|

市場調查報告書

商品編碼

1959333

工業致動器市場機會、成長要素、產業趨勢分析及2026年至2035年預測Industrial Actuators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

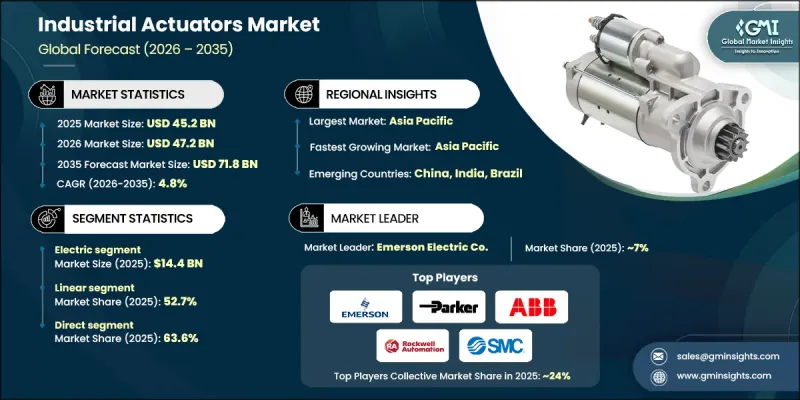

2025年全球工業致動器市場價值為452億美元,預計2035年將以4.8%的複合年成長率成長至718億美元。

這一成長反映了自動化生產系統日益普及,旨在提高營運效率、增強精度並支援可擴展的製造產量。致動器能夠實現自動化設備內的可控運動,並已成為現代運動控制系統的基本組成部分。隨著自動化在整個生產環境中不斷深入,對致動器技術的依賴性也進一步增強。製造流程的持續進步推動著致動器設計、性能和整合能力的穩步提升。製造商越來越傾向於根據自動化應對力設定生產力和效率目標,直接提升了先進致動器解決方案的重要性。因此,致動器技術的持續創新預計將在全球工業自動化發展中繼續發揮核心作用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 452億美元 |

| 預測金額 | 718億美元 |

| 複合年成長率 | 4.8% |

預計到2025年,電動致動器器市場規模將達到144億美元,並在2026年至2035年間以4.6%的複合年成長率成長。這些系統因其高能源效率、低維護需求以及與數位控制平台的無縫相容性而日益受到青睞。與液壓和氣動執行器相比,電動致動器能耗更低,並能支援更精確的運動控制。它們能夠與感測器、連接系統和預測性監控工具整合,這為現代自動化框架和永續性目標奠定了基礎。這些優勢使電動致動器成為未來自動化投資的首選。

預計到2025年,線性致動器市佔率將達到52.7%,並在2035年之前以4.1%的複合年成長率成長。線性致動器因其性能可靠、設計簡潔和功能適應性強而備受青睞。其在工業運動系統和流量控制系統中的廣泛應用,使其成為重要的收入來源。此細分市場的強勁地位凸顯了線性運動解決方案在工廠營運和設備基礎設施中發揮的結構性作用。

美國工業致動器市場預計到2025年將達到60億美元,並在2026年至2035年間以4.9%的複合年成長率成長。憑藉其先進的自動化生態系統和對精密運動技術的高需求,美國在北美市場佔據主導地位。對大規模工業基礎設施的大力投資和持續的製程最佳化正在推動致動器的應用。成熟的製造業基礎也為市場帶來了益處,該基礎優先考慮效率、可靠性和先進的控制能力。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 工業自動化和機器人應用日益普及

- 對節能和精確控制系統的需求

- 智慧製造(工業4.0)的發展

- 挑戰與困難

- 先進致動器高成本

- 對技能型專業人員的需求

- 機會

- 電動致動器的應用日益廣泛

- 亞太及新興市場擴張

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監理情勢

- 北美洲

- 美國:消費品安全委員會(CPSC)聯邦法規(CFR)第16篇第1512部分

- 加拿大:國際標準化組織(ISO)4210

- 歐洲

- 德國:德國標準化協會 (DIN)、歐洲標準 (EN)、ISO 4210

- 英國:歐洲標準 (EN) ISO 4210 /英國合格評定 (UKCA)

- 法國:歐洲標準 (EN) ISO 4210

- 亞太地區

- 中國:國家標準(GB)3565

- 印度:印度標準 (IS) 10613

- 日本:日本工業標準(JIS)D 9110

- 拉丁美洲

- 巴西:巴西技術標準協會 (ABNT)、巴西標準局 (NBR)、ISO 4210

- 墨西哥:國際標準化組織(ISO)4210

- 中東和非洲

- 南非:南非國家標準 (SANS) 311

- 沙烏地阿拉伯:沙烏地阿拉伯標準、計量和品質組織 (SASO)、海灣標準化組織 (GSO)、ISO 4210

- 北美洲

- 貿易統計(HS編碼 - 84819090)

