|

市場調查報告書

商品編碼

1959335

移動式汽車破碎拖車市場:機會、成長要素、產業趨勢分析及2026年至2035年預測Mobile Car Crusher Trailer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

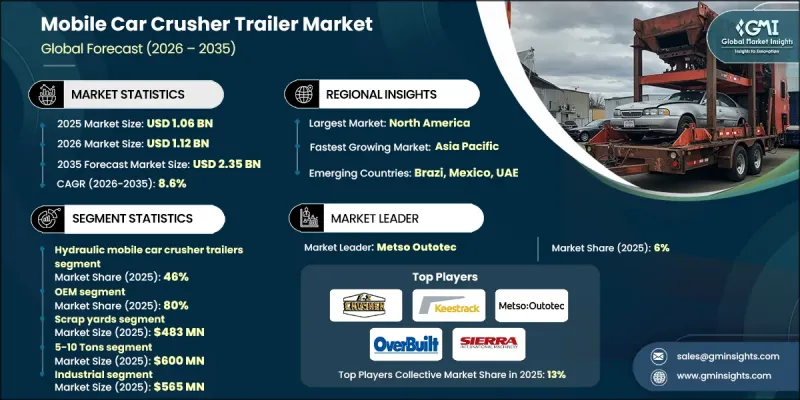

2025年全球移動式汽車破碎拖車市場價值為10.6億美元,預計2035年將達23.5億美元,年複合成長率為8.6%。

隨著全球汽車廢棄物數量的成長,在對更快、更有效率的回收流程日益成長的需求推動下,市場持續保持成長動能。更嚴格的環境政策和報廢車輛(ELV)法規合規要求促使回收商對其破碎設備進行現代化改造。廢品回收場、汽車拆解廠和工業回收設施越來越注重提高生產效率、減少排放氣體和履行安全義務,加速了對先進移動式破碎拖車的需求。現場破碎的普及也降低了運輸成本和工期延誤。擁有多個回收點的大型回收設施和廢品營運商正積極投資移動式、高容量和模組化破碎拖車,以保持營運的柔軟性和便利性。能夠處理各種車輛類型並在各種運作環境下提供穩定性能的液壓、電力和柴油系統的日益普及,進一步推動了市場成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 10.6億美元 |

| 預測金額 | 23.5億美元 |

| 複合年成長率 | 8.6% |

持續的技術創新正透過智慧製程控制、數位化性能監控、自動化安全機制和先進的動力系統,重塑移動式電動破碎拖車的運作方式。這些改進提高了破碎精度、處理能力和物料回收率,同時確保符合環境和職場標準。模組化拖車結構和預測性維護工具的整合延長了設備使用壽命並減少了停機時間。節能的電動和混合動力破碎系統也有助於降低操作人員對燃料的依賴和排放,從而提高營運效率並實現長期成本節約,同時符合不斷發展的永續性目標。

預計到2025年,液壓式移動汽車破碎拖車將佔據約46%的市場佔有率,並在2026年至2035年間以超過8.4%的複合年成長率成長。該細分市場之所以能夠保持主導地位,是因為它能夠以最小的人工干預實現可控的高強度破碎。操作人員之所以青睞液壓系統,是因為其可靠性高、能夠適應各種尺寸的車輛,並且安全性能更佳,尤其是在大批量廢料處理環境和多站點管理運營中。

預計到2025年,OEM(原始設備製造商)市佔率將達到80%,並在2035年之前以8.8%的複合年成長率成長。 OEM的領先地位得益於其能夠直接獲得設計完整、經過認證的破碎機拖車,這些拖車具有耐用性、客製化選項和整合合規功能等優勢。終端用戶更傾向於選擇OEM解決方案,因為其提供保固服務、技術支持,並且能夠滿足嚴格的營運和監管標準,這使其成為大型回收網路中的首選採購方案。

預計2025年,美國移動式汽車破碎拖車市場規模將達3.146億美元,市佔率高達83%。該地區受益於完善的汽車回收基礎設施和先進移動破碎技術的廣泛應用。持續增加對自動化、數位監控和高容量拖車解決方案的投資,使北美在高效、技術主導的汽車回收領域處於領先地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 汽車報廢和回收需求日益成長

