|

市場調查報告書

商品編碼

1959311

汽車電子導電塑膠市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Conductive Plastics for Automotive Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

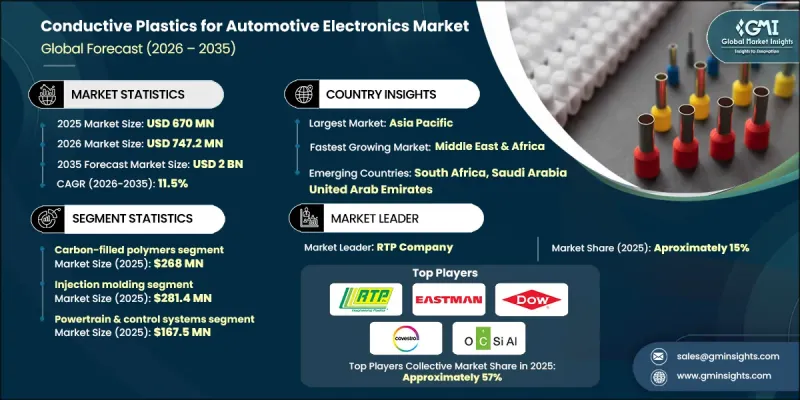

2025 年全球汽車電子導電塑膠市場價值為 6.7 億美元,預計到 2035 年將達到 20 億美元,年複合成長率為 11.5%。

這一成長源於汽車產業對輕量化、高性能材料的日益依賴,以提高能源效率、減輕車身重量並增強設計柔軟性。導電塑膠正擴大取代傳統金屬,應用於電子機殼、連接器和結構件中,在顯著降低成本的同時,還能提供與之相當的性能。這種轉變符合原始設備製造商 (OEM) 的優先事項,例如熱效率、緊湊封裝以及複雜電子架構的無縫整合。隨著汽車平臺變得更加模組化和電氣化,對兼具導電性、耐久性和可製造性的多功能材料的需求持續成長。汽車電子產品(包括高級駕駛輔助系統 (ADAS)、連網解決方案、資訊娛樂系統和電力電子產品)的普及,也增加了對有效電磁和高頻干擾屏蔽的需求。導電塑膠在保護敏感元件和實現緊湊系統設計方面發揮著至關重要的作用,使其成為現代汽車電子產品開發不可或缺的材料。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 6.7億美元 |

| 預測金額 | 20億美元 |

| 複合年成長率 | 11.5% |

預計到2025年,碳填充聚合物市場規模將達到2.68億美元。這類材料因其兼具導電性、成本效益和低密度等優點而被廣泛應用,尤其適用於電磁干擾(EMI)和靜電放電(ESD)屏蔽。其他類型的導電塑膠則滿足不同的性能需求;高導電性材料能夠承受嚴苛的電氣和熱學條件,而軟性導電聚合物在需要耐腐蝕性和可調性的特殊應用中也日益受到重視。

預計到2025年,動力傳動系統和控制系統市場規模將達到1.675億美元,並在2026年至2035年間以12.1%的複合年成長率成長。在這些系統中,在熱應力和機械應力下保持穩定的電氣性能至關重要,這促使導電塑膠在感測器、控制單元和電子模組中的應用日益廣泛。此外,導電塑膠在安全相關電子設備和駕駛輔助系統中的應用也在不斷擴展,因為這些系統需要穩定的訊號傳輸和有效的屏蔽才能確保可靠運作。

預計到2025年,北美汽車電子導電塑膠市場規模將達到1.209億美元,並有望在預測期內持續成長。該地區受益於先進汽車電子產品的普及、成熟的製造基礎設施以及對電動車生產的大力投資。美國憑藉其完善的供應鏈以及對輕質高性能材料的專注,佔據了該地區最大的需求佔有率,這些材料能夠提升電氣安全性和屏蔽性能。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 汽車電子領域輕量化材料的應用日益廣泛

- 電磁干擾/射頻干擾屏蔽元件的需求增加

- 導電添加劑的技術進步

- 產業潛在風險與挑戰

- 有限的熱導率

- 複雜且高成本的製作流程

- 市場機遇

- 電動車和智慧電子設備的應用範圍不斷擴大

- 高性能導電填料的進展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計資料(HS編碼)(註:貿易統計僅提供主要國家的資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估算與預測:導電塑膠依類型分類,2022-2035年

- 碳填充聚合物

- 炭黑

- 奈米碳管(CNTs)

