|

市場調查報告書

商品編碼

1959564

汽車照明市場機會、成長要素、產業趨勢分析及2026年至2035年預測Automotive Lighting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

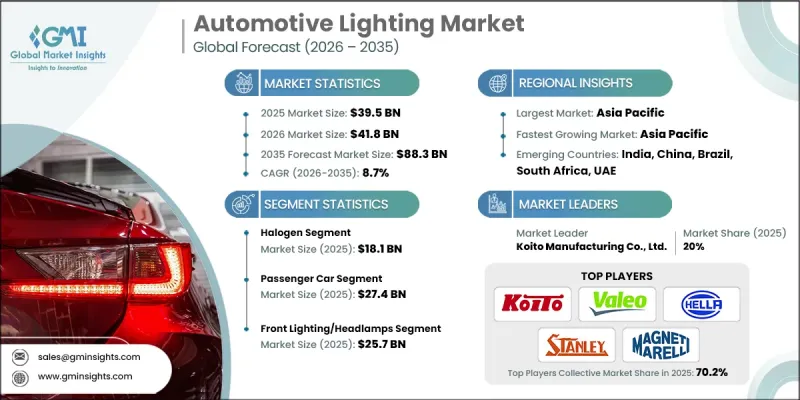

全球汽車照明市場預計到 2025 年價值 395 億美元,預計到 2035 年將達到 883 億美元,年複合成長率為 8.7%。

該產業的成長得益於LED和自適應照明系統的日益普及、日益嚴格的車輛安全標準和排放氣體法規、電動車和自動駕駛汽車的日益普及、消費者對節能時尚照明的需求,以及新興市場汽車製造業的擴張。遵守全球安全標準和能源效率要求正在加速先進照明技術的應用,從而提高駕駛員的視野、減少眩光並提升車輛的整體效率。向電氣化和自動駕駛的轉型進一步擴大了先進照明解決方案在現代車輛安全、能源管理和美學設計方面的應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 395億美元 |

| 預測金額 | 883億美元 |

| 複合年成長率 | 8.7% |

預計到2025年,鹵素燈市場規模將達到181億美元,其強勁的需求將得益於其低廉的生產成本、簡單的製造流程以及與現有車輛電氣系統的廣泛相容性。在LED和自適應照明系統等高階照明技術尚未普及的入門級和中檔車型中,鹵素燈仍然被廣泛使用,在不影響基本安全要求的前提下,提供了一種經濟高效的解決方案。隨著全球汽車數量的成長,鹵素燈在售後替換件市場也佔據重要地位,預計老舊車輛的改裝需求將持續成長。此外,鹵素燈泡在各種駕駛條件下都表現出可靠性,且維護需求極低,因此成為車隊營運商、商用車公司以及將成本效益放在首位的開發中市場的首選。

預計到2025年,乘用車市場規模將達到274億美元,主要得益於市場對先進照明技術的強勁需求,例如兼顧安全性和視覺美感的自我調整LED矩陣系統。這些技術能夠實現動態光束調節,提升夜間能見度,並減少對向來車的眩光,從而提高駕駛安全評級。此外,乘用車買家越來越重視照明的美觀性,將其作為車輛設計和品牌識別的重要組成部分,汽車製造商也正透過獨特的照明模式來區分不同車型。主要市場的法規結構(例如強制性日間行車燈、自我調整頭燈和能源效率標準)也在加速這些技術的普及應用。

推動要素到2025年,北美汽車照明市場佔有率將達到18.5%,這主要得益於車輛電氣化程度的提高、LED和智慧自適應照明系統的日益普及,以及聯邦照明和安全標準的嚴格執行。該地區先進的汽車製造生態系統、強力的監管執行以及消費者對高性能、高能源效率照明解決方案的偏好,都為市場擴張提供了支持。先進的頭燈系統、矩陣式LED和智慧運輸技術正逐漸成為新型乘用車和輕型商用車的標準配置,有助於提高能見度、降低能耗並增強駕駛安全性。此外,隨著自動駕駛和智慧出行基礎設施的日益普及,北美製造商正大力投資於智慧互聯照明解決方案的研發,這些解決方案整合了感測器和物聯網技術,能夠實現自適應的、與自動駕駛車輛相容的照明功能。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對LED和自適應照明系統的需求不斷成長

- 嚴格的車輛安全標準和排放氣體法規

- 電動車和自動駕駛汽車的廣泛應用

- 消費者越來越偏好選擇時尚節能的照明產品。

- 新興市場汽車生產的擴張

- 挑戰與困難

- 先進照明系統的初始成本很高

- 與車輛電子設備整合的複雜性

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 供應鏈韌性

- 地緣政治分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 地理位置比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 產品系列比較

- 2022-2025 年重大發展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估價與預測:依產品分類,2022-2035年

- LED

- 鹵素

- 氙

第6章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 商用車輛

- 摩托車

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 主要趨勢

- 頭燈/大燈

- 後部照明

- 室內照明

- 側燈

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- 主要企業

- General Electric Company

- Samsung Electronics Co., Ltd.

