|

市場調查報告書

商品編碼

1959334

石油和天然氣產業操作員培訓模擬器市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Oil and Gas OTS Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

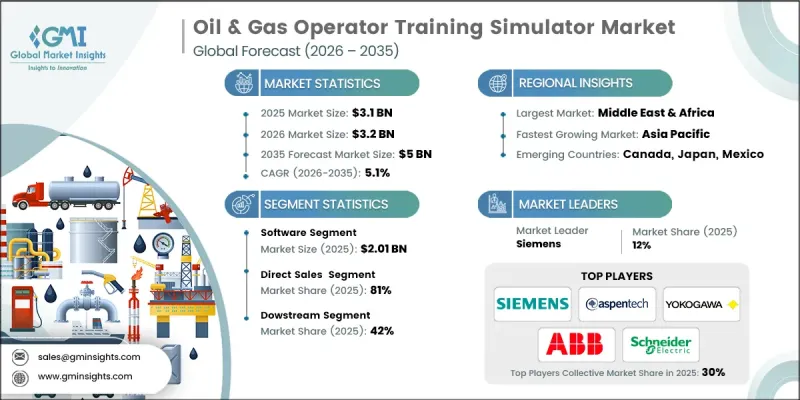

2025 年,全球石油和天然氣產業操作員訓練模擬器市場價值 31 億美元,預計到 2035 年將達到 50 億美元,年複合成長率為 5.1%。

該市場的成長源自於石油和天然氣作業固有的高風險性。高壓、極端溫度、危險化學品和複雜的製程流程,一旦出現人為失誤,都可能導致災難性事故。煉油、海上作業和天然氣加工作業中發生的嚴重事故凸顯了提高人員操作水準和採取積極主動的安全措施的必要性。操作員訓練模擬器 (OTS) 透過提供逼真的虛擬環境,使操作員能夠練習日常操作、異常情況和緊急情況,從而在降低操作風險方面發揮核心作用。這些模擬器使操作員能夠安全地體驗真實作業的壓力和要求。除了安全之外,人們的關注點正轉向積極主動的風險管理和損失預防。企業擴大使用 OTS 來模擬潛在故障、檢驗安全程序並評估操作員在高壓情況下的反應。這使得在實際事故發生之前識別培訓和操作程序中的不足成為可能,從而提高營運可靠性和員工能力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 31億美元 |

| 預測金額 | 50億美元 |

| 複合年成長率 | 5.1% |

預計到2025年,軟體領域將創造20.1億美元的收入。該軟體是OTS系統的核心,涵蓋製程模擬引擎、動態數學建模、模擬控制邏輯和場景管理工具。這款高精度軟體基於從實際工廠運作中推導出的第一原理過程模式,確保對操作員的操作做出逼真的回應。透過模擬虛擬工廠環境,操作員可以在與實際運作幾乎相同的條件下學習技能、做出明智的決策並提高安全回應能力。這使得該軟體對於有效的操作員培訓和持續的人才培養至關重要。

到2025年,銷售管道將佔據81%的市場佔有率。現成解決方案(OTS)技術複雜、可客製化性強且資本密集,因此更適合與供應商直接合作。供應商與燃氣公司緊密合作,創建工廠專屬模型,整合分散式控制系統(DCS),並開發反映實際操作流程的培訓方案。這種方法使營運商能夠掌控系統設計、品質和生命週期支援。直銷還有助於加強製造商與客戶之間的關係,從而改善安裝後支援並創造長期價值。

預計到2025年,美國油氣產業操作員訓練模擬器市場將佔據83%的佔有率,市場規模將達到7億美元。憑藉其龐大的煉油能力、液化天然氣出口基礎設施以及先進的上游和中游業務,美國市場在全球佔據主導地位。高度自動化的設施、嚴格的安全法規和環境監測正在推動對高保真DCS整合式操作員培訓模擬器(OTS)解決方案的需求。美國本土的OTS供應商和自動化廠商正積極推廣先進解決方案的應用,包括基於雲端的模擬工具、數位雙胞胎平台和基於績效的操作員評估系統。油氣活動活躍的州正在加速採用這些技術,並將安全、效率和合規性放在首位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 人們越來越關注營運安全和風險降低