- 技術進步

- 環境與監理合規

- 工業廢棄物處理廠及廢料堆場擴建

- 產業潛在風險與挑戰

- 較高的初始投資和維護成本

- 市場分散且標準化程度低

- 市場機遇

- 對現場和攜帶式回收設備的需求增加

- 新興市場和未開發地區

- 電動和混合動力破碎機拖車

- 專注永續性和循環經濟

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國:EPA、OSHA 和 RCRA 合規指南

- 加拿大稅務局 (CRA) 和加拿大環境與氣候變遷部的指導方針。

- 歐洲

- 德國:聯邦環境部和報廢車輛法規

- 法國:生態系統轉型部和報廢車輛指南

- 英國:環境署和廢棄物管理條例

- 義大利:環境部和報廢車輛合規性

- 亞太地區

- 中國:生態環境部標準

- 日本:經濟產業省及廢棄電子電氣設備回收法

- 韓國:環境部及報廢車輛法規

- 印度:環境、森林及氣候變遷部及汽車報廢政策

- 拉丁美洲

- 巴西:國家環境委員會 (CONAMA) 和回收標準

- 墨西哥:環境部(SEMARNAT)指南

- 中東和非洲

- 阿拉伯聯合大公國:環境署 - 阿布達比和聯邦標準

- 沙烏地阿拉伯:沙烏地阿拉伯標準、計量和品質研究院

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 使用案例場景

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估算與預測:依電源類型分類,2022-2035年

- 液壓移動式車輛破碎拖車

- 柴油動力移動式車輛破碎拖車

- 電動移動式汽車粉碎拖車

- 其他

第6章 市場估計與預測:依產能分類,2022-2035年

- 5-10噸

- 5噸或以下

- 超過10噸

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 廢品場

- 汽車回收

- 建設與拆除

- 緊急應變

- 軍事用途

- 其他

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 工業的

- 商業的

- 對於地方政府

- 其他

第9章 市場估價與預測:依通路分類,2022-2035年

- OEM

- 售後市場

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第11章:公司簡介

- Global Player

- Al-jon Manufacturing

- Eagle Crusher Company

- EZ Crusher

- Hammel Recyclingtechnik

- Keestrack

- McCloskey International

- Metso Outotec

- OverBuilt

- Sandvik

- Sierra International Machinery

- Regional Player

- BENLEE

- Big Mac

- Enerpat

- Gensco Equipment

- Granutech-Saturn Systems

- RM Johnson Company

- SAS of Luxemburg

- The Auto Crusher

- VYKIN Crushers

- Youngs Auto Center &Salvage

- 新興企業

- Baichy Heavy Industrial Machinery

- Fabo Company

- Guangxi Mesda Engineering Machinery

- SBM Mineral Processing

- Senya Crushers

The Global Mobile Car Crusher Trailer Market was valued at USD 1.06 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 2.35 billion by 2035.

The market continues to gain momentum as rising vehicle retirement rates worldwide increase the need for faster and more efficient recycling processes. Tighter environmental policies and End-of-Life Vehicle compliance requirements are pushing recycling operators to modernize their crushing infrastructure. Scrap yards, vehicle dismantlers, and industrial recycling facilities are increasingly focused on improving productivity, lowering emissions, and meeting safety obligations, which is accelerating demand for advanced mobile crusher trailers. The growing shift toward on-site crushing is also reducing transportation costs and operational delays. Large-scale recycling facilities and multi-site scrap operators are actively investing in mobile, high-capacity, and modular crusher trailers to maintain flexibility and operational control. Market growth is further supported by increasing adoption of hydraulic, electric, and diesel-powered systems designed to handle diverse vehicle types while delivering consistent performance across varied operating environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.06 Billion |

| Forecast Value | $2.35 Billion |

| CAGR | 8.6% |

Ongoing innovation is reshaping mobile car crusher trailer operations through intelligent process controls, digitally enabled performance monitoring, automated safety mechanisms, and advanced power systems. These improvements enhance crushing accuracy, increase throughput, and improve material recovery while ensuring compliance with environmental and workplace standards. The integration of modular trailer structures and predictive maintenance tools is extending equipment lifespan and reducing downtime. Energy-efficient electric and hybrid crusher systems are also helping operators reduce fuel dependency and emissions, allowing them to achieve higher operational efficiency and lower long-term costs while aligning with evolving sustainability targets.