- Koninklijke Philips NV

- Robert Bosch Gmbh

- 按地區分類的主要企業

- 北美洲

- Continental AG

- Lumax Industries

- Varroc Lighting Solutions

- 歐洲

- HELLA GmbH & Co. KGaA

- OSRAM Gmbh

- Tungsram Group

- Zkw Lichtsysteme Gmbh

- Zizala Lichtsysteme Gmbh

- Magnetti Marelli SpA

- Valeo Visibility Systems

- 亞太地區

- Hyundai Mobis Co., Ltd

- Koito Manufacturing Co.

- Ichikoh Industries, Ltd.

- Seoul Semiconductor

- Stanley Electric Co.Ltd

- 北美洲

- Niche Player/Disruptor

- Namyung Lighting

The Global Automotive Lighting Market was valued at USD 39.5 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 88.3 billion by 2035.

The industry's growth is driven by increasing adoption of LED and adaptive lighting systems, stricter vehicle safety and emissions regulations, rising popularity of electric and autonomous vehicles, consumer demand for energy-efficient and stylish lighting, and expansion of automotive manufacturing in emerging markets. Regulatory compliance with global safety standards and energy-efficiency mandates is encouraging the integration of advanced lighting technologies, enhancing driver visibility, reducing glare, and contributing to overall vehicle efficiency. The shift toward electrification and autonomous driving has further amplified the use of sophisticated lighting solutions as critical components of safety, energy management, and aesthetic design in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.5 Billion |

| Forecast Value | $88.3 Billion |

| CAGR | 8.7% |

The halogen segment accounted for USD 18.1 billion in 2025, maintaining strong demand due to its low production costs, straightforward manufacturing processes, and broad compatibility with existing vehicle electrical systems. Halogen lighting continues to be widely used in entry-level and mid-segment vehicles where premium lighting technologies like LEDs or adaptive systems are not yet standard, offering a cost-effective solution without compromising basic safety requirements. Its relevance extends to aftermarket replacements, supported by the growing global vehicle parc, which ensures a consistent demand for retrofitting older vehicles. Additionally, halogen bulbs provide reliability under diverse driving conditions and require minimal maintenance, making them a preferred choice for fleet operators, commercial vehicles, and markets in developing regions where cost efficiency remains a priority.

The passenger car segment reached USD 27.4 billion in 2025, driven by strong demand for advanced lighting features such as adaptive, LED, and matrix systems, which enhance both safety and visual appeal. These technologies provide dynamic beam adjustments, improved nighttime visibility, and glare reduction for oncoming traffic, contributing to higher driving safety ratings. Furthermore, passenger car buyers increasingly consider lighting aesthetics as part of vehicle design and brand identity, pushing automakers to differentiate their models with signature lighting patterns. Regulatory frameworks in major markets, including mandatory daytime running lights, adaptive headlamps, and energy-efficiency standards, further accelerate adoption.

North America Automotive Lighting Market held an 18.5% share in 2025, driven by rising vehicle electrification, widespread adoption of LED and smart adaptive lighting systems, and strict compliance with federal lighting and safety standards. The region's advanced automotive manufacturing ecosystem, strong regulatory enforcement, and consumer preference for high-performance, energy-efficient lighting solutions underpin market expansion. Advanced front lighting systems, matrix LED, and laser-based technologies are becoming standard in new passenger and commercial vehicle models, supporting enhanced visibility, reduced power consumption, and improved driving safety. Additionally, North American manufacturers are investing heavily in R&D for intelligent and connected lighting solutions, integrating sensors and IoT technologies to enable adaptive, autonomous vehicle-ready lighting that aligns with the growing focus on automated driving and smart mobility infrastructure.