- 石墨烯/石墨

- 金屬填充聚合物

- 鍍銀

- 鎳填充

- 銅填充物

- 混合金屬填料

- 本徵導電聚合物

- 聚苯胺(PANI)

- 聚吡咯(PPy)

- 聚(3,4-硫酚)(PEDOT)

- 導電聚合物複合材料

- 熱塑性複合材料

- 熱固性複合材料

第6章 依製造流程分類的市場估算與預測,2022-2035年

- 射出成型

- 擠出成型(型材、薄膜、片材、電纜)

- 塗層和表面處理

- 積層製造(3D列印)

- 混煉和母粒生產

第7章 市場估算與預測:最終用途分類,2022-2035年

- 動力傳動系統與控制系統

- 引擎控制模組(ECM)

- 電動車電池管理系統(BMS)

- 安全/ADAS

- 安全氣囊感知器

- LiDAR/雷達外殼

- 相機支架和護罩

- 資訊娛樂與車載資訊系統

- 觸控顯示器和邊框

- 天線罩

- 電磁干擾/射頻干擾屏蔽

- 人體電子系統

- 智慧鑰匙收納

- 感測器外殼(接近感測器、雨量感測器、光照感測器)

- 連接模組

- 充電/電源分配

- 電動車充電組件

- 配電單元

- 連接器外殼

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- RTP Company

- Eastman Chemical Company

- SIMONA AG

- Nanocyl SA

- OCSiAl

- DOW

- Covestro AG

- Heraeus Materials Technology

- Agfa-Gevaert NV

The Global Conductive Plastics for Automotive Electronics Market was valued at USD 670 million in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 2 billion by 2035.

Growth is driven by the automotive industry's increasing reliance on lightweight, high-performance materials to improve energy efficiency, reduce vehicle mass, and enable greater design flexibility. Conductive plastics are increasingly replacing conventional metals in electronic housings, connectors, and structural components, offering comparable performance with significantly lower weight. This transition aligns with OEM priorities around thermal efficiency, compact packaging, and seamless integration of complex electronic architectures. As vehicle platforms become more modular and electrified, demand for multifunctional materials that combine conductivity, durability, and manufacturability continues to rise. The rapid increase in onboard electronics, including advanced driver assistance, connectivity solutions, infotainment systems, and power electronics, has heightened the need for effective electromagnetic and radio-frequency interference shielding. Conductive plastics play a critical role in protecting sensitive components while enabling compact system designs, making them essential to modern automotive electronics development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $670 Million |

| Forecast Value | $2 Billion |

| CAGR | 11.5% |

The carbon-filled polymers segment reached USD 268 million in 2025. These materials are widely adopted due to their balanced electrical conductivity, cost efficiency, and low density, making them suitable for EMI and ESD shielding applications. Other conductive plastic types address different performance requirements, with higher conductivity materials supporting demanding electrical and thermal conditions, while flexible conductive polymers are gaining relevance in specialized applications that require corrosion resistance and tunable performance characteristics.

The powertrain and control systems segment accounted for USD 167.5 million in 2025 and is expected to grow at a CAGR of 12.1% during 2026-2035. Conductive plastics are increasingly used in sensors, control units, and electronic modules within these systems, where consistent electrical performance under thermal and mechanical stress is essential. Their adoption is also expanding across safety-related electronics and driver assistance systems, where stable signal transmission and effective shielding are critical for reliable operation.

North America Conductive Plastics for Automotive Electronics Market generated USD 120.9 million in 2025 and is expected to experience sustained growth over the forecast period. The region benefits from advanced automotive electronics adoption, mature manufacturing infrastructure, and strong investment in electric vehicle production. The United States represents the largest share of regional demand due to its well-established supply chain and focus on lightweight, high-performance materials that enhance electrical safety and shielding performance.

Key companies active in the Global Conductive Plastics for Automotive Electronics Market include Covestro AG, RTP Company, DOW, Eastman Chemical Company, Nanocyl SA, OCSiAl, Heraeus Materials Technology, SIMONA AG, and Agfa Gevaert NV. Companies in the conductive plastics for automotive electronics market are strengthening their market position through continuous material innovation and close collaboration with automotive OEMs. Manufacturers are investing in advanced polymer formulations that deliver improved conductivity, thermal stability, and weight reduction. Strategic partnerships with electronics and vehicle platform developers help align materials with next-generation design requirements. Firms are also expanding production capabilities and regional footprints to support growing EV and electronics demand. Emphasis on scalable manufacturing, cost optimization, and compliance with automotive standards enables wider adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Conductive Plastic Type

