|

市場調查報告書

商品編碼

1959327

經腸營養原料市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Enteral Nutrition Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球經腸營養成分市場價值為 43.1 億美元,預計到 2035 年將達到 85.8 億美元,年複合成長率為 7.3%。

市場擴張的驅動力在於慢性病盛行率上升和臨床營養解決方案需求成長,進而推動了對長期營養支持的需求。醫療機構擴大選擇經腸營養經腸營養而非其他營養方式,因為腸內營養具有成本效益高、併發症風險低、且能改善患者復健效果等優點。這種持續的轉變直接推動了對蛋白質、碳水化合物、脂類、維生素和礦物質等關鍵營養素的需求。人口結構變化也發揮重要作用,全球老年人口的不斷成長需要專業的營養管理。醫療機構和養老院老年護理服務的擴展促使生產商開發易於消化且營養最佳化的成分。同時,成分加工和配方技術的持續創新正在提高產品的功效、耐受性和臨床適用性,從而進一步促進市場成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 43.1億美元 |

| 預測金額 | 85.8億美元 |

| 複合年成長率 | 7.3% |

預計到2025年,碳水化合物原料市場規模將達到13.6億美元,並在2026年至2035年間以6.7%的複合年成長率成長。各類原料的整體成長受到配方要求日益複雜和臨床營養標準不斷演進的推動。蛋白質擴大被用於支持肌肉的維持和恢復,而碳水化合物原料則不斷精煉,以提供持續的能量供應並改善代謝反應。脂質和脂肪擴大被製成特殊結構,以提高吸收率和消化率。原料功能的擴展正在拓寬其應用範圍,從標準營養製劑到針對特定疾病的營養製劑。

2025年,重症監護/ 加護病房(ICU)領域的市場規模將達到15.6億美元,市佔率為36.3%。預計到2035年,年複合成長率(CAGR)將達到6.6%。臨床營養管理實踐的改變導致急性護理環境中經腸營養的早期啟動,從而增加了對支持代謝穩定和器官功能的成分的需求。此外,營養支持越來越融入疾病管理流程,導致配方更加複雜,成分用量也隨之增加。

預計到2025年,北美經腸營養原料市場規模將達到17.9億美元,並在整個預測期內保持強勁成長。該地區受益於先進的醫療保健基礎設施、完善的報銷系統以及醫院和居家醫療機構中臨床營養的廣泛應用。美國由於人口老化和長期健康問題高發,在該市場中扮演核心角色,臨床指南也日益強調使用特定蛋白質、脂質、纖維和微量營養素進行有針對性的營養干預的重要性。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依原料類型分類,2022-2035年

- 蛋白質原料

- 總蛋白

- 水解蛋白質/胜肽

- 遊離胺基酸

- 功能性胺基酸

- 碳水化合物原料

- 麥芽糊精

- 玉米糖漿固態/葡萄糖

- 複合碳水化合物

- 單醣

- 脂類/脂肪原料

- 長鏈三酸甘油酯(LCTs)

- 中鏈三酸甘油酯(MCT)

- Omega-3脂肪酸

- 單元不飽和脂肪酸(MUFA)

- 結構化脂質和混合乳化劑

- 膳食纖維成分

- 水溶性膳食纖維

- 不溶性膳食纖維

- 抗澱粉

- 益生元纖維

- 微量營養素來源

- 維他命

- 礦物

- 電解質

- 微量元素

- 功能性和增強免疫力的成分

- 核苷酸

- 益生菌

- 抗氧化劑

- 生物活性胜肽

- 其他

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 重症監護/加護病房(ICU)

- 腫瘤學/癌症

- 消化系統疾病

- 神經系統疾病

- 代謝性疾病

- 其他

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第8章:公司簡介

- Abbott

- Nutricia(Danone)

