|

市場調查報告書

商品編碼

1959318

2026 年至 2035 年航太高性能熱塑性塑膠市場的市場機會、成長要素、產業趨勢分析與預測。High-Performance Thermoplastics in Aerospace Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

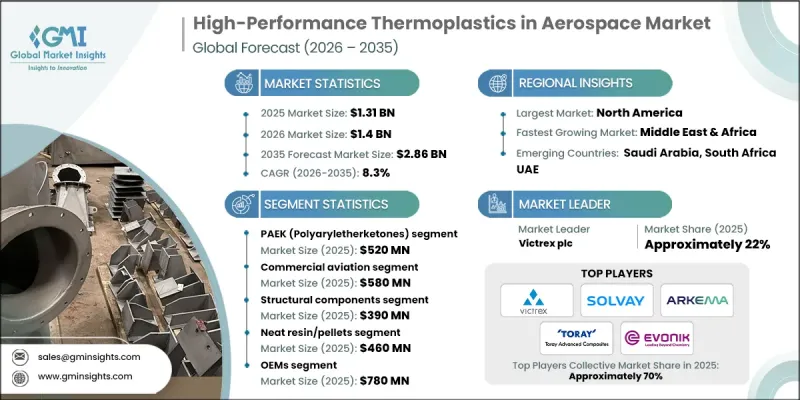

2025 年全球航太領域高性能熱塑性塑膠市場價值為 13.1 億美元,預計到 2035 年將達到 28.6 億美元,年複合成長率為 8.3%。

航太業對輕質高強度材料的需求不斷成長,推動了市場成長。這些材料有助於提高燃油效率並降低營運成本。航太製造商正推動從傳統金屬和熱固性樹脂轉向高性能熱塑性塑膠。這些聚合物具有卓越的熱穩定性、機械強度和耐腐蝕性,同時也能減輕飛機的整體重量。先進聚合物科學的進步提高了這些材料的耐久性和性能,使其適用於關鍵結構部件。此外,人們對永續性關注以及更嚴格的排放法規,也推動了對環境影響較小的可再生熱塑性塑膠的採用。這些材料能夠承受極端溫度和惡劣的化學環境,從而延長民用航空、國防和公務航空領域的使用壽命,減少維護週期,並提高可靠性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 13.1億美元 |

| 預測金額 | 28.6億美元 |

| 複合年成長率 | 8.3% |

預計到2025年,聚芳醚酮(PAEK)市場規模將達到5.2億美元,並在2026年至2035年間以7.8%的複合年成長率成長。 PAEK材料因其優異的耐熱性和嚴苛的機械性能,在航太領域日益受到青睞。其耐化學性和耐熱性使其成為結構件和半結構件的理想選擇。同樣,聚醯亞胺也因其出色的尺寸穩定性和耐熱性而備受關注,尤其是在引擎周圍和其他高溫區域等極端溫度環境下。這些材料的獨特性能使航太工程師能夠設計出更輕、更有效率且能承受嚴苛運作條件的飛機。

預計到2025年,民用航空市場規模將達到5.8億美元,並在2026年至2035年間以7.9%的複合年成長率成長。飛機製造量的增加、機身現代化改造以及對效率提升的追求,推動了對用於機身結構、內飾和機載系統的高性能熱塑性塑膠的需求。軍用和國防航空領域也為市場成長做出了貢獻,需要能夠承受嚴苛運作環境並具有長使用壽命的材料。在公務航空和通用航空領域,先進熱塑性塑膠的應用日益廣泛,旨在應對傳統航太材料的複雜性和成本挑戰,從而提升性能並簡化製造流程。

預計到2025年,北美航太高性能熱塑性塑膠市場規模將達到4.9億美元。該地區市場擴張的驅動力包括先進的飛機製造技術、研發帶來的持續材料創新以及自動化製造技術的早期應用。北美受益於成熟的航太供應鏈和對下一代飛機項目的持續投資。美國正透過增加民航機交付、推進軍事現代化項目以及將輕質高性能熱塑性塑膠整合到結構和系統部件中,推動區域市場成長。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依材料類型分類,2022-2035年

- PAEK(聚芳醚酮)

- PEEK(聚醚醚酮)

- PEKK(聚醚酮酮)

- LM-PAEK(低熔點PAEK)

- 聚醯亞胺

- PEI(聚醚醯亞胺/Artem)

- PAI(聚醯胺-醯亞胺)

- 聚碸

- 聚亞苯硫醚(PPS)

