|

市場調查報告書

商品編碼

1959291

按需付費訂閱市場機會、成長要素、產業趨勢分析及預測(2026-2035 年)Performance-on-Demand Subscription Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

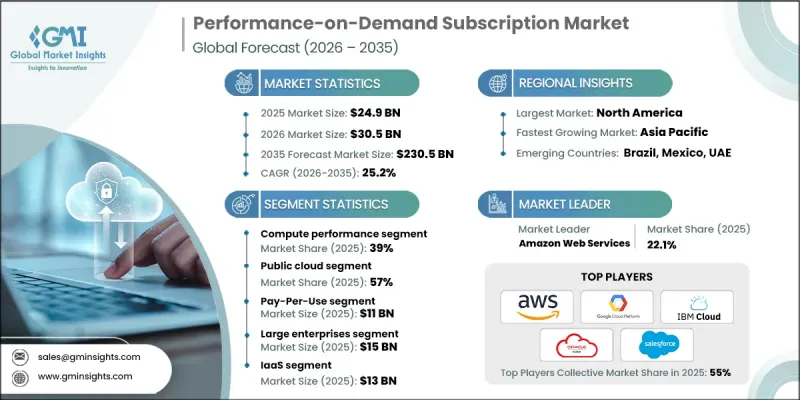

2025 年全球按需付費訂閱市場價值為 249 億美元,預計到 2035 年將達到 2,305 億美元,年複合成長率為 25.2%。

市場成長的驅動力來自雲端原生架構的加速轉型、企業對計量型IT模式日益成長的偏好,以及在維持成本控制的同時即時最佳化效能的迫切需求。各行各業的組織都面臨越來越大的壓力,需要提高營運柔軟性、控制基礎設施支出、增強應用程式回應能力,並遵守不斷發展的安全和監管標準。因此,將資源利用率與實際工作負載需求掛鉤的基於效能的訂閱框架正變得越來越普遍。企業正在從固定容量的基礎設施轉向可擴展的、基於使用量的環境,以支援動態配置和可衡量的效能結果。這種轉變在混合雲和多重雲端環境中尤其顯著,因為企業需要持續了解運算、儲存、網路和應用程式的效率。因此,隨著全球數位轉型力度的加大,隨選性能訂閱市場預計將顯著成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 249億美元 |

| 預測金額 | 2305億美元 |

| 複合年成長率 | 25.2% |

快速的技術進步正在重塑按需效能訂閱的格局。人工智慧 (AI) 和機器學習的進步實現了預測性資源分配、自動化工作負載平衡和即時基礎設施分析。現代可觀測性工具和編配平台提高了分散式 IT 系統的可見性,而邊緣到雲端的連接則改善了響應速度和營運彈性。無伺服器運算框架和模組化訂閱模式透過無需大量資本支出即可實現資源即時擴展,進一步變革了傳統的基礎設施策略。行業相關人員越來越關注可互通的、以雲端為中心的訂閱生態系統,並希望對績效指標和支出模式進行精細控制。這些發展正在重新定義企業 IT 策略,為全球企業、中小企業和專業工業環境帶來更敏捷、高效和數據驅動的基礎設施管理。

預計到2025年,計算性能細分市場將佔據39%的市場佔有率,並在2026年至2035年間以25.3%的複合年成長率成長。該細分市場之所以能保持主導地位,是因為運算資源是雲端、混合雲和多重雲端環境中數位工作負載的基礎。企業依靠可擴展的運算服務來管理不斷變化的處理需求、支援進階分析並保持應用程式的回應速度。動態分配虛擬化和容器化資源的能力,透過確保業務連續性並最大限度地減少延遲和資源利用不足,進一步鞏固了該細分市場的主導地位。

預計到2025年,公共雲端市場佔有率將達到57%,並在2035年之前以25.7%的複合年成長率成長。對於地理位置分散的企業而言,公共雲端平台憑藉其可擴展性、維運柔軟性和成本最佳化優勢,仍是首選的部署模式。企業青睞公共雲端環境,因為它能夠集中進行效能監控、智慧工作負載最佳化、提供預測分析功能並存取遠端系統。公有雲能夠即時擴展運算、儲存、網路和應用服務,同時與現有IT系統保持無縫整合,這持續推動其廣泛應用和市場領先地位。

預計2025年,美國按需付費效能訂閱市場規模將達到約80億美元,市佔率高達83%。成熟的雲端基礎設施、先進的數位生態系統以及人工智慧驅動的效能管理解決方案的快速整合是推動這一成長的主要因素。高速連接框架的早期應用,例如支援預測性工作負載分析、自動化資源配置以及高效安全的IT運維,也促進了該地區的成長。企業對技術的廣泛應用以及對雲端創新持續投入,進一步鞏固了北美在按需付費性能訂閱市場的領先地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 雲端和混合IT環境的廣泛應用

