|

市場調查報告書

商品編碼

1959304

醋基保鮮系統市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Vinegar-based Preservation Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

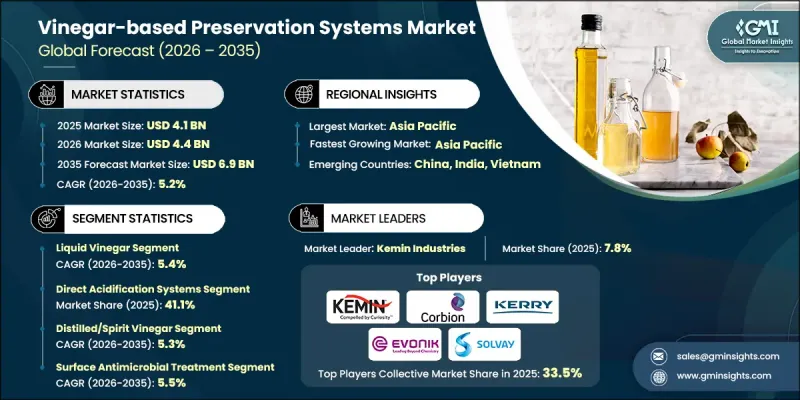

2025 年全球醋基保鮮系統市場價值為 41 億美元,預計到 2035 年將達到 69 億美元,年複合成長率為 5.2%。

該市場涵蓋多種解決方案,例如液態醋、粉狀醋和乾醋、濃縮型醋、緩衝醋混合物以及有機醋技術。這些系統採用先進的製造流程開發,包括複合保藏系統、氯化鈣和醋酸組合系統、過氧乙酸 (PAA) 基溶液、緩衝系統和直接酸化技術。應用範圍涵蓋蒸餾食品、飲料、調味醬料、肉類和家禽產品以及烘焙產品。市場成長的驅動力在於消費者對天然和潔淨標示保藏方法的需求不斷成長,以及食品安全和永續加工方法監管支援的加強。世界各國政府正透過資助和支持政策,促進採用環境友善且對消費者友善的保藏技術,用於天然抗菌解決方案的研究。目前,亞太地區在醋基保藏系統市場中處於領先地位,這主要得益於中國、印度和日本等國家對生產能力和基礎設施的大力投資。同時,北美市場正迅速崛起,這得益於技術創新、潔淨標示成分支出的增加以及消費者對加工最少和天然保藏食品日益成長的偏好。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 41億美元 |

| 預測金額 | 69億美元 |

| 複合年成長率 | 5.2% |

預計到2025年,液態醋的市佔率將達到53.4%,並在2035年之前以5.4%的複合年成長率成長。液態醋在眾多食品類別中的廣泛應用,反映了其強大的抗菌性能和對不同配方的適應性。液態醋符合潔淨標示的趨勢,滿足了消費者對透明成分標籤的需求。由於液態醋的高效性、可靠性以及無需依賴合成添加劑即可延長保存期限的特性,食品生產商正將其應用於各種保鮮製程。

預計到2025年,直接酸化系統市佔率將達到41.1%,到2035年將以5.2%的複合年成長率成長。這些系統因其能夠快速且有效率地控制微生物,並能無縫整合到大規模食品生產環境中而備受認可。食品安全標準的提高和產品品質的維持能力正在推動商業加工設施對該系統的應用。對低加工食品需求的成長以及對食品安全合規性的日益關注,持續加速醋基保鮮系統市場對直接酸化技術的應用。

預計2026年至2035年,北美醋基防腐劑市場將以5.2%的複合年成長率成長。市場擴張的驅動力主要來自永續加工技術的創新以及緩衝醋配方作為潔淨標示防腐劑的日益普及。該地區的企業正致力於開發符合食品安全法規和循環經濟舉措的天然解決方案。消費者對人工防腐劑潛在健康風險的日益關注,促使製造商轉向使用GRAS認證的醋基防腐劑,從而推動市場持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 液體醋