- 監管和合規要求

- 數位轉型 工業4.0

- 產業潛在風險與挑戰

- 前期成本高

- 技術複雜性和維護負擔

- 機會

- 與數位雙胞胎和人工智慧的整合

- 模組化和雲端支援的OTS模型

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按組件

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估計與預測:依組件分類,2022-2035年

- 硬體

- 軟體

- 控制仿真

- 過程模擬

- 身臨其境型模擬

- 服務

- 諮詢

- 安裝和環境模擬

- 維護和支援

第6章 市場估算與預測:依部署模式分類,2022-2035年

- 現場

- 基於雲端的

- 混合

第7章 市場估計與預測:依業務部門分類,2022-2035年

- 上游業務

- 中游業務

- 下游業務

第8章 市場估計與預測:依營運區分,2022-2035年

- 主機操作員培訓

- 現場操作員培訓

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- ABB

- ANDRITZ

- Aspen Technology

- AVEVA Group Limited

- Designing Digitally

- DNV AS

- DuPont

- EON Reality

- ESI Group

- Hyperion Group

- Schneider Electric

- Siemens

- Tecnatom

- TRAX Energy Solutions

- Yokogawa Electric

The Global Oil & Gas Operator Training Simulator Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 5 billion by 2035.

The market's growth is driven by the inherently high-risk nature of oil and gas operations, where high pressure, extreme temperatures, hazardous chemicals, and complex processes can lead to catastrophic events if errors occur. Historically, major accidents in refining, offshore, and gas processing operations have emphasized the need for enhanced human performance and preventive safety measures. Operator Training Simulators (OTS) have become central to reducing operational risks by providing realistic virtual environments where operators can practice routine, abnormal, and emergency scenarios. These simulators allow operators to experience the pressures and demands of real-world operations safely. In addition to safety, the focus has shifted to proactive risk management and loss prevention. Companies are increasingly using OTS to simulate potential failures, test safety procedures, and evaluate operator responses to high-stress situations. This enables identification of gaps in training and operational procedures before actual incidents occur, improving both operational reliability and workforce competence.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $5 Billion |

| CAGR | 5.1% |

In 2025, the software segment generated USD 2.01 billion. Software forms the core of OTS systems, encompassing process simulation engines, dynamic mathematical modeling, emulated control logic, and scenario management tools. High-fidelity software relies on first-principle process models derived from actual plant performance, ensuring realistic responses to operator actions. By recreating a virtual plant environment, the software allows operators to develop skills, make informed decisions, and improve safety readiness in conditions nearly identical to real operations. This makes software indispensable for effective operator training and continuous workforce development.

The direct sales channel segment held 81% share in 2025. The high level of technical complexity, customization, and capital intensity of OTS solutions drives the preference for direct engagement with suppliers. Vendors collaborate closely with oil and gas companies to create plant-specific models, integrate with Distributed Control Systems (DCS), and ensure training scenarios reflect actual operating procedures. This approach allows operators to maintain control over system design, quality, and lifecycle support. Direct sales also foster stronger relationships between manufacturers and clients, enhancing post-installation support and long-term value.

U.S. Oil & Gas Operator Training Simulator Market captured 83% share, generating USD 0.7 billion in 2025. The U.S. market leads globally due to its extensive refining capacity, LNG export infrastructure, and advanced upstream and midstream operations. Highly automated facilities, stringent safety regulations, and environmental oversight drive demand for DCS-integrated OTS solutions with high fidelity. U.S.-based OTS suppliers and automation vendors actively promote the adoption of advanced solutions, including cloud-based simulation tools, digital twin platforms, and performance-based operator assessment systems. States with significant oil and gas activity are accelerating the deployment of these technologies, emphasizing safety, efficiency, and regulatory compliance.