- 2.2.3 Manufacturing Process

- 2.2.4 End Use Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of lightweight materials in automotive electronics

- 3.2.1.2 Increasing demand for EMI/RFI shielding components

- 3.2.1.3 Technological advancements in conductive additives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited thermal conductivity

- 3.2.2.2 Complex and costly processing

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of EV & smart electronics applications

- 3.2.3.2 Advancements in high-performance conductive fillers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Conductive Plastic Type, 2022 - 2035 (USD million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Carbon-filled polymers

- 5.2.1 Carbon black

- 5.2.2 Carbon nanotubes (CNT)

- 5.2.3 Graphene/graphite

- 5.3 Metal-filled polymers

- 5.3.1 Silver-filled

- 5.3.2 Nickel-filled

- 5.3.3 Copper-filled

- 5.3.4 Hybrid metal fillers

- 5.4 Intrinsic conductive polymers

- 5.4.1 Polyaniline (PANI)

- 5.4.2 Polypyrrole (PPy)

- 5.4.3 Poly(3,4-ethylenedioxythiophene) (PEDOT)

- 5.5 Conductive polymer composites

- 5.5.1 Thermoplastic composites

- 5.5.2 Thermoset composites

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Injection molding

- 6.3 Extrusion (Profile, Film, Sheet, Cable)

- 6.4 Coating & surface treatment

- 6.5 Additive manufacturing (3D Printing)

- 6.6 Compounding & masterbatch production

Chapter 7 Market Estimates and Forecast, By End Use Application, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powertrain & control systems

- 7.2.1 Engine control modules (ECM)

- 7.2.2 Battery management systems (BMS) for EVs

- 7.3 Safety & ADAS

- 7.3.1 Airbag sensors

- 7.3.2 Lidar/radar housings

- 7.3.3 Camera mounts & shielding

- 7.4 Infotainment & telematics

- 7.4.1 Touch displays & bezels

- 7.4.2 Antenna covers

- 7.4.3 EMI/RFI Shields

- 7.5 Body electronics

- 7.5.1 Smart key housings

- 7.5.2 Sensor housings (Proximity, Rain, Light)

- 7.5.3 Connectivity modules

- 7.6 Charging & power distribution

- 7.6.1 Ev charging components

- 7.6.2 Power distribution units

- 7.6.3 Connector housings

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 RTP Company

- 9.2 Eastman Chemical Company

- 9.3 SIMONA AG

- 9.4 Nanocyl SA

- 9.5 OCSiAl

- 9.6 DOW

- 9.7 Covestro AG

- 9.8 Heraeus Materials Technology

- 9.9 Agfa-Gevaert NV

汽車電子市場:2026年至2032年全球市場預測(按類別分類):動力傳動系統電子、車身電子、資訊娛樂和互聯、安全電子、ADAS(高級駕駛輔助系統)和底盤電子

汽車電子市場:2026年至2032年全球市場預測(按類別分類):動力傳動系統電子、車身電子、資訊娛樂和互聯、安全電子、ADAS(高級駕駛輔助系統)和底盤電子 2026年全球汽車電子市場報告2026年全球汽車電氣和電子設備市場報告卡克電子及通訊配件全球市場報告(2026年)

2026年全球汽車電子市場報告2026年全球汽車電氣和電子設備市場報告卡克電子及通訊配件全球市場報告(2026年) 智慧停車電子設備市場預測至2034年—按組件、存取方式、停車類型、技術、最終用戶和地區分類的全球分析

智慧停車電子設備市場預測至2034年—按組件、存取方式、停車類型、技術、最終用戶和地區分類的全球分析 汽車電子市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測汽車電子製造服務市場:按服務類型、車輛類型、技術和應用分類-2026-2032年全球市場預測汽車電子編程系統市場:按車輛類型、技術、工具類型、最終用途、部署模式和應用分類,全球預測,2026-2032年

汽車電子市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測汽車電子製造服務市場:按服務類型、車輛類型、技術和應用分類-2026-2032年全球市場預測汽車電子編程系統市場:按車輛類型、技術、工具類型、最終用途、部署模式和應用分類,全球預測,2026-2032年 全球汽車電子元件市場:按應用、銷售管道、動力方式、車輛類型、類型、國家和地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測2026-2034年全球汽車內裝環境照明系統市場規模、佔有率、趨勢及成長分析報告

全球汽車電子元件市場:按應用、銷售管道、動力方式、車輛類型、類型、國家和地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測2026-2034年全球汽車內裝環境照明系統市場規模、佔有率、趨勢及成長分析報告