- 主要進口國

- 主要出口國

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 電

- 氣動型

- 油壓

- 其他

第6章 市場估計與預測:依營運類型分類,2022-2035年

- 直線

- 旋轉式

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 閥門

- 泵浦

- 阻尼器

- 輸送帶

- 機器人技術

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 石油和天然氣

- 發電

- 水處理和污水處理

- 化工/石油化工

- 食品/飲料

- 製藥

- 採礦和金屬

- 汽車/製造業

- 航太/國防

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- ABB

- Curtiss-Wright

- Eaton Corporation plc

- Emerson Electric Co.

- Festo AG &Co. KG

- Flowserve Corporation

- IMI Critical Engineering

- KITZ Corporation

- Moog Inc.

- Parker Hannifin Corp

- Rockwell Automation

- Rotork plc

- SMC Corporation

- Tolomatic, Inc.

- Venture MFG. Co.

The Global Industrial Actuators Market was valued at USD 45.2 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 71.8 billion by 2035.

The growth reflects the increasing adoption of automated production systems designed to enhance operational efficiency, improve precision, and support scalable manufacturing output. Actuators enable controlled motion within automated equipment, making them a foundational element of modern motion control systems. As automation deepens across production environments, reliance on actuator technology continues to intensify. Ongoing advancements in manufacturing processes are prompting consistent upgrades in actuator design, performance, and integration capabilities. Manufacturers increasingly define their productivity and efficiency goals around automation readiness, which directly elevates the importance of advanced actuator solutions. Continuous innovation in actuator technology is therefore expected to remain central to the evolution of industrial automation worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.2 Billion |

| Forecast Value | $71.8 Billion |

| CAGR | 4.8% |

The electric actuators segment generated USD 14.4 billion in 2025 and is expected to grow at a CAGR of 4.6% from 2026 to 2035. These systems are gaining preference due to higher energy efficiency, reduced servicing requirements, and smooth compatibility with digital control platforms. Compared to hydraulic and pneumatic alternatives, electric actuators consume less energy and support more precise motion control. Their ability to integrate with sensors, connected systems, and predictive monitoring tools supports modern automation frameworks and sustainability goals. The advantages position electric actuators as a primary choice for future automation investments.

The linear actuator segment accounted for 52.7% share in 2025 and is forecast to grow at a CAGR of 4.1% through 2035. Linear actuators are valued for dependable performance, design simplicity, and broad functional adaptability. Their extensive deployment across industrial motion and flow control systems has established them as a dominant revenue contributor. The segment's strong position highlights the structural role linear motion solutions play within plant operations and equipment infrastructure.

U.S. Industrial Actuators Market reached USD 6 billion in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035. The country holds a leading share within North America due to its advanced automation ecosystem and high demand for precision motion technologies. Strong investment in large-scale industrial infrastructure and process optimization continues to support actuator adoption. The market benefits from a mature manufacturing base that prioritizes efficiency, reliability, and advanced control capabilities.

Key companies operating in the Global Industrial Actuators Market include Parker Hannifin Corp, ABB, Emerson Electric Co., SMC Corporation, Rotork plc, Eaton Corporation plc, Rockwell Automation, Flowserve Corporation, Moog Inc., Festo AG & Co. KG, Curtiss-Wright, IMI Critical Engineering, KITZ Corporation, Tolomatic, Inc., and Venture MFG. Co. Companies in the industrial actuators market focus on technology innovation, portfolio expansion, and strategic partnerships to strengthen their market position. Many players invest heavily in research and development to enhance energy efficiency, precision, and digital compatibility. Integration of smart features such as condition monitoring and predictive maintenance is a key priority. Firms also pursue mergers, acquisitions, and collaborations to expand geographic reach and access new customer segments. Customization capabilities and application-specific solutions help suppliers differentiate their offerings. Additionally, manufacturers emphasize sustainability initiatives and compliance with evolving industrial standards to reinforce long-term competitiveness and customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Motion Type

- 2.2.4 Application

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising industrial automation & robotics adoption

- 3.2.1.2 Demand for energy-efficient & precise control systems

- 3.2.1.3 Growth of smart manufacturing (industry 4.0)

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High cost of advanced actuators

- 3.2.2.2 Requirement for skilled professionals

- 3.2.3 Opportunities

- 3.2.3.1 Rising adoption of electric actuators

- 3.2.3.2 Expansion in Asia Pacific & emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.1.1 US: Consumer Product Safety Commission (CPSC) 16 Code of Federal Regulations (CFR) part 1512