Hydraulic mobile car crusher trailers accounted for roughly 46% of the total market share in 2025 and are projected to grow at a CAGR exceeding 8.4% from 2026 to 2035. This segment continues to lead due to its ability to deliver controlled, high-force crushing with minimal manual handling. Operators favor hydraulic systems for their reliability, adaptability to different vehicle sizes, and enhanced safety performance, particularly in high-volume scrappage environments and operations managing multiple sites.

The OEM segment held 80% share in 2025 and is forecast to grow at a CAGR of 8.8% through 2035. OEM dominance is driven by direct access to fully engineered and certified crusher trailers that offer durability, customization options, and integrated compliance features. End users prioritize OEM solutions for their warranty coverage, technical support, and ability to meet strict operational and regulatory standards, making them the preferred procurement choice across large recycling networks.

United States Mobile Car Crusher Trailer Market held 83% share and reached USD 314.6 million in 2025. The region benefits from a well-established vehicle recycling infrastructure and widespread deployment of advanced mobile crushing technologies. Strong investment in automation, digital monitoring, and high-capacity trailer solutions continues to position North America at the forefront of efficient and technology-driven vehicle recycling.

Key companies active in the Global Mobile Car Crusher Trailer Market include Metso Outotec, Sandvik, Al jon Manufacturing, Sierra International Machinery, Eagle Crusher Company, McCloskey International, OverBuilt, EZ Crusher, Hammel Recyclingtechnik, and Keestrack. Companies operating in the mobile car crusher trailer market are strengthening their market position through continuous product innovation, strategic equipment upgrades, and expanded service offerings. Manufacturers are focusing on developing higher-capacity trailers with improved energy efficiency and advanced control systems to meet evolving customer demands. Many players are investing in modular designs and smart monitoring technologies to enhance flexibility and reduce maintenance costs. Strategic partnerships with recycling operators and regional distributors are helping companies expand their geographic reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Power Source

- 2.2.3 Capacity

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Vehicle Scrappage & Recycling Needs

- 3.2.1.2 Technological Advancements

- 3.2.1.3 Environmental & Regulatory Compliance

- 3.2.1.4 Expansion of Industrial & Scrap Yard Operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Investment & Maintenance Costs

- 3.2.2.2 Fragmented Market & Limited Standardization

- 3.2.3 Market opportunities

- 3.2.3.1 Rising Demand for On-Site and Portable Recycling

- 3.2.3.2 Emerging Markets & Untapped Regions

- 3.2.3.3 Electric & Hybrid Crusher Trailers

- 3.2.3.4 Sustainability and Circular Economy Focus

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, OSHA, and RCRA Compliance Guidelines

- 3.4.1.2 Canada Revenue Agency (CRA) & Environment and Climate Change Canada Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: Federal Ministry for the Environment & ELV Regulations

- 3.4.2.2 France: Ministry of Ecological Transition & ELV Guidelines

- 3.4.2.3 UK: Environment Agency & Waste Regulations

- 3.4.2.4 Italy: Ministry of Environment & ELV Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Ecology and Environment Standards

- 3.4.3.2 Japan: Ministry of Economy, Trade and Industry & ELV Recycling Law

- 3.4.3.3 South Korea: Ministry of Environment & ELV Regulations

- 3.4.3.4 India: Ministry of Environment, Forest and Climate Change & Vehicle Scrappage Policy

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Environment Council (CONAMA) & Recycling Standards

- 3.4.4.2 Mexico: SEMARNAT Guidelines

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Environment Agency - Abu Dhabi & Federal Standards

