|

市場調查報告書

商品編碼

1959319

雲端合規市場機會、成長要素、產業趨勢分析及2026年至2035年預測Cloud Compliance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

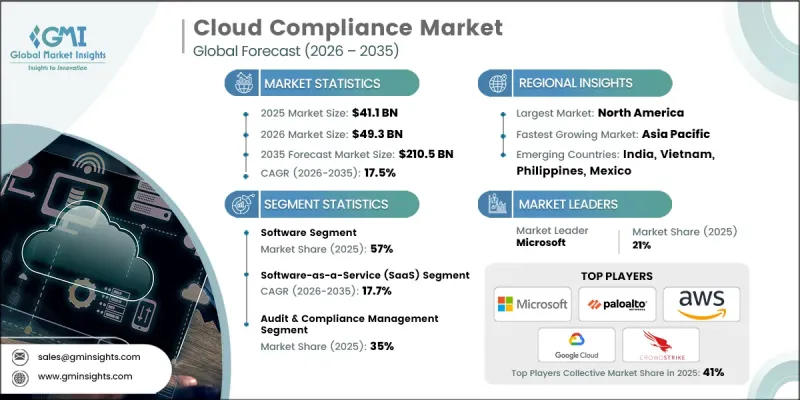

2025 年全球雲端合規市場價值為 411 億美元,預計到 2035 年將達到 2,105 億美元,年複合成長率為 17.5%。

隨著企業加速向公有雲、私有雲和混合雲端環境遷移,工作負載、身分、配置和資料資產等方面的合規複雜性急劇增加。隨著企業將應用程式分佈在多個雲端基礎架構上,維護一致的管治和策略執行變得更加具有挑戰性。對不同雲端服務供應商和私人基礎設施的依賴性日益增強,容易導致可見性分散,從而對集中式合規編配和自動化監控平台產生了強烈的需求。企業正在優先採用持續監控框架,以大規模地滿足內部管治標準和不斷變化的監管要求。通訊業正在加速採用整合安全態勢管理和應用程式保護功能的統一安全合規架構。此外,不斷擴展的資料保護條例和特定產業義務增加了合規風險,因此需要投資於自動化證據收集和報告系統。即時合規追蹤正在逐步取代傳統的定期審核,推動了基於 SaaS 的合規解決方案的普及,這些解決方案提供敏捷性、擴充性和主動風險緩解功能。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 411億美元 |

| 預測金額 | 2105億美元 |

| 複合年成長率 | 17.5% |

預計到2025年,軟體領域將佔據57%的市場佔有率,並在2026年至2035年間以16.6%的複合年成長率成長。合規平台正從獨立的姿態管理工具演變為整合身分管治、工作負載保護、組態管理和資料安全控制的生態系統。這種轉變正在推動企業內部工具的整合,以期提高跨雲端可見度和營運效率。軟體供應商正在將合規性檢驗功能直接整合到開發平臺和基礎設施自動化工作流程中,從而在配置生命週期的早期階段檢測違規行為。將合規性檢查整合到DevOps和平台工程流程中,能夠幫助企業降低補救成本、加速雲端部署,並增強整個技術團隊的課責。這些進展進一步強化了軟體主導的合規框架在複雜的多重雲端環境中的優勢。

軟體即服務(SaaS) 預計到 2025 年將佔據 52% 的市場佔有率,並在 2026 年至 2035 年期間以 17.7% 的複合年成長率成長。基於 SaaS 的合規解決方案能夠持續監控外部託管應用程式的資料存取控制、使用者行為和設定一致性。隨著企業快速採用雲端原生平台,維護第三方系統的可見性和管治變得日益重要。 SaaS 合規工具提供集中式管理儀表板、自動化報告功能和可用於審核的文檔,協助組織保護敏感資料、執行身分管理標準並維持合規性。 SaaS 交付模式的柔軟性和擴充性持續推動著各種規模的企業採用此模式。

預計2025年,美國雲端合規市場規模將達141億美元。美國企業正在將多種安全和合規解決方案整合到整合的雲端原生保護平台中,以簡化監管合規流程並降低營運複雜性。這種整合減少了工具重複,增強了審核應對力,並實現了對混合雲和多重雲端工作負載的持續監控。人工智慧 (AI) 驅動的風險優先排序技術正在被廣泛採用,使企業能夠識別高影響力的合規問題,並自動執行跨職能、協調一致的糾正工作流程。 AI 驅動的分析技術透過最大限度地減少誤報並促進 IT 營運團隊和安全團隊之間的更緊密協作,提高了營運效率。這些發展正在使美國成為先進雲端合規創新領域的領先中心。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 加速雲端遷移