- 3.7.1.2 Canada: International Organization for Standardization (ISO) 4210

- 3.7.2 Europe

- 3.7.2.1 Germany: Deutsches Institut fur Normung (DIN) European Norm (EN) ISO 4210

- 3.7.2.2 UK: European Norm (EN) ISO 4210 / United Kingdom Conformity Assessed (UKCA)

- 3.7.2.3 France: European Norm (EN) ISO 4210

- 3.7.3 Asia Pacific

- 3.7.3.1 China: Guobiao (GB) 3565

- 3.7.3.2 India: Indian Standard (IS) 10613

- 3.7.3.3 Japan: Japanese Industrial Standard (JIS) D 9110

- 3.7.4 Latin America

- 3.7.4.1 Brazil: Associacao Brasileira de Normas Tecnicas (ABNT) Norma Brasileira (NBR) ISO 4210

- 3.7.4.2 Mexico: International Organization for Standardization (ISO) 4210

- 3.7.5 Middle East & Africa

- 3.7.5.1 South Africa: South African National Standard (SANS) 311

- 3.7.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization (SASO) Gulf Standardization Organization (GSO) ISO 4210

- 3.7.1 North America

- 3.8 Trade statistics (HS code- 84819090)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Electric

- 5.3 Pneumatic

- 5.4 Hydraulic

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Motion Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Linear

- 6.3 Rotary

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Valves

- 7.3 Pumps

- 7.4 Dampers

- 7.5 Conveyors

- 7.6 Robotics

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Oil & gas

- 8.3 Power generation

- 8.4 Water & wastewater treatment

- 8.5 Chemical & petrochemical

- 8.6 Food & beverage

- 8.7 Pharmaceuticals

- 8.8 Mining & metals

- 8.9 Automotive & manufacturing

- 8.10 Aerospace & defense

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Curtiss-Wright

- 11.3 Eaton Corporation plc

- 11.4 Emerson Electric Co.

- 11.5 Festo AG & Co. KG

- 11.6 Flowserve Corporation

- 11.7 IMI Critical Engineering

- 11.8 KITZ Corporation

- 11.9 Moog Inc.

- 11.10 Parker Hannifin Corp

- 11.11 Rockwell Automation

- 11.12 Rotork plc

- 11.13 SMC Corporation

- 11.14 Tolomatic, Inc.

- 11.15 Venture MFG. Co.

2026年全球感測器和執行器市場報告

2026年全球感測器和執行器市場報告 汽車壓電陶瓷元件市場:依元件類型、材料類型、應用、車輛類型和銷售管道分類-2026-2032年全球市場預測

汽車壓電陶瓷元件市場:依元件類型、材料類型、應用、車輛類型和銷售管道分類-2026-2032年全球市場預測 壓電堆疊致動器市場報告:至2035年的趨勢、預測與競爭分析阻尼器致動器市場:按致動器類型、控制模式、應用和安裝配置分類的全球市場預測 - 2026-2032 年液壓線性致動器市場:2026-2032年全球市場預測(依致動器類型、工作壓力、行程長度、終端用戶產業、應用程式和銷售管道)

壓電堆疊致動器市場報告:至2035年的趨勢、預測與競爭分析阻尼器致動器市場:按致動器類型、控制模式、應用和安裝配置分類的全球市場預測 - 2026-2032 年液壓線性致動器市場:2026-2032年全球市場預測(依致動器類型、工作壓力、行程長度、終端用戶產業、應用程式和銷售管道) 航太致動器市場預測至2034年-按類型、平台、技術、應用、最終用戶和地區分類的全球分析

航太致動器市場預測至2034年-按類型、平台、技術、應用、最終用戶和地區分類的全球分析 安全致動器市場規模、佔有率和成長分析:按類型、最終用途和地區分類 - 2026-2033 年行業預測基於形狀記憶合金(SMA)的致動器市場:按應用程式、致動器類型、合金類型、最終用戶和分銷管道分類,全球預測,2026-2032年

安全致動器市場規模、佔有率和成長分析:按類型、最終用途和地區分類 - 2026-2033 年行業預測基於形狀記憶合金(SMA)的致動器市場:按應用程式、致動器類型、合金類型、最終用戶和分銷管道分類,全球預測,2026-2032年 2026-2034年奈米定位致動器全球市場規模、佔有率、趨勢和成長分析報告

2026-2034年奈米定位致動器全球市場規模、佔有率、趨勢和成長分析報告 日本家用保險箱市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年

日本家用保險箱市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年