|

市場調查報告書

商品編碼

1959549

草坪及園藝設備市場機會、成長要素、產業趨勢分析及2026年至2035年預測Lawn and Garden Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

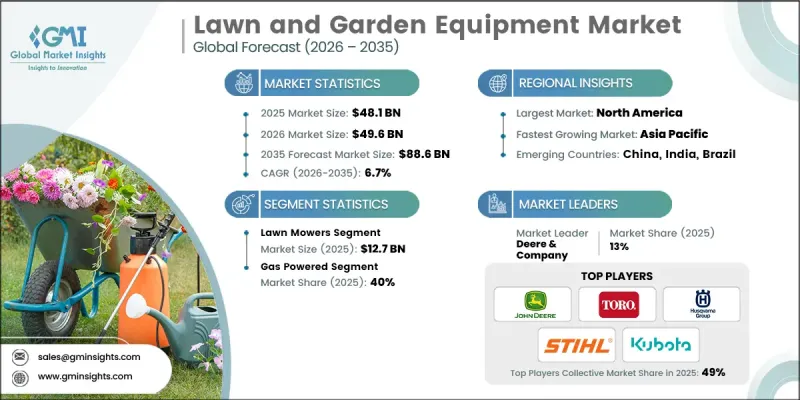

2025 年全球草坪和花園設備市場價值 481 億美元,預計到 2035 年將達到 886 億美元,年複合成長率為 6.7%。

除了住宅消費者的穩定需求外,商業和公共景觀領域的快速成長也為該產業提供了支撐。城市擴張和新住宅開發正在改變住宅對戶外空間的看法,尤其是在郊區和周邊地區,這使得草坪和花園的維護不再只是日常保養,而成為一種生活方式。這種轉變推動了對使用者友善、符合人體工學、多功能且便利的設備的需求。同時,承包商、市政當局和休閒設施等商業客戶仍需要能夠勝任繁重工作的高性能、耐用且高效的設備。季節性波動會影響購買模式,而強大的經銷商網路、租賃計劃和完善的售後服務在提高收入和培養客戶忠誠度方面發揮著至關重要的作用。技術創新,特別是電池驅動和電動設備的興起,正在重塑競爭格局,並支持市場的永續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 481億美元 |

| 預測金額 | 886億美元 |

| 複合年成長率 | 6.7% |

預計到2025年,割草機市場規模將達到127億美元。無論是在消費者領域還是專業領域,割草機被視為維護戶外空間整潔的必備設備,與其他草坪和園藝工具相比,其安裝量大規模,更換週期也更短。消費者優先考慮易用性、效率和穩定的割草性能,而專業用戶和商業用戶則需要能夠承受頻繁高強度作業的大容量割草機。園林綠化作為一種生活方式的日益普及、郊區化的推進以及人們對戶外美觀的日益重視,都進一步推動了對先進割草機設計的需求,包括自走式、機器人式和多功能型號。

預計到2025年,汽油動力設備市佔率將達到40%。汽油引擎以其耐用性、高功率和多功能性而聞名,仍然是大規模場地、專業園林綠化公司和承包商的理想選擇,因為它們需要更長的運作時間、快速加油以及即使在崎嶇不平的地形上也能保持穩定的性能。汽油動力割草機和修剪機尤其擅長修剪茂密和過長的草坪,因此對於商業園林綠化、高爾夫球場、運動場和大型住宅草坪來說必不可少。儘管電動和電池驅動的替代產品越來越受歡迎,但汽油動力工具憑藉其可靠性、強大的耐用性和對各種氣候和工作條件的適應性,仍然保持著優勢。

預計到2025年,美國草坪和花園設備市場將佔據80%的市場佔有率,市場規模將達到910億美元。推動草坪和花園設備需求成長的因素包括:濃厚的草坪養護文化、較高的住宅率以及郊區住宅普遍存在的維護需求。住宅熱衷於精心照料草坪和花園,以提升房屋外觀、保持房產價值並打造功能齊全的戶外生活空間,日常或每週的維護已成為一種普遍做法。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 技術進步

