|

市場調查報告書

商品編碼

1959306

個人護理生物基界面活性劑市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Bio-based Surfactants for Personal Care Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

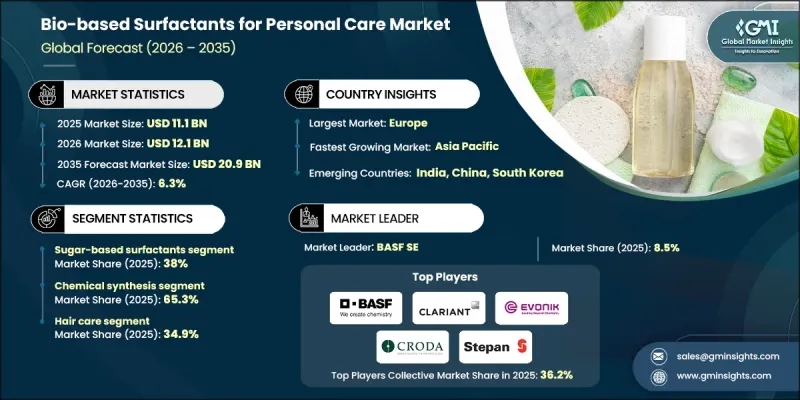

2025 年全球個人護理用生物基界面活性劑市場價值為 111 億美元,預計到 2035 年將達到 209 億美元,年複合成長率為 6.3%。

市場擴張反映了美容和個人護理行業加速向永續和可生物分解原料轉型。用於個人保健產品的生物基界面活性劑涵蓋了廣泛的可再生技術,包括微生物生物界面活性劑、氨基酸基界面活性劑、糖基表面活性劑、生物基乙氧基化物以及其他透過發酵、酵素處理和可再生原料合成等方法開發的植物來源替代品。這些原料在護髮、護膚、口腔護理、嬰兒護理和特色美容產品中的可再生日益廣泛。意識提升對環境永續性和原料透明度的日益關注正在顯著影響他們的購買決策。世界各國政府都在積極推廣綠色化學框架,支持可再生配方創新,並實施鼓勵環保個人照護生產體系轉型的監管政策。目前,歐洲在世界範圍內處於領先地位,這得益於其主要經濟體強力的監管支持和對生產基礎設施的大量投資。同時,亞太地區正在崛起為一個高成長地區,這得益於快速的工業發展、人們對天然美容解決方案日益成長的興趣,以及消費者對潔淨標示和環保型個人保健產品的偏好不斷增強。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 111億美元 |

| 預測金額 | 209億美元 |

| 複合年成長率 | 6.3% |

預計到2025年,糖基界面活性劑的市佔率將達到38%,並在2035年之前以6.7%的複合年成長率成長。其市場佔有率的不斷成長歸功於其溫和的性能、高生物分解性和對敏感肌膚配方的適用性。由於與天然和有機產品相容,這些表面活性劑被廣泛應用於各種個人護理領域。製造商更傾向於使用糖基界面活性劑,因為它們既能提供有效的清潔力,又能滿足清潔美容的標準。對溫和的植物來源成分日益成長的需求,正在加速糖基界面活性劑在新一代化妝品配方中的應用。

預計到2025年,以可再生原料為基礎的化學合成製程將佔65.3%的市場佔有率,並在2035年以6.2%的複合年成長率成長。此生產製程在多種生物基界面活性劑的生產中發揮至關重要的作用,包括胺基酸衍生物、糖基界面活性劑和生物基乙氧基化物。該方法利用可再生原料,並透過成熟的化學技術進行加工,這些技術以其擴充性、營運效率和穩定的產品品質而聞名。與新興的生物技術平台相比,該方法具有更高的商業性可行性和成本優勢,使其在大規模生產中極具吸引力。對可再生原料供應鏈投資的不斷增加以及對可靠的生物基界面活性劑生產日益成長的需求,進一步鞏固了該技術平台的優勢。

預計2026年至2035年,北美個人護理領域生物基界面活性劑市場將以6.7%的複合年成長率成長。這一區域成長主要得益於永續原料開發的創新以及符合綠色化學原則的發酵技術的日益普及。隨著消費者對傳統界面活性劑環境影響的日益關注,各大品牌正在重新設計產品,採用可生物分解的植物來源替代品。不斷壯大的清潔美容運動,以及鼓勵環保生產的法規,進一步刺激了護髮、護膚和專業個人護理領域的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 微生物生物生物界面活性劑