- 對IT支出成本最佳化和透明度的需求日益成長

- 數據密集型和人工智慧驅動型工作負載的擴展

- 自動化和可觀測性技術的進步

- 產業潛在風險與挑戰

- 與成本可預測性相關的挑戰

- 安全、合規和供應商鎖定風險

- 市場機遇

- 人工智慧驅動的效能最佳化平台的應用日益廣泛

- 拓展新興市場與中小企業領域

- 從邊緣到雲端的整合

- 行業特定客製化

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國:國家公路交通安全管理局 (NHTSA) 和聯邦通訊委員會 (FCC) 指南

- 加拿大:加拿大和加拿大創新、科學與經濟發展部 (ISED) 指南

- 歐洲

- 德國:聯邦交通和數位基礎設施部

- 法國:生態轉型部

- 英國:運輸部

- 義大利:基礎設施和運輸部

- 亞太地區

- 中國:工業和資訊化部

- 日本國土交通省

- 韓國國土交通部

- 印度:公路運輸與公路部

- 拉丁美洲

- 巴西:國家交通運輸署

- 墨西哥:通訊與運輸部部 (SCT)

- 中東和非洲

- 阿拉伯聯合大公國:工業與先進技術部

- 沙烏地阿拉伯:沙烏地阿拉伯標準、計量和品質研究院

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 使用案例場景

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依服務業分類,2022-2035年

- 運算效能

- 儲存吞吐量

- 網路效能

- 資料庫/分析效能

- 安全性能服務

第6章 市場估價與預測:依訂閱模式分類,2022-2035年

- 付費使用制

- 按層級分類的績效

- 動態縮放

- 油電混合套件

第7章 市場估算與預測:依部署類型分類,2022-2035年

- 公共雲端

- 私有雲端

- 混合雲端

第8章 市場估算與預測:依雲端服務模式分類,2022-2035年

- IaaS

- PaaS

- SaaS

- FaaS

第9章 市場估計與預測:依公司規模分類,2022-2035年

- 主要企業

- 小型企業

第10章 市場估計與預測:依產業分類,2022-2035年

- BFSI

- 衛生保健

- 零售與電子商務

- 溝通

- IT和軟體服務

- 其他

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第12章:公司簡介

- Global Player

- Alibaba Cloud

- Amazon Web Services(AWS)

- Dassault Systemes

- Google Cloud Platform(GCP)

- IBM Cloud

- Microsoft Azure

- Oracle Cloud

- PTC

- Salesforce

- Siemens

- Regional Player

- ANSYS

- Baidu Cloud

- EZ Crusher

- Hexagon

- Huawei Cloud

- Keestrack

- NEC

- OverBuilt

- SAP

- Tata Consultancy Services

- 新玩家

- CloudSigma

- Cohesity

- DigitalOcean

- Nutanix

- OutSystems

The Global Performance-on-Demand Subscription Market was valued at USD 24.9 billion in 2025 and is estimated to grow at a CAGR of 25.2% to reach USD 230.5 billion by 2035.

Market growth is fueled by the accelerating shift toward cloud-native architectures, the growing preference among enterprises for consumption-based IT models, and the increasing need to optimize performance in real-time while maintaining cost discipline. Organizations across industries are under mounting pressure to enhance operational flexibility, control infrastructure spending, improve application responsiveness, and comply with evolving security and regulatory standards. As a result, performance-based subscription frameworks that align resource utilization with actual workload demand are gaining widespread traction. Enterprises are moving away from fixed-capacity infrastructure toward scalable, usage-driven environments that support dynamic provisioning and measurable performance outcomes. This transition is particularly strong in hybrid and multi-cloud ecosystems, where businesses require continuous visibility into compute, storage, networking, and application efficiency. The performance-on-demand subscription market is therefore positioned for substantial expansion as digital transformation initiatives intensify globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.9 Billion |

| Forecast Value | $230.5 Billion |

| CAGR | 25.2% |

Rapid technological innovation is reshaping the performance-on-demand subscription landscape. Advancements in artificial intelligence and machine learning are enabling predictive resource allocation, automated workload balancing, and real-time infrastructure analytics. Modern observability tools and orchestration platforms are enhancing visibility across distributed IT systems, while edge-to-cloud connectivity is improving response times and operational resilience. Serverless computing frameworks and modular subscription models are further transforming traditional infrastructure strategies by allowing organizations to scale resources instantly without heavy capital expenditure. Industry participants are increasingly focused on interoperable, cloud-centric subscription ecosystems that provide granular control over performance metrics and spending patterns. These developments are redefining enterprise IT strategies by enabling more agile, efficient, and data-driven infrastructure management across global enterprises, SMEs, and specialized industry environments.