- 人們對環保和永續產品的興趣日益濃厚。

- 住宅維修和戶外休閒活動的成長

- 產業潛在風險與挑戰

- 技術進步

- 人們對環保和永續產品的興趣日益濃厚。

- 住宅維修和戶外休閒活動的成長

- 機會

- 對智慧園藝工具的需求日益成長

- 在新興市場拓展業務

- 促進因素

- 成長潛力分析

- 關鍵市場趨勢與顛覆性因素

- 未來市場趨勢

- 風險分析及緩解措施

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理情勢

- 標準和合規要求

- 認證標準

- 波特的分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費者行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 割草機

- 聯結機

- 噴灌和軟管

- 鼓風機

- 鏈鋸

- 切割機和切碎機

- 其他

第6章 市場估計與預測:依產量分類,2022-2035年

- 氣體類型

- 電的

- 手動的

- 其他

第7章 市場估計與預測:依價格分類,2022-2035年

- 低價位

- 中號

- 高價位範圍

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 住宅

- 商業的

- 其他

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 專賣店

- 家居建材商店

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Ariens Company

- Briggs &Stratton Corporation

- Deere &Company

- Falcon Garden Tools

- Fiskars Group

- Honda Motor Co., Ltd

- Husqvarna Group

- Koki Holdings Co., Ltd

- Kubota Corporation

- Makita Corporation

- Robert Bosch GmbH

- Stanley Black &Decker

- STIGA SpA

- Stihl Holding AG &Co. KG

- Techtronic Industries Co. Ltd(TTI)

- The Toro Company

The Global Lawn and Garden Equipment Market was valued at USD 48.1 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 88.6 billion by 2035.

The industry is experiencing steady demand from residential consumers alongside rapid growth in commercial and institutional landscaping sectors. Urban expansion and new housing developments have transformed how homeowners perceive their outdoor spaces, particularly in suburban and peri-urban areas, making lawn and garden care a lifestyle activity rather than simple maintenance. This shift has driven demand for equipment that is user-friendly, ergonomic, multifunctional, and convenient. At the same time, commercial clients, including contractors, municipalities, and recreational facilities, continue to demand high-performance, durable, and productive equipment capable of heavy-duty use. Seasonal fluctuations still influence purchasing patterns, but strong dealer networks, rental programs, and comprehensive after-sales services now play a key role in boosting revenue and fostering customer loyalty. Technological advancements, particularly the rise of battery-powered and electric equipment, are reshaping the competitive landscape and supporting sustainable growth in the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $48.1 Billion |

| Forecast Value | $88.6 Billion |

| CAGR | 6.7% |

The lawn mowers segment generated USD 12.7 billion in 2025. Across both consumer and contractor segments, mowers are considered indispensable for maintaining well-manicured outdoor spaces, contributing to a sizable installed base and shorter replacement cycles compared to other lawn and garden tools. Consumers prioritize ease of use, efficiency, and consistent cutting performance, while contractors and commercial users demand high-capacity mowers capable of handling frequent, heavy-duty operation. The growing trend of landscaping as a lifestyle activity, coupled with increased suburbanization and emphasis on outdoor aesthetics, is further fueling demand for advanced mower designs, including self-propelled, robotic, and multi-functional models.

The gas-powered equipment segment held a 40% share in 2025. Renowned for their durability, high power output, and versatility, gas engines remain the equipment of choice for large properties, professional landscapers, and contractors who require long operational runtime, rapid refueling, and consistent performance on uneven or challenging terrain. Gas-powered mowers and trimmers excel in cutting dense or overgrown grass, making them indispensable for commercial landscaping operations, golf courses, sports fields, and expansive residential lawns. Despite the rising popularity of electric and battery-powered alternatives, gas-powered tools maintain their dominance due to reliability, heavy-duty endurance, and adaptability across diverse climates and work conditions.

U.S. Lawn and Garden Equipment Market held 80% share, generating USD 91 billion in 2025. Lawn and garden equipment demand is driven by a deep-rooted lawn care culture, high home ownership, and widespread suburban properties that require regular upkeep. Homeowners are motivated to maintain lawns and gardens to enhance curb appeal, preserve property values, and create functional outdoor living spaces, making daily or weekly maintenance a common routine.

