep Limited

- Merck

- Regeneron Pharmaceuticals

- Sanofi

- Shanghai Junshi Biosciences

- Sun Pharmaceuticals

- Zydus Lifesciences

The Global Immune Checkpoint Inhibitors Market was valued at USD 66.2 billion in 2025 and is estimated to grow at a CAGR of 16.6% to reach USD 303.9 billion by 2035.

The market expansion is driven by the proven clinical effectiveness of these therapies across a broad spectrum of cancers and their increasing adoption as a standard of care in oncology. As cancer incidence continues to rise worldwide, the demand for potent and targeted treatments such as immune checkpoint inhibitors is intensifying. These therapies work by enhancing the body's immune system to combat tumor cells, specifically by blocking immune checkpoint proteins like PD-1, PD-L1, and CTLA-4, which are exploited by cancer cells to evade immune detection. By inhibiting these proteins, T-cell function is restored, enabling the immune system to effectively target and eliminate malignant cells. The rising prevalence of hard-to-treat and late-stage cancers is increasing the patient population for immunotherapy, while ongoing innovation in the development of more effective, precise, and safe inhibitors continues to propel market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $66.2 Billion |

| Forecast Value | $303.9 Billion |

| CAGR | 16.6% |

The PD-1 segment reached USD 48.5 billion in 2025, reflecting its critical role in cancer immunotherapy. PD-1 inhibitors enhance the immune system's ability to attack tumor cells by blocking the PD-1 pathway, which is commonly used by cancer cells to escape immune recognition. The success of these therapies is supported by strong clinical outcomes, a growing list of approved indications, and widespread adoption in oncology practices, positioning PD-1 inhibitors as a cornerstone in modern cancer treatment. Their effectiveness across multiple cancer types reinforces their dominant share and solidifies their importance in clinical oncology.

The lung cancer segment held 25.4% share and is expected to grow at a CAGR of 16% through 2035. This dominance is attributed to the high prevalence of lung cancer and the demonstrated clinical benefits of immune checkpoint inhibitors in improving survival rates and patient outcomes. The increasing adoption of immunotherapy as a primary treatment, combined with ongoing clinical trials exploring its efficacy in different stages of lung cancer, continues to strengthen market presence. The high disease burden and unmet medical needs further drive demand for these therapies, sustaining robust growth in this segment.

North America Immune Checkpoint Inhibitors Market held 48.3% share in 2025. This leadership is supported by the presence of major pharmaceutical companies actively engaged in research, development, and commercialization of these therapies. The region benefits from a favorable regulatory environment, strong governmental and non-governmental support for cancer treatment initiatives, and rising demand driven by increasing cancer prevalence. Advanced healthcare infrastructure, widespread awareness of immunotherapy options, and access to innovative treatment solutions collectively strengthen North America's dominant position in the global market.

Key players in the Global Immune Checkpoint Inhibitors Market include Merck, Bristol-Myers Squibb Company, AstraZeneca, BeiGene, GlaxoSmithKline, Eli Lilly and Company, Sanofi, Immutep Limited, Incyte Corporation, Shanghai Junshi Biosciences, Zydus Lifesciences, Regeneron Pharmaceuticals, F. Hoffmann-La Roche, and Sun Pharmaceuticals. Companies in the immune checkpoint inhibitors market are leveraging multiple strategies to expand their footprint and reinforce their market presence. They are investing heavily in research and development to create next-generation inhibitors with improved safety profiles, broader efficacy, and expanded indications across cancer types. Strategic partnerships with biotechnology firms, hospitals, and academic institutions accelerate clinical trials and innovation. Geographic expansion into emerging markets allows firms to tap into growing patient populations. Additionally, mergers and acquisitions, licensing agreements, and collaborations with regulatory agencies streamline market entry and product approvals.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer worldwide