Prominent players in the Global Automotive Lighting Market include Continental AG, General Electric Company, HELLA GmbH & Co. KGaA, Hyundai Mobis Co., Ltd, Ichikoh Industries, Ltd., Koito Manufacturing Co., Koninklijke Philips N.V., Lumax Industries, Magnetti Marelli S.p.A, Namyung Lighting, OSRAM GmbH, Robert Bosch GmbH, Samsung Electronics Co., Ltd., Seoul Semiconductor, Stanley Electric Co., Ltd., Tungsram Group, Valeo Visibility Systems, Varroc Lighting Solutions, Zizala Lichtsysteme GmbH, and ZKW Lichtsysteme GmbH. Companies in the Automotive Lighting Market are focusing on strategic initiatives such as expanding R&D for LED and adaptive systems, forming partnerships with OEMs to integrate intelligent lighting technologies, optimizing supply chains for global distribution, investing in sustainable energy-efficient solutions, launching aftermarket programs to capture legacy vehicle demand, and adopting digital and IoT-enabled lighting innovations. Emphasis on design differentiation, regulatory compliance, and modular, scalable solutions helps manufacturers strengthen market presence, improve brand recognition, and secure long-term contracts with automotive producers worldwide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Vehicle type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for LED and adaptive lighting systems

- 3.2.1.2 Stringent vehicle safety and emission regulations

- 3.2.1.3 Increasing adoption of electric and autonomous vehicles

- 3.2.1.4 Growing consumer preference for stylish and energy-efficient lighting

- 3.2.1.5 Expansion of automotive production in emerging markets

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High initial costs of advanced lighting systems

- 3.2.2.2 Complexity in integration with vehicle electronics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 LED

- 5.3 Halogen

- 5.4 Xenon

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicles

- 6.4 Two wheelers

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 Front lighting/Headlamps

- 7.3 Rear lighting

- 7.4 Interior lighting

- 7.5 Side lighting

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 General Electric Company

- 9.1.2 Samsung Electronics Co., Ltd.

- 9.1.3 Koninklijke Philips N.V.

- 9.1.4 Robert Bosch Gmbh

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Continental AG

- 9.2.1.2 Lumax Industries

- 9.2.1.3 Varroc Lighting Solutions

- 9.2.2 Europe

- 9.2.2.1 HELLA GmbH & Co. KGaA

- 9.2.2.2 OSRAM Gmbh

- 9.2.2.3 Tungsram Group

- 9.2.2.4 Zkw Lichtsysteme Gmbh

- 9.2.2.5 Zizala Lichtsysteme Gmbh

- 9.2.2.6 Magnetti Marelli S.p.A

- 9.2.2.7 Valeo Visibility Systems

- 9.2.3 Asia Pacific

- 9.2.3.1 Hyundai Mobis Co., Ltd

- 9.2.3.2 Koito Manufacturing Co.

- 9.2.3.3 Ichikoh Industries, Ltd.

- 9.2.3.4 Seoul Semiconductor

- 9.2.3.5 Stanley Electric Co.Ltd

- 9.2.1 North America

- 9.3 Niche Player/Disruptor

- 9.3.1 Namyung Lighting

2026年全球汽車輔助照明市場報告

2026年全球汽車輔助照明市場報告 汽車照明市場:2026-2032年全球市場預測(依產品類型、技術、車輛類型、應用和銷售管道分類)汽車周邊照明市場:依技術、銷售管道、車輛類型及應用分類-2026-2032年全球市場預測汽車外飾LED照明市場:依產品類型、安裝位置、乘用車及銷售管道分類-2026-2032年全球市場預測汽車高位煞車燈市場:按光源、車輛類型、驅動系統和銷售管道分類-2026-2032年全球市場預測下一代汽車照明市場:按產品類型、技術、車輛類型、銷售管道和應用分類-2026-2032年全球市場預測汽車鹵素燈泡市場:依產品類型、應用、車輛類型和通路分類,全球預測,2026-2032年

汽車照明市場:2026-2032年全球市場預測(依產品類型、技術、車輛類型、應用和銷售管道分類)汽車周邊照明市場:依技術、銷售管道、車輛類型及應用分類-2026-2032年全球市場預測汽車外飾LED照明市場:依產品類型、安裝位置、乘用車及銷售管道分類-2026-2032年全球市場預測汽車高位煞車燈市場:按光源、車輛類型、驅動系統和銷售管道分類-2026-2032年全球市場預測下一代汽車照明市場:按產品類型、技術、車輛類型、銷售管道和應用分類-2026-2032年全球市場預測汽車鹵素燈泡市場:依產品類型、應用、車輛類型和通路分類,全球預測,2026-2032年 全球汽車照明市場規模、佔有率、趨勢和成長分析報告(2026-2034年)汽車照明市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

全球汽車照明市場規模、佔有率、趨勢和成長分析報告(2026-2034年)汽車照明市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 汽車照明:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車照明:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)