- Nestle Health Science

- Fresenius Kabi

- Otsuka Pharmaceutical

- RAUMEDIC AG

- EA Pharma

- Meiji

- Arla Foods Ingredients

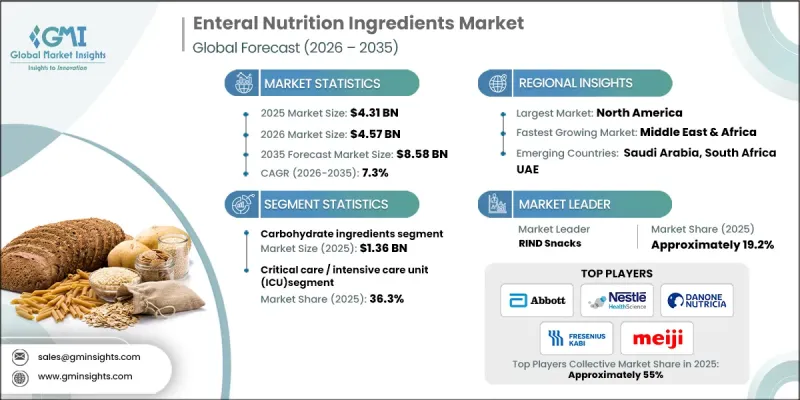

The Global Enteral Nutrition Ingredients Market was valued at USD 4.31 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 8.58 billion by 2035.

Market expansion is supported by the rising demand for long-term nutritional support driven by the growing burden of chronic health conditions and the expanding need for clinical nutrition solutions. Healthcare providers are increasingly favoring enteral nutrition over alternative feeding approaches due to its cost efficiency, lower complication risks, and improved patient recovery outcomes. This sustained shift is directly driving demand for core nutritional ingredients, including proteins, carbohydrates, lipids, vitamins, and minerals. Demographic changes also play a critical role, as the global elderly population continues to grow and requires specialized nutritional management. Expanding geriatric care services across medical and assisted-care facilities is encouraging manufacturers to develop ingredients that are easier to digest and nutritionally optimized. In parallel, continuous innovation in ingredient processing and formulation technologies is enhancing product effectiveness, tolerance, and clinical applicability, further supporting market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.31 Billion |

| Forecast Value | $8.58 Billion |

| CAGR | 7.3% |

The carbohydrate ingredient segment accounted for USD 1.36 billion in 2025 and is projected to register a CAGR of 6.7% from 2026 to 2035. Growth across ingredient types is being shaped by more advanced formulation requirements and evolving clinical nutrition standards. Proteins are increasingly incorporated to support muscle preservation and recovery, while carbohydrate ingredients are being refined to deliver sustained energy and improved metabolic response. Lipids and fats are increasingly formulated into specialized structures to improve absorption and digestive tolerance. This broadening of ingredient functionality is expanding their application across both standard and condition-focused nutritional formulations.

The critical care and intensive care unit application segment generated USD 1.56 billion in 2025 and held a 36.3% share, with a CAGR of 6.6% through 2035. Shifts in clinical nutrition practices are driving earlier initiation of enteral feeding in acute care environments, increasing demand for ingredients that support metabolic stability and organ function. Nutritional support is also becoming increasingly integrated into disease management pathways, raising formulation complexity and ingredient utilization.

North America Enteral Nutrition Ingredients Market accounted for USD 1.79 billion in 2025 and is expected to maintain strong growth throughout the forecast period. The region benefits from advanced healthcare infrastructure, consistent reimbursement frameworks, and widespread adoption of clinical nutrition in hospital and home-care settings. The United States plays a central role due to its aging population and high incidence of long-term health conditions, with clinical guidelines increasingly emphasizing targeted nutrition interventions using specialized proteins, lipids, fibers, and micronutrients.

Key participants in the Global Enteral Nutrition Ingredients Market include Fresenius Kabi, Abbott, Meiji, Nutricia (Danone), Nestle Health Science, and other established suppliers. Companies operating in the enteral nutrition ingredients market are strengthening their competitive position through continuous product innovation and targeted ingredient development. Many players are investing in research to enhance the bioavailability, digestibility, and clinical efficacy of core ingredients. Strategic collaborations with healthcare providers and expansion of production capabilities are helping companies meet rising demand across hospital and home-care settings. Firms are also focusing on disease-specific formulations to align with evolving clinical protocols.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Ingredient Type

- 2.2.3 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Ingredient Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Protein Ingredients

- 5.2.1 Whole Proteins

- 5.2.2 Hydrolyzed Proteins/Peptides

- 5.2.3 Free Amino Acids

- 5.2.4 Functional Amino Acids

- 5.3 Carbohydrate Ingredients

- 5.3.1 Maltodextrins

- 5.3.2 Corn Syrup Solids / Glucose

- 5.3.3 Complex Carbohydrates

- 5.3.4 Simple Sugars

- 5.4 Fat / Lipid Ingredients

- 5.4.1 Long-Chain Triglycerides (LCTs)