- 醣脂

- 槐醣脂

- 鼠李醣脂

- 赤藻糖醇醇脂質(MEL)

- 海藻醣脂質

- 脂肽

- 表面活性素

- 伊特林

- 理研新

- 醣脂

- 糖基界面活性劑

- 烷基聚葡萄糖苷(APGs)

- 葡糖醯胺

- 蔗糖酯

- 山梨糖醇酯

- 胺基酸衍生的表面活性劑

- 麩胺酸

- 甘胺酸

- 異硫氰酸酯

- 肌氨酸

- 牛

- 生物基乙氧基化物

- 生物基醇醚

- 生物基聚山梨醇酯

- 生物基PEG衍生物

- 生物基蓖麻油乙氧基化物

- 其他

第6章 市場估計與預測:依技術類型分類,2022-2035年

- 微生物發酵技術

- 利用可再生原料進行化學合成

- 酵素合成

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 護髮

- 護膚

- 口腔護理

- 嬰兒護理

- 專業個人護理

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- BASF SE

- Clariant AG

- Evonik Industries AG

- Croda International Plc

- Kao Corporation

- Stepan Company

- Sino Lion

- Galaxy Surfactants Ltd

- Ajinomoto Co., Inc.

- Seppic

- Lonza

- Innospec

- Holiferm Ltd

- Solvay/Syensqo

- Miwon Commercial

The Global Bio-based Surfactants for Personal Care Market was valued at USD 11.1 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 20.9 billion by 2035.

Market expansion reflects the accelerating shift toward sustainable and biodegradable ingredients within the beauty and personal care industry. Bio-based surfactants used in personal care formulations include a broad portfolio of renewable technologies such as microbial-derived biosurfactants, amino acid-based surfactants, sugar-derived surfactants, bio-based ethoxylates, and other plant-origin alternatives developed through fermentation, enzymatic processing, and renewable feedstock synthesis. These ingredients are increasingly incorporated into hair care, skin care, oral hygiene, baby care, and specialty beauty products. Rising consumer awareness of environmental sustainability and ingredient transparency is significantly influencing purchasing decisions. Governments worldwide are promoting green chemistry frameworks, funding innovation in renewable formulations, and introducing regulatory policies that encourage the transition toward eco-conscious personal care manufacturing systems. Europe currently leads the global landscape, supported by strong regulatory backing and substantial investment in production infrastructure across major economies. Meanwhile, Asia Pacific is emerging as a high-growth region, driven by rapid industrial advancement, increased focus on natural beauty solutions, and expanding consumer preference for clean-label and environmentally responsible personal care products.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.1 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 6.3% |

The sugar-based surfactants segment accounted for 38% share in 2025 and is forecast to grow at a CAGR of 6.7% through 2035. Their growing prominence is attributed to their mild performance profile, high biodegradability, and suitability for sensitive skin formulations. These surfactants are widely adopted across diverse personal care categories due to their compatibility with natural and organic product positioning. Manufacturers favor sugar-derived solutions for their ability to deliver effective cleansing while aligning with clean beauty standards. The increasing demand for gentle, plant-based ingredients is accelerating the integration of sugar-based surfactants into next-generation cosmetic formulations.

The chemical synthesis from renewable feedstocks segment held 65.3% share in 2025 and is anticipated to grow at a CAGR of 6.2% by 2035. This production pathway plays a critical role in manufacturing a wide array of bio-based surfactants, including amino acid-derived variants, sugar-based surfactants, and bio-based ethoxylates. The approach leverages renewable raw materials processed through established chemical technologies known for scalability, operational efficiency, and consistent output quality. Compared to emerging biotechnology platforms, this method offers strong commercial viability and cost advantages, making it attractive for large-scale production. Rising investments in renewable feedstock supply chains and growing demand for dependable bio-based surfactant manufacturing are reinforcing the dominance of this technology platform.

North America Bio-based Surfactants for Personal Care Market is expected to register a CAGR of 6.7% between 2026 and 2035. Growth in the region is fueled by innovation in sustainable ingredient development and increased adoption of fermentation-based technologies aligned with green chemistry principles. Consumer concern regarding the ecological footprint of conventional surfactants is prompting brands to reformulate products with biodegradable and plant-derived alternatives. Expanding clean beauty movements, combined with regulatory encouragement for environmentally responsible manufacturing, are further stimulating demand across hair care, skin care, and specialty personal care segments.