- 3.4.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Power Source, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hydraulic Mobile Car Crusher Trailers

- 5.3 Diesel-Powered Mobile Car Crusher Trailers

- 5.4 Electric Mobile Car Crusher Trailers

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Capacity, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 5-10 Tons

- 6.3 Up to 5 Tons

- 6.4 Above 10 Tons

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Scrap Yards

- 7.3 Automotive Recycling

- 7.4 Construction & Demolition

- 7.5 Emergency Response

- 7.6 Military

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.3 Commercial

- 8.4 Municipal

- 8.5 Other

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 Al-jon Manufacturing

- 11.1.2 Eagle Crusher Company

- 11.1.3 EZ Crusher

- 11.1.4 Hammel Recyclingtechnik

- 11.1.5 Keestrack

- 11.1.6 McCloskey International

- 11.1.7 Metso Outotec

- 11.1.8 OverBuilt

- 11.1.9 Sandvik

- 11.1.10 Sierra International Machinery

- 11.2 Regional Player

- 11.2.1 BENLEE

- 11.2.2 Big Mac

- 11.2.3 Enerpat

- 11.2.4 Gensco Equipment

- 11.2.5 Granutech-Saturn Systems

- 11.2.6 RM Johnson Company

- 11.2.7 SAS of Luxemburg

- 11.2.8 The Auto Crusher

- 11.2.9 VYKIN Crushers

- 11.2.10 Youngs Auto Center & Salvage

- 11.3 Emerging Players

- 11.3.1 Baichy Heavy Industrial Machinery

- 11.3.2 Fabo Company

- 11.3.3 Guangxi Mesda Engineering Machinery

- 11.3.4 SBM Mineral Processing

- 11.3.5 Senya Crushers

移動式破碎篩分機市場報告:按產品類型、應用、最終用戶和地區分類,2026-2034年

移動式破碎篩分機市場報告:按產品類型、應用、最終用戶和地區分類,2026-2034年 行動式火葬場市場規模、佔有率和成長分析:按燃料/動力來源、行動平台、系統技術、應用和地區分類-2026-2033年產業預測

行動式火葬場市場規模、佔有率和成長分析:按燃料/動力來源、行動平台、系統技術、應用和地區分類-2026-2033年產業預測 半移動式破碎站市場:按破碎機類型、動力來源、應用和終端用戶產業分類-全球預測,2026-2032年

半移動式破碎站市場:按破碎機類型、動力來源、應用和終端用戶產業分類-全球預測,2026-2032年 全球移動式破碎篩分機市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球移動式破碎篩分機市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 2026年全球移動式破碎篩分機市場報告

2026年全球移動式破碎篩分機市場報告 行動破碎分選市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、機械類型、最終用戶產業、地區和競爭格局分類,2021-2031年

行動破碎分選市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、機械類型、最終用戶產業、地區和競爭格局分類,2021-2031年 移動式破碎篩分機市場規模、佔有率及成長分析(依產品類型、應用、最終用戶及地區分類)-2026-2033年產業預測

移動式破碎篩分機市場規模、佔有率及成長分析(依產品類型、應用、最終用戶及地區分類)-2026-2033年產業預測 北美行動式破碎分類機市場:市場規模、佔有率、趨勢分析(按類型、應用和國家分類)、細分市場預測(2025-2033 年)行動碎紙機和篩選機市場規模、佔有率和趨勢分析報告:按類型、按應用、按地區、細分市場預測,2025-2030 年

北美行動式破碎分類機市場:市場規模、佔有率、趨勢分析(按類型、應用和國家分類)、細分市場預測(2025-2033 年)行動碎紙機和篩選機市場規模、佔有率和趨勢分析報告:按類型、按應用、按地區、細分市場預測,2025-2030 年 日本的移動式碾碎機及篩分機市場評估:類型·終端用戶產業·行動類型·各地區的機會及預測 (2018-2032年)

日本的移動式碾碎機及篩分機市場評估:類型·終端用戶產業·行動類型·各地區的機會及預測 (2018-2032年)