Key players in the Global Lawn and Garden Equipment Market include Ariens Company, Briggs & Stratton Corporation, Deere & Company, Falcon Garden Tools, Fiskars Group, Honda Motor Co., Ltd, Husqvarna Group, Koki Holdings Co., Ltd, Kubota Corporation, Makita Corporation, Robert Bosch GmbH, Stanley Black & Decker, STIGA S.p.A, Stihl Holding AG & Co. KG, Techtronic Industries Co., Ltd (TTI), and The Toro Company. Companies in the Lawn and Garden Equipment Market are strengthening their foothold by focusing on product innovation, such as ergonomic designs, battery-powered solutions, and multifunctional tools. Expanding global distribution networks and forming strategic partnerships with dealers and service providers improve market reach and customer support. Investment in digital platforms, smart connectivity, and after-sales services enhances brand loyalty, while targeted marketing campaigns build awareness among both residential and commercial customers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 regional

- 2.2.2 product type

- 2.2.3 power

- 2.2.4 price

- 2.2.5 end user

- 2.2.6 distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements

- 3.2.1.2 Increasing interest in eco-friendly and sustainable products

- 3.2.1.3 Growth in home improvement and outdoor leisure activities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Technological advancements

- 3.2.2.2 Increasing interest in eco-friendly and sustainable products

- 3.2.2.3 Growth in home improvement and outdoor leisure activities

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for smart gardening tools

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and Disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 by product type

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirement

- 3.9.2 Certification standards

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Lawn mowers

- 5.3 Tractors

- 5.4 Sprinkler and hoses

- 5.5 Blowers

- 5.6 Chain saws

- 5.7 Cutters and shredders

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By power, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Gas powered

- 6.3 Electric powered

- 6.4 Manual

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By price, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Specialty stores

- 9.3.2 Home improvement stores

- 9.3.3 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Ariens Company

- 11.2 Briggs & Stratton Corporation

- 11.3 Deere & Company

- 11.4 Falcon Garden Tools

- 11.5 Fiskars Group

- 11.6 Honda Motor Co., Ltd

- 11.7 Husqvarna Group

- 11.8 Koki Holdings Co., Ltd

- 11.9 Kubota Corporation

- 11.10 Makita Corporation

- 11.11 Robert Bosch GmbH

- 11.12 Stanley Black & Decker

- 11.13 STIGA S.p.A

- 11.14 Stihl Holding AG & Co. KG

- 11.15 Techtronic Industries Co. Ltd (TTI)

- 11.16 The Toro Company

草坪和花園設備市場規模、佔有率和成長分析:按產品類型、動力來源、最終用戶、分銷管道、應用和地區分類-2026-2033年產業預測

草坪和花園設備市場規模、佔有率和成長分析:按產品類型、動力來源、最終用戶、分銷管道、應用和地區分類-2026-2033年產業預測 草坪割草機市場-全球產業規模、佔有率、趨勢、機會和預測:按產品、最終用戶、銷售管道、地區和競爭對手分類,2021-2031年

草坪割草機市場-全球產業規模、佔有率、趨勢、機會和預測:按產品、最終用戶、銷售管道、地區和競爭對手分類,2021-2031年 草坪和花園設備市場:按設備類型、最終用戶、動力來源、銷售管道和地區分類

草坪和花園設備市場:按設備類型、最終用戶、動力來源、銷售管道和地區分類 電動園藝噴霧器市場:依電源、產品類型、應用、最終用戶、通路分類,全球預測(2026-2032)翼形遮陽篷市場:按類型、材料、產品、最終用途和分銷管道分類,全球預測,2026-2032年

電動園藝噴霧器市場:依電源、產品類型、應用、最終用戶、通路分類,全球預測(2026-2032)翼形遮陽篷市場:按類型、材料、產品、最終用途和分銷管道分類,全球預測,2026-2032年 全球天然草坪市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球割草機市場-2026-2031年預測全球草坪和花園設備產業,2025-2030 年

全球天然草坪市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球割草機市場-2026-2031年預測全球草坪和花園設備產業,2025-2030 年 全球天然草市場全球花園和草坪設備市場

全球天然草市場全球花園和草坪設備市場