- 5.4.2 Medium-Chain Triglycerides (MCTs)

- 5.4.3 Omega-3 Fatty Acids

- 5.4.4 Monounsaturated Fatty Acids (MUFA)

- 5.4.5 Structured Lipids & Blended Emulsions

- 5.5 Fiber Ingredients

- 5.5.1 Soluble Fibers

- 5.5.2 Insoluble Fibers

- 5.5.3 Resistant Starch

- 5.5.4 Prebiotic Fibers

- 5.6 Micronutrient Ingredients

- 5.6.1 Vitamins

- 5.6.2 Minerals

- 5.6.3 Electrolytes

- 5.6.4 Trace Elements

- 5.7 Functional & Immunonutrition Ingredients

- 5.7.1 Nucleotides

- 5.7.2 Probiotics

- 5.7.3 Antioxidants

- 5.7.4 Bioactive Peptides

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Critical care / intensive care unit (ICU)

- 6.3 Oncology / cancer

- 6.4 Gastrointestinal diseases

- 6.5 Neurological disorders

- 6.6 Metabolic disorders

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East & Africa

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Nutricia (Danone)

- 8.3 Nestle Health Science

- 8.4 Fresenius Kabi

- 8.5 Otsuka Pharmaceutical

- 8.6 RAUMEDIC AG

- 8.7 EA Pharma

- 8.8 Meiji

- 8.9 Arla Foods Ingredients

經腸營養市場規模、佔有率和成長分析:按產品類型、年齡層、給藥途徑、應用、護理環境、分銷管道和地區分類-2026-2033年產業預測

經腸營養市場規模、佔有率和成長分析:按產品類型、年齡層、給藥途徑、應用、護理環境、分銷管道和地區分類-2026-2033年產業預測 經腸營養市場:按產品類型、營養類型、配方、患者類型、應用、分銷管道、最終用戶和地區分類

經腸營養市場:按產品類型、營養類型、配方、患者類型、應用、分銷管道、最終用戶和地區分類 經腸營養市場:依產品類型、劑型、年齡層及最終用戶分類-2026-2032年全球預測

經腸營養市場:依產品類型、劑型、年齡層及最終用戶分類-2026-2032年全球預測 全球經腸營養市場規模、佔有率、趨勢和成長分析報告(2026-2034年)管飼配方奶粉市場按產品類型、營養類型、年齡層、適應症、最終用戶和分銷管道分類,全球預測,2026-2032年經腸營養市場:2026-2032年全球預測(依產品類型、年齡層、給藥途徑、劑型、用途及最終用戶分類)經腸營養市場:依產品類型、配方類型、給藥途徑、疾病指標、年齡層及通路分類,全球預測,2026-2032年

全球經腸營養市場規模、佔有率、趨勢和成長分析報告(2026-2034年)管飼配方奶粉市場按產品類型、營養類型、年齡層、適應症、最終用戶和分銷管道分類,全球預測,2026-2032年經腸營養市場:2026-2032年全球預測(依產品類型、年齡層、給藥途徑、劑型、用途及最終用戶分類)經腸營養市場:依產品類型、配方類型、給藥途徑、疾病指標、年齡層及通路分類,全球預測,2026-2032年 腸內營養市場規模及預測 2021 - 2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:依產品類型、應用、年齡層、配銷通路及地理分類

腸內營養市場規模及預測 2021 - 2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:依產品類型、應用、年齡層、配銷通路及地理分類 歐洲腸內營養市場規模及預測 2021-2031、區域佔有率、趨勢及成長機會分析報告範圍:依產品類型(鼻胃管、鼻腸管、吸飲管及其他)及國家/地區

歐洲腸內營養市場規模及預測 2021-2031、區域佔有率、趨勢及成長機會分析報告範圍:依產品類型(鼻胃管、鼻腸管、吸飲管及其他)及國家/地區 腸內營養市場,按產品類型、按應用、按配銷通路、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

腸內營養市場,按產品類型、按應用、按配銷通路、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測