- 多重雲端和混合環境的複雜性

- 日益成長的資料隱私和安全義務

- 向持續合規自動化過渡

- 產業潛在風險與挑戰

- 高昂的實施和整合成本

- 熟練的雲端合規專家短缺

- 市場機遇

- 中小企業的合規自動化

- 託管雲端合規服務

- 與 DevSecOps 和 CI/CD 流水線整合

- 公共部門和政府機構的雲端採用情況

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國國家標準與技術研究院(NIST)

- 聯邦風險授權管理計劃 (FedRAMP)

- 歐洲

- 歐洲資料保護委員會(EDPB)

- 歐洲網路安全局 (ENISA)

- 亞太地區

- 新加坡個人資料保護委員會(PDPC)

- 資訊科技促進機構(IPA)

- 拉丁美洲

- 巴西國家資料保護局(ANPD)

- 墨西哥國家資訊自由與個人資料保護委員會(INAI)

- 中東和非洲

- 阿拉伯聯合大公國資料管理局/人工智慧部/聯邦身分和公民權辦公室

- 南非資訊監理局(SAIR)

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 用例

- 投資與資金籌措分析

- 風險與網路安全暴露分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依組件分類,2022-2035年

- 軟體

- 服務

第6章 市場估算與預測:依部署模式分類,2022-2035年

- 軟體即服務(SaaS)

- 基礎設施即服務 (IaaS)

- 平台即服務 (PaaS)

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 審核和合規管理

- 威脅偵測與補救

- 活動監測與分析

- 可見性和風險評估

- 其他

第8章 市場估計與預測:依公司規模分類,2022-2035年

- 主要企業

- 中小企業

第9章 市場估計與預測:依最終用途分類,2022-2035年

- BFSI

- 資訊科技/通訊

- 衛生保健

- 政府/公共部門

- 零售和消費品

- 製造業

- 能源與公共產業

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 菲律賓

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- Amazon Web Services(AWS)

- Check Point Software Technologies

- CrowdStrike

- Fortinet

- Google Cloud(Alphabet Inc.)

- IBM

- Microsoft

- Palo Alto Networks

- Qualys

- Trend Micro

- 本地球員

- Aqua Security

- Lacework(Fortinet)

- Orca Security

- Rapid7

- SentinelOne

- Snyk

- Sysdig

- Tenable

- Wiz

- Zscaler

- 新興企業

- Horangi Cyber Security

- Scrut Automation

- Secureframe

- Vanta

The Global Cloud Compliance Market was valued at USD 41.1 billion in 2025 and is estimated to grow at a CAGR of 17.5% to reach USD 210.5 billion by 2035.

Accelerated enterprise migration toward public, private, and hybrid cloud environments is significantly increasing compliance complexity across workloads, identities, configurations, and data assets. As organizations distribute applications across multiple cloud infrastructures, maintaining consistent governance and policy enforcement has become more challenging. The growing reliance on diverse cloud service providers alongside private infrastructure often results in fragmented visibility, creating a strong demand for centralized compliance orchestration and automated oversight platforms. Enterprises are prioritizing continuous monitoring frameworks to satisfy both internal governance standards and evolving regulatory requirements at scale. Industries such as financial services and telecommunications are increasingly deploying unified security and compliance architectures that consolidate posture management and application protection capabilities. Additionally, expanding data protection regulations and sector-specific mandates are intensifying compliance exposure, compelling businesses to invest in automated evidence collection and reporting systems. Real-time compliance tracking is gradually replacing traditional periodic audits, driving widespread adoption of SaaS-based compliance solutions that offer agility, scalability, and proactive risk mitigation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $41.1 Billion |

| Forecast Value | $210.5 Billion |

| CAGR | 17.5% |

The software segment accounted for 57% share in 2025 and is anticipated to grow at a CAGR of 16.6% from 2026 to 2035. Compliance platforms are evolving from standalone posture management tools into integrated ecosystems that unify identity governance, workload protection, configuration management, and data security controls. This transition is encouraging tool consolidation within enterprises seeking improved cross-cloud visibility and operational efficiency. Software providers are embedding compliance validation directly into development pipelines and infrastructure automation workflows to detect violations earlier in the deployment lifecycle. By incorporating compliance checks within DevOps and platform engineering processes, organizations can reduce remediation expenses, accelerate cloud rollouts, and strengthen accountability across technical teams. These advancements are reinforcing the dominance of software-driven compliance frameworks in complex multi-cloud environments.

The Software-as-a-Service segment held a 52% share in 2025 and is forecast to grow at a CAGR of 17.7% between 2026 and 2035. SaaS-based compliance solutions deliver continuous monitoring of data access controls, user behavior, and configuration integrity across externally hosted applications. As enterprises rapidly deploy cloud-native platforms, maintaining visibility and governance across third-party systems becomes increasingly critical. SaaS compliance tools provide centralized dashboards, automated reporting capabilities, and audit-ready documentation that help organizations safeguard sensitive data, enforce identity management standards, and maintain regulatory readiness. The flexibility and scalability of SaaS delivery models continue to drive adoption across enterprises of all sizes.