- 濃縮醋

- 醋粉

- 緩衝醋 - 液體

- 緩衝醋 - 乾粉狀

- 有機醋

- 其他

第6章 市場估計與預測:依技術類型分類,2022-2035年

- 直接酸化系統

- 緩衝醋系統

- 鈉基

- 鉀基

- 鈣基

- 氯化鈣+醋酸體系

- 複合儲能系統

- 基於過氧乙酸(PAA)的體系

- 其他

第7章 市場估價與預測:依原料分類的醋市場,2022-2035年

- 蒸餾醋/烈酒醋

- 蘋果醋

- 葡萄酒醋

- 紅酒醋

- 白葡萄酒醋

- 香醋

- 米醋

- 其他

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 醃菜和鹹味食品

- 表面抗菌處理

- 醃製和浸泡系統

- 調味料和調味料的混合

- 散裝/工業儲存系統

- 發酵助劑和保肝劑

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Kemin Industries

- Corbion NV

- Kerry Group

- Evonik Industries

- Solvay SA

- IFF

- Novonesis

- Galactic SA

- Henan Weichuang

- YOTA BIO

- Hydrite Chemical

- BioSafe Systems

- Sunson Biotech

- Handary SA

- AmTech Ingredients

The Global Vinegar-based Preservation Systems Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 6.9 billion by 2035.

The market includes a wide range of solutions such as liquid vinegar, powdered and dry vinegar formats, concentrated variants, buffered vinegar blends, and organic vinegar technologies. These systems are developed using advanced production approaches, including combination preservation systems, calcium chloride with acetic acid systems, peroxyacetic acid (PAA)-based solutions, buffered systems, and direct acidification technologies. Applications span ready-to-eat meals, beverages, sauces and dressings, meat and poultry, and bakery products. Growth is being fueled by rising demand for natural and clean-label preservation methods, along with increasing regulatory support for food safety and sustainable processing practices. Governments worldwide are encouraging the adoption of environmentally responsible and consumer-friendly preservation technologies by funding research into natural antimicrobial solutions and implementing supportive policies. Asia Pacific currently leads the vinegar-based preservation systems market, driven by strong investments in production capacity and infrastructure across countries such as China, India, and Japan. Meanwhile, North America is emerging rapidly due to technological innovation, higher spending on clean-label ingredients, and a growing consumer preference for minimally processed and naturally preserved food products.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 5.2% |

The liquid vinegar segment accounted for 53.4% share in 2025 and is anticipated to grow at a CAGR of 5.4% through 2035. Its widespread adoption across multiple food categories reflects its strong antimicrobial performance and compatibility with diverse formulations. Liquid vinegar aligns with clean label trends and meets consumer demand for transparent ingredient declarations. Food manufacturers are incorporating liquid vinegar into various preservation processes due to its effectiveness, reliability, and ability to support extended shelf life without relying on synthetic additives.

The direct acidification systems segment held 41.1% share in 2025 and is forecast to grow at a CAGR of 5.2% by 2035. These systems are recognized for delivering fast and efficient microbial control while integrating seamlessly into large-scale food production environments. Their ability to enhance food safety standards and maintain product integrity has strengthened their adoption across commercial processing facilities. Rising demand for minimally processed food options and heightened attention to food safety compliance continue to accelerate the deployment of direct acidification technologies within the vinegar-based preservation systems market.

North America Vinegar-based Preservation Systems Market is expected to grow at a CAGR of 5.2% between 2026 and 2035. Market expansion is being supported by innovation in sustainable processing techniques and increasing use of buffered vinegar formulations as clean-label preservation ingredients. Companies across the region are focusing on developing natural solutions that align with food safety regulations and circular economy initiatives. Growing consumer awareness regarding the potential health concerns associated with artificial preservatives has encouraged manufacturers to shift toward GRAS-designated, vinegar-based preservation ingredients, thereby driving sustained market growth.