- 3.2.1.2 Expanding approvals across multiple cancer indications

- 3.2.1.3 Growing shift toward immunotherapy as standard of care

- 3.2.1.4 Increasing investments and partnerships

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Growing risk of immune-related adverse events

- 3.2.2.2 High treatment costs

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of combination immunotherapy regimens

- 3.2.3.2 Development of next-generation immune checkpoint targets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Reimbursement scenario

- 3.6 Pipeline analysis

- 3.7 Pricing analysis

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 PD-1

- 5.3 PD-L1

- 5.4 CTLA-4

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Lung cancer

- 6.3 Breast cancer

- 6.4 Bladder cancer

- 6.5 Melanoma

- 6.6 Cervical cancer

- 6.7 Hodgkin lymphoma

- 6.8 Colorectal cancer

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Cancer centers

- 7.4 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AstraZeneca

- 9.2 BeiGene

- 9.3 Bristol-Myers Squibb Company

- 9.4 Eli Lilly and Company

- 9.5 F. Hoffmann-La Roche

- 9.6 GlaxoSmithKline

- 9.7 Incyte Corporation

- 9.8 Immutep Limited

- 9.9 Merck

- 9.10 Regeneron Pharmaceuticals

- 9.11 Sanofi

- 9.12 Shanghai Junshi Biosciences

- 9.13 Sun Pharmaceuticals

- 9.14 Zydus Lifesciences

下一代免疫查核點抑制劑市場(第二版):按標靶免疫查核點、標靶疾病、分子類型、地區、主要參與者和治療方法的銷售預測-趨勢與預測至2035年

下一代免疫查核點抑制劑市場(第二版):按標靶免疫查核點、標靶疾病、分子類型、地區、主要參與者和治療方法的銷售預測-趨勢與預測至2035年 免疫查核點抑制劑市場報告:按類型、分銷管道、應用和地區分類(2026-2034 年)

免疫查核點抑制劑市場報告:按類型、分銷管道、應用和地區分類(2026-2034 年) 全球免疫查核點抑制劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球免疫查核點抑制劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 免疫查核點抑制劑市場:按適應症、作用機制、給藥途徑和最終用戶分類的全球市場預測,2026-2032年PD-1/PD-L1查核點抑制劑市場按產品、治療線、適應症、最終用戶和分銷管道分類,全球預測,2026-2032 年

免疫查核點抑制劑市場:按適應症、作用機制、給藥途徑和最終用戶分類的全球市場預測,2026-2032年PD-1/PD-L1查核點抑制劑市場按產品、治療線、適應症、最終用戶和分銷管道分類,全球預測,2026-2032 年 免疫查核點抑制劑市場:依藥物類別、癌症類型、通路和地區分類

免疫查核點抑制劑市場:依藥物類別、癌症類型、通路和地區分類 免疫查核點抑制劑市場規模、佔有率和成長分析(按類型、應用、分銷管道和地區分類)-2026-2033年產業預測免疫檢查點抑制劑市場-產業趨勢及全球預測(至2030年)-依關鍵免疫檢查點標靶、標靶適應症、作用機轉、治療方式、治療方法及主要地區劃分

免疫查核點抑制劑市場規模、佔有率和成長分析(按類型、應用、分銷管道和地區分類)-2026-2033年產業預測免疫檢查點抑制劑市場-產業趨勢及全球預測(至2030年)-依關鍵免疫檢查點標靶、標靶適應症、作用機轉、治療方式、治療方法及主要地區劃分 內源性幹細胞動員、全身組織再生和器官間修復途徑-技術趨勢、研發管線和市場展望(2025-2045)

內源性幹細胞動員、全身組織再生和器官間修復途徑-技術趨勢、研發管線和市場展望(2025-2045) 免疫查核點抑制劑市場分析及預測(至 2034 年):類型、產品、應用、最終用戶、技術、服務、成分、製程、設備

免疫查核點抑制劑市場分析及預測(至 2034 年):類型、產品、應用、最終用戶、技術、服務、成分、製程、設備