|

市場調查報告書

商品編碼

1959559

2026 年至 2035 年硼礦物和化學品的市場機會、成長要素、產業趨勢分析和預測。Boron Minerals and Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

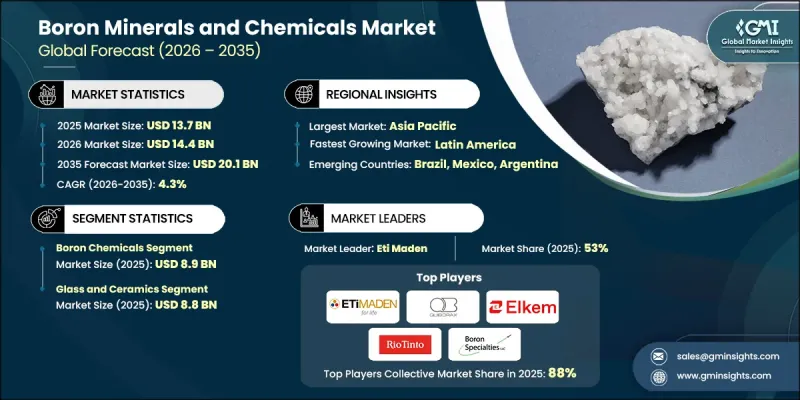

2025 年全球硼礦物和化學品市場價值為 137 億美元,預計到 2035 年將達到 201 億美元,年複合成長率為 4.3%。

該市場涵蓋天然硼礦物及其衍生的所有工業化合物。主要礦物包括硼砂、鈣硼石、鉀硼石和尿素硼石,它們為商業硼萃取提供了基礎資訊。透過加工這些礦物可獲得硼酸、氧化硼和各種硼酸鹽等硼化合物,這些化合物因其耐熱性、硬度和化學穩定性而備受重視。傳統上,硼因其成本效益和功能多樣性而被廣泛應用於玻璃、陶瓷和農業領域。在玻璃和陶瓷應用中,硼有望改善其熱性能和光學性能;在農業領域,硼有望作為一種重要的微量營養素,促進植物生長和提高產量。近年來,隨著技術的進步,硼的應用範圍已擴展到高科技領域,尤其是在鋰離子電池、永久磁鐵、半導體、航太複合材料和永續奈米材料等新興產業中,硼的應用呈現出顯著的環保和高附加價值趨勢。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 137億美元 |

| 預測金額 | 201億美元 |

| 複合年成長率 | 4.3% |

預計到2025年,硼化學品市場規模將達89億美元。農業、清潔劑、電子產品和先進材料等領域的廣泛應用,推動了對高純度和特殊化合物的需求成長。各行業都希望利用這些化學品來提升性能、效率和永續性,從而促進化學加工技術的創新,並開發用於高價值應用的差異化產品。

預計到2025年,玻璃和陶瓷產業的市場規模將達到88億美元。硼能夠增強硼矽酸玻璃、玻璃纖維和先進陶瓷的耐熱性和耐久性。建築和工業領域對硼的需求持續受到節能目標的驅動。將硼添加到合金和金屬中可以提高其硬度、強度和耐腐蝕性,從而支持其在製造業和汽車行業的應用。此外,硼的清潔效率和化學穩定性也使清潔劑和漂白劑受益,使其成為家用和工業配方中不可或缺的成分。

預計到2025年,北美硼礦物和化學品市場規模將達到22億美元。這一成長主要得益於先進製造業的擴張,這些產業對高性能硼產品的需求日益成長,例如航太、電子和清潔能源等行業。基礎設施投資、回收利用計劃以及嚴格的環境法規也進一步推動了市場需求。北美擁有完善的供應鏈和強大的特殊硼化學品研發生態系統。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 擴大在多個工業領域的應用