Key companies operating in the Global Vinegar-based Preservation Systems Market include Kerry Group, Kemin Industries, Corbion N.V., Solvay S.A., IFF, Evonik Industries, Galactic S.A., Novonesis, Hydrite Chemical, Henan Weichuang, BioSafe Systems, YOTA BIO, Handary S.A., Sunson Biotech, and AmTech Ingredients. Companies in the Global Vinegar-based Preservation Systems Market are strengthening their competitive position through strategic product innovation, expansion of clean label portfolios, and investment in sustainable production technologies. Many players are enhancing research and development capabilities to create advanced antimicrobial blends that meet evolving regulatory and consumer standards. Strategic partnerships, capacity expansions, and regional manufacturing investments are also being used to improve supply chain resilience and global reach. Firms are focusing on certifications, GRAS compliance, and transparent sourcing practices to build brand credibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Technology type

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Liquid vinegar

- 5.3 Concentrated vinegar

- 5.4 Dry / powder vinegar

- 5.5 Buffered vinegar - liquid

- 5.6 Buffered vinegar - dry / powder

- 5.7 Organic vinegar

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Technology Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Direct acidification systems

- 6.3 Buffered vinegar systems

- 6.3.1 Sodium-based

- 6.3.2 Potassium-based

- 6.3.3 Calcium-based

- 6.4 Calcium chloride + acetic acid systems

- 6.5 Combination preservation systems

- 6.6 Peroxyacetic acid (PAA)-based systems

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Vinegar Source, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Distilled / spirit vinegar

- 7.3 Apple cider vinegar

- 7.3.1 Wine vinegar

- 7.3.2 Red wine vinegar

- 7.4 White wine vinegar

- 7.5 Balsamic vinegar

- 7.6 Rice vinegar

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pickling & brining

- 8.3 Surface antimicrobial treatment

- 8.4 Marinade & injection systems

- 8.5 Dressing & condiment formulation

- 8.6 Bulk / industrial preservation systems

- 8.7 Fermentation aid & pH control

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Kemin Industries

- 10.2 Corbion N.V.

- 10.3 Kerry Group

- 10.4 Evonik Industries

- 10.5 Solvay S.A.

- 10.6 IFF

- 10.7 Novonesis

- 10.8 Galactic S.A.

- 10.9 Henan Weichuang

- 10.10 YOTA BIO

- 10.11 Hydrite Chemical

- 10.12 BioSafe Systems

- 10.13 Sunson Biotech

- 10.14 Handary S.A.

- 10.15 AmTech Ingredients

細胞冷凍保存市場:按產品類型、應用、最終用戶和地區分類。

細胞冷凍保存市場:按產品類型、應用、最終用戶和地區分類。 冷凍保存設備市場:按設備類型、儲存方法、容量、應用和最終用戶分類,全球預測,2026-2032年

冷凍保存設備市場:按設備類型、儲存方法、容量、應用和最終用戶分類,全球預測,2026-2032年 2026年全球冷凍保存設備市場報告冷凍保存設備市場:按設備類型、冷凍材料、應用、最終用戶、地區分類

2026年全球冷凍保存設備市場報告冷凍保存設備市場:按設備類型、冷凍材料、應用、最終用戶、地區分類 全球細胞冷凍保存市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球細胞冷凍保存市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 細胞冷凍保存市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、地區和競爭對手分類,2021-2031年HPV子宮頸細胞保存液市場:按保存技術、應用和分銷管道分類的全球預測(2026-2032年)液態氮冷凍治療艙市場(按艙體類型、應用、最終用戶和分銷管道分類)—2026-2032年全球預測2025年全球幹細胞冷凍保存市場報告

細胞冷凍保存市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、地區和競爭對手分類,2021-2031年HPV子宮頸細胞保存液市場:按保存技術、應用和分銷管道分類的全球預測(2026-2032年)液態氮冷凍治療艙市場(按艙體類型、應用、最終用戶和分銷管道分類)—2026-2032年全球預測2025年全球幹細胞冷凍保存市場報告 細胞冷凍保存市場規模、佔有率及成長分析(按產品、應用、最終用途及地區分類)-2026-2033年產業預測

細胞冷凍保存市場規模、佔有率及成長分析(按產品、應用、最終用途及地區分類)-2026-2033年產業預測