- 其他高性能熱塑性樹脂

第6章 市場估算與預測:依飛機平台分類,2022-2035年

- 商業航空

- 窄體飛機

- 寬體飛機

- 軍事/國防航空

- 戰鬥機

- 軍用運輸機

- 軍用直升機

- 商務及通用航空

- 空間應用

- 其他

第7章 市場估計與預測:依組件類型分類,2022-2035年

- 結構部件

- 主體結構

- 二級結構

- 內部零件

- 座椅和座椅框架

- 廚房和衛生間

- 頭頂置物箱

- 側牆和天花板麵板

- 窗框和裝飾條

- 引擎和推進系統部件

- 引擎室和引擎罩

- 反推裝置

- 管道和空氣管理系統

- 風扇葉片和隔音襯裡

- 電氣和電子設備機殼

- 雷達罩和天線外殼

- 航空電子設備機殼

- 線纜管理系統

- 電磁干擾/射頻干擾屏蔽要求

- 透明部件和窗戶

- 飛機舷窗和擋風玻璃

- (軍用)座艙罩

- 聚碳酸酯和丙烯酸樹脂的比較分析

- 前緣和氣動表面

- 主翼前緣

- 控制面

- 空氣力學整流罩

第8章 市場估算與預測:依產品類型分類,2022-2035年

- 純樹脂/顆粒

- 預孕

- 單向(UD)膠帶

- 紡織預浸料

- 半成品

- 板材和層壓板

- 薄膜和膜

- 型材和擠壓產品

- 成品零件/組件

第9章 市場估價與預測:依製造流程分類,2022-2035年

- 自動光纖鋪放(AFP)和自動膠帶鋪放(ATP)

- 壓縮成型和壓製成型

- 熱成型

- 射出成型

- 積層製造(AM)

- 焊接和連接技術

- 電阻焊接

- 感應焊接

- 超音波焊接

- 雷射焊接

- 連續壓縮成型(CCM)

第10章 市場估價與預測:依最終用戶分類,2022-2035年

- OEM(原始設備製造商)

- MRO(維修、修理和大修)服務供應商

- 研究機構和學術機構

- 其他

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第12章:公司簡介

- Victrex plc

- Solvay Special Chemicals

- Arkema SA

- Evonik Industries AG

- SABIC

- BASF SE

- Envalior

- Toray Advanced Composites

- Teijin Limited

- Celanese Corporation

- Mitsubishi Chemical Group

- Rochling Group

- Syensqo

- Ensinger GmbH

The Global High-Performance Thermoplastics in Aerospace Market was valued at USD 1.31 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 2.86 billion by 2035.

Market growth is driven by the aerospace industry's increasing need for lightweight, high-strength materials that can improve fuel efficiency and reduce operational costs. Aerospace manufacturers are progressively replacing traditional metals and thermosets with high-performance thermoplastics, as these polymers offer superior thermal stability, mechanical strength, and corrosion resistance while reducing overall aircraft weight. The development of advanced polymer science has enhanced the durability and performance of these materials, making them suitable for critical structural components. Sustainability concerns and stricter emissions regulations are also pushing the adoption of recyclable thermoplastics with lower environmental impact. Their ability to endure extreme temperatures and harsh chemical environments ensures longer service life, fewer maintenance cycles, and increased reliability across commercial, defense, and business aviation applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.31 Billion |

| Forecast Value | $2.86 Billion |

| CAGR | 8.3% |

The PAEK (Polyaryletherketones) segment generated USD 0.52 billion in 2025 and is estimated to grow at a CAGR of 7.8% between 2026 and 2035. PAEK materials are increasingly preferred for aerospace applications requiring high thermal tolerance and demanding mechanical performance. Their chemical and thermal resilience make them ideal for structural and semi-structural components. Similarly, polyimides are gaining traction in regions exposed to extreme heat, such as areas near engines or other high-temperature zones, due to their exceptional dimensional stability and heat resistance. The unique properties of these materials enable aerospace engineers to design lighter and more efficient aircraft capable of withstanding rigorous operating conditions.

The commercial aviation segment reached USD 0.58 billion in 2025 and is expected to grow at a CAGR of 7.9% from 2026 to 2035. The rise in aircraft manufacturing, fleet modernization, and the push for improved efficiency are driving demand for high-performance thermoplastics in airframes, interiors, and onboard systems. Military and defense aviation is also contributing to growth, as these sectors demand materials capable of enduring harsh operational conditions while offering long service life. Business and general aviation platforms are increasingly utilizing advanced thermoplastics to enhance performance and simplify manufacturing processes, addressing the complexity and cost of traditional aerospace materials.

North America High-Performance Thermoplastics in Aerospace Market accounted for USD 0.49 billion in 2025. Market expansion in the region is fueled by advanced aircraft production, continuous material innovation through research and development, and early adoption of automated manufacturing technologies. North America benefits from a well-established aerospace supply chain and ongoing investment in next-generation aircraft programs. The U.S. is leading regional growth due to rising commercial aircraft deliveries, military modernization programs, and the integration of lightweight, high-performance thermoplastics in both structural and system components.