- 建築和基礎設施開發增加

- 持續改善材料性能和效率

- 產業潛在風險與挑戰

- 加強對採礦活動的環境監管

- 精製硼化學品生產成本高昂

- 市場機遇

- 對先進高性能材料的需求日益成長。

- 人們越來越關注永續和高效的農業

- 向特種用途和高附加價值硼產品過渡

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 硼礦物

- 煤炭石

- 尿素

- 電氣石

- 硼基化學品

- 硼酸

- 硼酸鹽

- 無水硼酸鹽

- 硼砂

- 無水硼砂

- 鹵化硼

- 三氯化硼

- 三氟化硼

- 三溴化硼

- 其他

- 硼酸酯

- 硼氫化物

- 黑蘭花

- 尼多波蘭

- 蛛形綱

- 碳化硼

- 氮化硼

- 六方晶系氮化硼

- 立方氮化硼

- 纖鋅礦型氮化硼

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 玻璃和陶瓷

- 硼矽酸玻璃

- 展示玻璃

- 玻璃纖維

- 絕緣玻璃纖維

- 特種玻璃

- 其他

- 合金和金屬

- 鋼合金

- 金屬加工

- 焊接和連接

- 其他

- 清潔劑和漂白劑

- 洗衣精

- 家用清潔劑

- 工業清潔劑

- 漂白

- 其他

- 殺蟲劑

- 微量元素肥料

- 土壤改良

- 其他

- 黏合劑

- 工業用黏合劑

- 建築黏合劑

- 特殊黏合劑

- 其他

- 其他

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第8章:公司簡介

- 3M Company

- American Borate

- Boron Specialties, LLC

- Eti Maden

- Gremont Chemical Company

- Inkabor

- Minera Santa Rita

- National Boraxx Corporation

- Rio Tinto(US Borax)

- Searles Valley Minerals

- 5E Advanced Materials

- Quiborax SA

The Global Boron Minerals and Chemicals Market was valued at USD 13.7 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 20.1 billion by 2035.

The market encompasses naturally occurring boron minerals and all industrial chemical compounds derived from them. Key minerals include borax, colemanite, kernite, and ulexite, which serve as primary sources for commercial boron extraction. Boron chemicals, such as boric acid, boron oxide, and various borates, are obtained through processing these minerals and are prized for their heat resistance, hardness, and chemical stability. Traditionally, boron has been used in glass, ceramics, and agriculture due to its cost-effectiveness and functional versatility. Glass and ceramic applications benefit from enhanced thermal and optical properties, while boron-based chemicals in agriculture act as essential micronutrients that support plant growth and crop yields. Recently, technological advancements have expanded boron's role into high-tech applications, including lithium-ion batteries, permanent magnets, semiconductors, aerospace composites, and sustainable nanomaterials, reflecting a shift toward environmentally conscious, high-value uses in emerging industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.7 Billion |

| Forecast Value | $20.1 Billion |

| CAGR | 4.3% |

The boron chemicals segment reached USD 8.9 billion in 2025. Their widespread adoption in agriculture, detergents, electronics, and advanced materials stems from the increasing demand for high-purity and specialty compounds. Industries are seeking these chemicals to enhance performance, efficiency, and sustainability, prompting innovations in chemical processing technologies and the development of differentiated products for high-value applications.

The glass and ceramics segment generated USD 8.8 billion in 2025. Boron improves heat resistance and durability in borosilicate glass, fiberglass, and advanced ceramics. The construction and industrial sectors continue to drive demand due to energy efficiency goals. Boron's integration into alloys and metals enhances hardness, strength, and corrosion resistance, supporting applications in manufacturing and automotive industries. Additionally, detergents and bleaches benefit from boron's cleaning efficiency and chemical stability, making it an essential component in household and industrial formulations.

North America Boron Minerals and Chemicals Market captured USD 2.2 billion in 2025. Growth is supported by advanced manufacturing sectors, including aerospace, electronics, and clean energy, which rely on high-performance boron products. Infrastructure investments, recycling initiatives, and strict environmental regulations further reinforce demand. North America benefits from well-established supply chains and robust R&D ecosystems for specialty boron chemicals.

Key players in the Global Boron Minerals and Chemicals Market industry include Rio Tinto (U.S. Borax), 3M Company, Inkabor, Searles Valley Minerals, Eti Maden, Boron Specialties, LLC, Quiborax S.A., Minera Santa Rita, Gremont Chemical Company, 5E Advanced Materials, and Elkem. Companies in the boron minerals and chemicals market are adopting diverse strategies to strengthen their market position. They are investing heavily in R&D to develop high-purity, specialty, and sustainable boron compounds for advanced applications in electronics, energy storage, and aerospace. Strategic partnerships with industrial end-users and tech firms help expand deployment in emerging sectors. Geographic expansion into high-growth regions and local production facilities ensures supply reliability. Firms are also enhancing processing technologies to improve efficiency, reduce environmental impact, and capture premium pricing. Product differentiation, intellectual property development, and targeted marketing campaigns support brand recognition and long-term market leadership while addressing evolving industrial and environmental demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Application