Key players operating in the Global Oil & Gas Operator Training Simulator Market include ABB, Aspen Technology, ANDRITZ, AVEVA Group Limited, Designing Digitally, DNV AS, DuPont, EON Reality, ESI Group, Hyperion Group, Schneider Electric, Siemens, Tecnatom, TRAX Energy Solutions, and Yokogawa Electric. Companies in the Oil & Gas Operator Training Simulator Market are strengthening their presence by investing in high-fidelity simulation software, cloud-enabled platforms, and scenario libraries covering routine, abnormal, and emergency operations. Strategic collaborations with oil and gas operators help ensure simulators are tailored to plant-specific processes and DCS configurations. Firms are expanding service offerings, including operator performance assessments, training analytics, and remote access to simulation environments. Adoption of digital twin technology, real-time monitoring, and AI-driven evaluation tools differentiates providers and enhances value delivery.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment model

- 2.2.4 Operations

- 2.2.5 Environmental simulation

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing focus on operational safety & risk reduction

- 3.2.1.2 Regulatory & compliance requirements

- 3.2.1.3 Digital transformation & industry 4.0

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront cost

- 3.2.2.2 Technical complexity & maintenance burden

- 3.2.3 Opportunities

- 3.2.3.1 Integration with digital twins & AI

- 3.2.3.2 Modular & cloud-enabled OTS models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By component

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.3.1 Control simulation

- 5.3.2 Process simulation

- 5.3.3 Immersive simulation

- 5.4 Services

- 5.4.1 Consulting

- 5.4.2 Installation & environmental simulation

- 5.4.3 Maintenance & support

Chapter 6 Market Estimates and Forecast, By Deployment Model, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 On-Premises

- 6.3 Cloud-based

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Operations, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Upstream operations

- 7.3 Midstream operations

- 7.4 Downstream operations

Chapter 8 Market Estimates and Forecast, By Operations, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Console operator training

- 8.3 Field operator training

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 ANDRITZ

- 11.3 Aspen Technology

- 11.4 AVEVA Group Limited

- 11.5 Designing Digitally

- 11.6 DNV AS

- 11.7 DuPont

- 11.8 EON Reality

- 11.9 ESI Group

- 11.10 Hyperion Group

- 11.11 Schneider Electric

- 11.12 Siemens

- 11.13 Tecnatom

- 11.14 TRAX Energy Solutions

- 11.15 Yokogawa Electric

數位油田市場:2026-2032年全球市場預測(依解決方案、流程、技術和營運模式分類)數位油田解決方案市場:2026-2032年全球市場預測(按解決方案類型、組件、應用、最終用戶和部署模式分類)

數位油田市場:2026-2032年全球市場預測(依解決方案、流程、技術和營運模式分類)數位油田解決方案市場:2026-2032年全球市場預測(按解決方案類型、組件、應用、最終用戶和部署模式分類) 全球石油天然氣產業人工智慧和機器學習市場:按組件、部署、技術、應用、產業細分、最終用戶和地區分類-市場規模、市場動態、機會分析和預測(2026-2035)

全球石油天然氣產業人工智慧和機器學習市場:按組件、部署、技術、應用、產業細分、最終用戶和地區分類-市場規模、市場動態、機會分析和預測(2026-2035) 數位油田市場:按解決方案、製程、應用和地區分類,2026-2034 年

數位油田市場:按解決方案、製程、應用和地區分類,2026-2034 年 數位油田市場:按解決方案、流程、服務、應用、最終用戶、技術、組件和區域分類

數位油田市場:按解決方案、流程、服務、應用、最終用戶、技術、組件和區域分類 2026年全球數位化油田市場報告

2026年全球數位化油田市場報告 全球數位化油田市場:市場規模、佔有率和趨勢分析(按解決方案、應用、製程和地區分類),細分市場預測(2026-2033 年)2026年全球互聯油田市場報告2026年全球數位化油田解決方案市場報告

全球數位化油田市場:市場規模、佔有率和趨勢分析(按解決方案、應用、製程和地區分類),細分市場預測(2026-2033 年)2026年全球互聯油田市場報告2026年全球數位化油田解決方案市場報告 數位油田市場-全球產業規模、佔有率、趨勢、機會及預測(依製程、技術、地區及競爭格局分類,2021-2031年)

數位油田市場-全球產業規模、佔有率、趨勢、機會及預測(依製程、技術、地區及競爭格局分類,2021-2031年)