Key players operating in the Global High-Performance Thermoplastics in Aerospace Market include Solvay Special Chemicals, Victrex plc, Toray Advanced Composites, Evonik Industries AG, Arkema S.A., and several others. Companies in the high-performance thermoplastics in the aerospace market are focusing on strategic growth initiatives to strengthen their market foothold. They are investing heavily in research and development to create advanced thermoplastic materials with higher thermal tolerance, mechanical strength, and chemical resistance to meet evolving aerospace demands. Expanding production capabilities and forming partnerships with aerospace OEMs allow companies to integrate their solutions into cutting-edge aircraft designs. Firms are also emphasizing sustainability by developing recyclable materials with lower environmental impact, improving lifecycle performance, and reducing maintenance needs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Aircraft Platform

- 2.2.4 Component Type

- 2.2.5 Product Type

- 2.2.6 Manufacturing Process

- 2.2.7 End-User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 PAEK (Polyaryletherketones)

- 5.2.1 PEEK (Polyetheretherketone)

- 5.2.2 PEKK (Polyetherketoneketone)

- 5.2.3 LM-PAEK (Low-Melt PAEK)

- 5.3 Polyimides

- 5.3.1 PEI (Polyetherimide/Ultem)

- 5.3.2 PAI (Polyamideimide)

- 5.4 Polysulfones

- 5.5 PPS (Polyphenylene Sulfide)

- 5.6 Other High-Performance Thermoplastics

Chapter 6 Market Estimates and Forecast, By Aircraft Platform, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Commercial Aviation

- 6.2.1 Narrow-Body Aircraft

- 6.2.2 Wide-Body Aircraft

- 6.3 Military & Defense Aviation

- 6.3.1 Fighter Aircraft

- 6.3.2 Military Transport Aircraft

- 6.3.3 Military Helicopters

- 6.4 Business & General Aviation

- 6.5 Space Applications

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Structural Components

- 7.2.1 Primary Structures

- 7.2.2 Secondary Structures

- 7.3 Interior Components

- 7.3.1 Seats & Seat Frames

- 7.3.2 Galleys & Lavatories

- 7.3.3 Overhead Stow Bins

- 7.3.4 Sidewall & Ceiling Panels

- 7.3.5 Window Reveals & Trim

- 7.4 Engine & Propulsion Components

- 7.4.1 Nacelles & Engine Cowlings

- 7.4.2 Thrust Reversers

- 7.4.3 Ducts & Air Management Systems

- 7.4.4 Fan Blades & Acoustic Liners

- 7.5 Electrical & Electronic Housings

- 7.5.1 Radomes & Antenna Housings

- 7.5.2 Avionics Enclosures

- 7.5.3 Cable Management Systems

- 7.5.4 EMI/RFI Shielding Requirements

- 7.6 Transparencies & Windows

- 7.6.1 Aircraft Windows & Windshields

- 7.6.2 Canopies (Military Applications)

- 7.6.3 Polycarbonate vs. Acrylic Analysis

- 7.7 Leading Edges & Aerodynamic Surfaces

- 7.7.1 Wing Leading Edges

- 7.7.2 Control Surfaces

- 7.7.3 Aerodynamic Fairings

Chapter 8 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Neat Resin/Pellets

- 8.3 Prepregs

- 8.3.1 Unidirectional (UD) Tape

- 8.3.2 Woven Fabric Prepregs

- 8.4 Semi-Finished Products

- 8.4.1 Sheets & Laminates

- 8.4.2 Films & Membranes

- 8.4.3 Profiles & Extruded Shapes

- 8.5 Finished Parts/Components

Chapter 9 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Automated Fiber Placement (AFP) & Automated Tape Placement (ATP)

- 9.3 Compression Molding & Stamp Forming

- 9.4 Thermoforming

- 9.5 Injection Molding

- 9.6 Additive Manufacturing (AM)

- 9.7 Welding & Joining Technologies

- 9.7.1 Resistance Welding

- 9.7.2 Induction Welding

- 9.7.3 Ultrasonic Welding

- 9.7.4 Laser Welding

- 9.8 Continuous Compression Molding (CCM)

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 OEMs (Original Equipment Manufacturers)

- 10.3 MRO (Maintenance, Repair & Overhaul) Providers

- 10.4 Research Institutions & Academia

- 10.5 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East & Africa

Chapter 12 Company Profiles

- 12.1 Victrex plc

- 12.2 Solvay Special Chemicals

- 12.3 Arkema S.A.

- 12.4 Evonik Industries AG

- 12.5 SABIC

- 12.6 BASF SE

- 12.7 Envalior

- 12.8 Toray Advanced Composites

- 12.9 Teijin Limited

- 12.10 Celanese Corporation

- 12.11 Mitsubishi Chemical Group

- 12.12 Rochling Group

- 12.13 Syensqo

- 12.14 Ensinger GmbH

航太熱塑性塑膠市場-全球產業規模、佔有率、趨勢、機會及預測,依平台類型、應用類型、形態類型、地區及競爭格局分類,2020-2030年預測

航太熱塑性塑膠市場-全球產業規模、佔有率、趨勢、機會及預測,依平台類型、應用類型、形態類型、地區及競爭格局分類,2020-2030年預測 航太用熱塑性塑膠複合材料市場:全球產業分析,規模,佔有率,成長,趨勢,2024~2031年預測

航太用熱塑性塑膠複合材料市場:全球產業分析,規模,佔有率,成長,趨勢,2024~2031年預測