- 2.2.3 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing use across multiple industrial sectors

- 3.2.1.2 Rising construction and infrastructure development

- 3.2.1.3 Ongoing improvements in material performance and efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Increasing environmental regulations on mining activities

- 3.2.2.2 High production costs for refined boron chemicals

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for advanced and high-performance materials

- 3.2.3.2 Expanding focus on sustainable and efficient agriculture

- 3.2.3.3 Shift toward specialty and value-added boron products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Boron Minerals

- 5.2.1 Colemanite

- 5.2.2 Ulexite

- 5.2.3 Tourmaline

- 5.3 Boron Chemicals

- 5.3.1 Boric Acid

- 5.3.2 Borates

- 5.3.3 Anhydrous Borates

- 5.3.4 Borax

- 5.3.5 Anhydrous Borax

- 5.3.6 Boron Halides

- 5.3.6.1 Boron trichloride

- 5.3.6.2 Boron trifluoride

- 5.3.6.3 Boron tribromide

- 5.3.6.4 Others

- 5.3.7 Boric Acid Esters

- 5.3.8 Boron Hydrides

- 5.3.8.1 Closo borane

- 5.3.8.2 Nido borane

- 5.3.8.3 Arachno borane

- 5.3.9 Boron Carbide

- 5.3.10 Boron Nitride

- 5.3.10.1 Hexagonal Boron Nitride

- 5.3.10.2 Cubic Boron Nitride

- 5.3.10.3 Wurtzite Boron Nitride

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Glass and Ceramics

- 6.2.1 Borosilicate Glass

- 6.2.2 Display Glass

- 6.2.3 Textile Fiberglass

- 6.2.4 Insulation Fiberglass

- 6.2.5 Specialty Glass

- 6.2.6 Others

- 6.3 Alloy and Metals

- 6.3.1 Steel Alloys

- 6.3.2 Metal Processing

- 6.3.3 Welding & Joining

- 6.3.4 Others

- 6.4 Detergents & Bleaches

- 6.4.1 Laundry Detergents

- 6.4.2 Household Cleaners

- 6.4.3 Industrial Cleaners

- 6.4.4 Bleaching Agents

- 6.4.5 Others

- 6.5 Agrochemicals

- 6.5.1 Micronutrient Fertilizers

- 6.5.2 Soil Correction

- 6.5.3 Others

- 6.6 Adhesives

- 6.6.1 Industrial Adhesives

- 6.6.2 Construction Adhesives

- 6.6.3 Specialty Adhesives

- 6.6.4 Others

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 3M Company

- 8.2 American Borate

- 8.3 Boron Specialties, LLC

- 8.4 Eti Maden

- 8.5 Gremont Chemical Company

- 8.6 Inkabor

- 8.7 Minera Santa Rita

- 8.8 National Boraxx Corporation

- 8.9 Rio Tinto (U.S. Borax)

- 8.10 Searles Valley Minerals

- 8.11 5E Advanced Materials

- 8.12 Quiborax S.A.

硼砂市場:按類型、產品類型、等級、銷售管道和應用分類-2026-2032年全球市場預測

硼砂市場:按類型、產品類型、等級、銷售管道和應用分類-2026-2032年全球市場預測 硼嗪全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)硼基阻燃劑市場:按產品類型、形態、等級、通路和應用分類的全球預測 - 2026 年至 2032 年非晶質硼粉市場:依純度、粒徑、應用及銷售管道-2026-2032年全球預測

硼嗪全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)硼基阻燃劑市場:按產品類型、形態、等級、通路和應用分類的全球預測 - 2026 年至 2032 年非晶質硼粉市場:依純度、粒徑、應用及銷售管道-2026-2032年全球預測 硼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球硼市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

硼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球硼市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球硼市場報告科爾曼石材全球市場報告(2026年)2026年全球氮化硼塗層市場報告氮化硼塗層市場按類型、形態、塗層技術、應用和最終用途行業分類-2026-2032年全球預測

2026年全球硼市場報告科爾曼石材全球市場報告(2026年)2026年全球氮化硼塗層市場報告氮化硼塗層市場按類型、形態、塗層技術、應用和最終用途行業分類-2026-2032年全球預測