United States Cloud Compliance Market reached USD 14.1 billion in 2025. Across the country, enterprises are consolidating multiple security and compliance solutions into unified cloud-native protection platforms to streamline regulatory adherence and reduce operational complexity. This consolidation reduces redundant tooling, enhances audit preparedness, and enables continuous oversight of hybrid and multi-cloud workloads. Adoption of artificial intelligence-driven risk prioritization is expanding, allowing organizations to identify high-impact compliance gaps and automate coordinated remediation workflows across departments. AI-powered analytics are improving operational efficiency by minimizing false alerts and fostering closer collaboration between IT operations and security teams. These developments are positioning the United States as a leading hub for advanced cloud compliance innovation.

Major companies operating in the Global Cloud Compliance Market include Palo Alto Networks, Microsoft, Google Cloud, Amazon Web Services (AWS), Check Point Software, CrowdStrike, Fortinet, Trend Micro, Qualys, and Wiz. These providers compete by delivering integrated compliance, security, and risk management platforms designed to address evolving regulatory landscapes and multi-cloud operational demands. Companies in the Global Cloud Compliance Market are reinforcing their competitive standing through platform consolidation, AI-driven automation, and expanded multi-cloud interoperability. Vendors are investing in advanced analytics and machine learning models to deliver predictive compliance insights and automated remediation capabilities. Strategic partnerships with cloud providers and enterprise clients enable deeper integration across hybrid infrastructures. Many firms are enhancing developer-focused tools that embed compliance validation within CI/CD pipelines to promote proactive governance. In addition, providers are expanding global data center footprints and compliance certifications to meet regional regulatory standards.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment model

- 2.2.4 Application

- 2.2.5 Enterprise size

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerated cloud migration

- 3.2.1.2 Multi-cloud and hybrid complexity

- 3.2.1.3 Rising data privacy and security obligations

- 3.2.1.4 Shift to continuous compliance automation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Shortage of skilled cloud compliance professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Compliance automation for SMBs

- 3.2.3.2 Managed cloud compliance services

- 3.2.3.3 Integration with DevSecOps and CI/CD pipelines

- 3.2.3.4 Public sector and government cloud adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Institute of Standards and Technology (NIST)

- 3.4.1.2 Federal Risk and Authorization Management Program (FedRAMP)

- 3.4.2 Europe

- 3.4.2.1 European Data Protection Board (EDPB)

- 3.4.2.2 ENISA (European Union Agency for Cybersecurity)

- 3.4.3 Asia Pacific

- 3.4.3.1 Singapore Personal Data Protection Commission (PDPC)

- 3.4.3.2 Japan Information-technology Promotion Agency (IPA)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Data Protection Authority (ANPD)

- 3.4.4.2 Mexico National Institute for Transparency, Access to Information and Personal Data Protection (INAI)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Data Office / Ministry of Artificial Intelligence & Federal Authority for Identity and Citizenship

- 3.4.5.2 South Africa Information Regulator (SAIR)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Investment & funding analysis

- 3.13 Risk & cybersecurity exposure analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Deployment model, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Software-as-a-Service (SaaS)

- 6.3 Infrastructure-as-a-Service (IaaS)

- 6.4 Platform-as-a-Service (PaaS)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Audit & compliance management

- 7.3 Threat detection & remediation

- 7.4 Activity monitoring & analytics

- 7.5 Visibility & risk assessment

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Enterprise size, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Large enterprises

- 8.3 Small & medium enterprises (SMEs)

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT & telecommunications

- 9.4 Healthcare

- 9.5 Government & public sector

- 9.6 Retail & consumer goods

- 9.7 Manufacturing

- 9.8 Energy & utilities

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Philippines

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Amazon Web Services (AWS)

- 11.1.2 Check Point Software Technologies

- 11.1.3 CrowdStrike

- 11.1.4 Fortinet

- 11.1.5 Google Cloud (Alphabet Inc.)

- 11.1.6 IBM

- 11.1.7 Microsoft

- 11.1.8 Palo Alto Networks

- 11.1.9 Qualys

- 11.1.10 Trend Micro

- 11.2 Regional players

- 11.2.1 Aqua Security

- 11.2.2 Lacework (Fortinet)

- 11.2.3 Orca Security

- 11.2.4 Rapid7

- 11.2.5 SentinelOne

- 11.2.6 Snyk

- 11.2.7 Sysdig

- 11.2.8 Tenable

- 11.2.9 Wiz

- 11.2.10 Zscaler

- 11.3 Emerging players

- 11.3.1 Horangi Cyber Security

- 11.3.2 Scrut Automation

- 11.3.3 Secureframe

- 11.3.4 Vanta