Key companies operating in the Global Bio-based Surfactants for Personal Care Market include BASF SE, Croda International Plc, Clariant AG, Evonik Industries AG, Solvay / Syensqo, Galaxy Surfactants Ltd, Kao Corporation, Ajinomoto Co., Inc., Stepan Company, Innospec, Seppic, Lonza, Sino Lion, Miwon Commercial, and Holiferm Ltd. These companies are actively shaping competitive dynamics through innovation, sustainability commitments, and strategic expansion initiatives. Companies in the bio-based surfactants for personal care market are strengthening their market position by investing in advanced research and development focused on high-performance, biodegradable formulations. Strategic collaborations with beauty brands enable the co-creation of customized ingredients tailored to clean-label demands. Many firms are expanding manufacturing capacity for renewable feedstocks while improving supply chain transparency to meet sustainability benchmarks. Portfolio diversification into specialty and premium-grade surfactants supports differentiation in a competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Technology type

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Microbial biosurfactants

- 5.2.1 Glycolipids

- 5.2.1.1 Sophorolipids

- 5.2.1.2 Rhamnolipids

- 5.2.1.3 Mannosylerythritol lipids (MELs)

- 5.2.1.4 Trehalolipids

- 5.2.2 Lipopeptides

- 5.2.2.1 Surfactin

- 5.2.2.2 Iturin

- 5.2.2.3 Lichenysin

- 5.2.1 Glycolipids

- 5.3 Sugar-based surfactants

- 5.3.1 Alkyl polyglucosides (APGs)

- 5.3.2 Glucamides

- 5.3.3 Sucrose esters

- 5.3.4 Sorbitan esters

- 5.4 Amino acid-derived surfactants

- 5.4.1 Glutamates

- 5.4.2 Glycinates

- 5.4.3 Isethionates

- 5.4.4 Sarcosinates

- 5.4.5 Taurates

- 5.5 Bio-based ethoxylates

- 5.5.1 Bio-based alcohol ethoxylates

- 5.5.2 Bio-based polysorbates

- 5.5.3 Bio-based PEG derivatives

- 5.5.4 Bio-based castor oil ethoxylates

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Microbial fermentation technology

- 6.3 Chemical synthesis from renewable feedstocks

- 6.4 Enzymatic synthesis

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Hair care

- 7.3 Skin care

- 7.4 Oral care

- 7.5 Baby care

- 7.6 Specialty personal care

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Clariant AG

- 9.3 Evonik Industries AG

- 9.4 Croda International Plc

- 9.5 Kao Corporation

- 9.6 Stepan Company

- 9.7 Sino Lion

- 9.8 Galaxy Surfactants Ltd

- 9.9 Ajinomoto Co., Inc.

- 9.10 Seppic

- 9.11 Lonza

- 9.12 Innospec

- 9.13 Holiferm Ltd

- 9.14 Solvay / Syensqo

- 9.15 Miwon Commercial

綠色生物溶劑市場:2026-2032年全球市場預測(依產品類型、原料技術、應用、終端用戶產業及通路分類)

綠色生物溶劑市場:2026-2032年全球市場預測(依產品類型、原料技術、應用、終端用戶產業及通路分類) 生物基塗料市場:依產品種類、應用、樹脂類型及地區分類。

生物基塗料市場:依產品種類、應用、樹脂類型及地區分類。 綠色溶劑市場:預測(至2034年)-按產品類型、純度、應用、最終用戶和地區分類的全球分析

綠色溶劑市場:預測(至2034年)-按產品類型、純度、應用、最終用戶和地區分類的全球分析 2026年全球生物基界面活性劑市場報告綠色氣體市場:按類型、原料、應用和地區分類

2026年全球生物基界面活性劑市場報告綠色氣體市場:按類型、原料、應用和地區分類 環保溶劑和生物溶劑市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年

環保溶劑和生物溶劑市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年 全球生物基界面活性劑市場2026年全球綠色溶劑市場報告

全球生物基界面活性劑市場2026年全球綠色溶劑市場報告 生物溶劑市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)深共熔溶劑市場:按類型、成分、製造流程、形態、應用和最終用戶分類 - 全球預測(2026-2032年)

生物溶劑市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)深共熔溶劑市場:按類型、成分、製造流程、形態、應用和最終用戶分類 - 全球預測(2026-2032年)