The compute performance segment accounted for 39% share in 2025 and is anticipated to grow at a CAGR of 25.3% from 2026 to 2035. This segment maintains a leading position because compute resources form the backbone of digital workloads across cloud, hybrid, and multi-cloud environments. Organizations rely on scalable compute services to manage fluctuating processing requirements, support advanced analytics, and maintain consistent application responsiveness. The ability to dynamically allocate virtualized and containerized resources ensures operational continuity while minimizing latency and resource underutilization, reinforcing the segment's dominance.

The public cloud segment held 57% share in 2025 and is forecast to grow at a CAGR of 25.7% through 2035. Public cloud platforms remain the preferred deployment model due to their scalability, operational flexibility, and cost optimization advantages across geographically distributed enterprises. Businesses favor public cloud environments for centralized performance monitoring, intelligent workload optimization, predictive analytics capabilities, and remote system accessibility. The capacity to scale compute, storage, networking, and application services in real time while integrating seamlessly with existing IT systems continues to drive widespread adoption and market leadership.

United States Performance-on-Demand Subscription Market accounted for 83% share, generating nearly USD 8 billion in 2025, owing to its mature cloud infrastructure, advanced digital ecosystem, and rapid integration of AI-powered performance management solutions. The region benefits from early deployment of predictive workload analytics, automated resource provisioning, and high-speed connectivity frameworks that support efficient and secure IT operations. Strong enterprise technology adoption and continuous investment in cloud innovation further solidify North America's dominant position within the performance-on-demand subscription market.

Major companies operating in the Global Performance-on-Demand Subscription Market include Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), IBM Cloud, Oracle Cloud, Alibaba Cloud, Salesforce, Siemens, Dassault Systemes, and PTC. Companies in the Performance-on-Demand Subscription Market are strengthening their competitive advantage through continuous platform innovation, AI-driven automation, and ecosystem expansion strategies. Providers are investing heavily in advanced analytics, intelligent workload orchestration, and predictive performance modeling to enhance service differentiation. Strategic partnerships and multi-cloud integrations enable broader market reach and seamless interoperability across enterprise environments. Many vendors are adopting flexible pricing models aligned with usage metrics to attract cost-conscious organizations. In addition, companies emphasize cybersecurity enhancements, compliance certifications, and edge integration capabilities to address complex regulatory and operational demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Services

- 2.2.3 Subscription Model

- 2.2.4 Deployment Mode

- 2.2.5 Cloud Service Model

- 2.2.6 Organization Size

- 2.2.7 Vertical

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Adoption of Cloud & Hybrid IT Environments

- 3.2.1.2 Growing Need for Cost Optimization & IT Spend Transparency

- 3.2.1.3 Expansion of Data-Intensive & AI-Driven Workloads

- 3.2.1.4 Advancements in Automation & Observability Technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cost Predictability Challenges

- 3.2.2.2 Security, Compliance & Vendor Lock-In Risks

- 3.2.3 Market opportunities

- 3.2.3.1 Growing Adoption of AI-Driven Performance Optimization Platforms

- 3.2.3.2 Expansion in Emerging Markets & SME Segment

- 3.2.3.3 Edge-to-Cloud Integration

- 3.2.3.4 Industry-Specific Customization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: NHTSA & FCC Guidelines

- 3.4.1.2 Canada: Canada & ISED Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: Federal Ministry of Transport & Digital Infrastructure

- 3.4.2.2 France: Ministry for the Ecological Transition

- 3.4.2.3 UK: Department for Transport

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Industry and Information Technology

- 3.4.3.2 Japan: Ministry of Land, Infrastructure, Transport and Tourism

- 3.4.3.3 South Korea: Ministry of Land, Infrastructure and Transport

- 3.4.3.4 India: Ministry of Road Transport & Highways

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Transport Agency

- 3.4.4.2 Mexico: Secretariat of Communications and Transportation (SCT)

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Ministry of Industry and Advanced Technology

- 3.4.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Compute Performance

- 5.3 Storage & Throughput

- 5.4 Network Performance

- 5.5 Database/Analytics Performance

- 5.6 Security Performance Services

Chapter 6 Market Estimates & Forecast, By Subscription Model, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Pay-Per-Use

- 6.3 Tiered Performance

- 6.4 Dynamic Scaling

- 6.5 Hybrid Packages

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Public Cloud

- 7.3 Private Cloud

- 7.4 Hybrid Cloud

Chapter 8 Market Estimates & Forecast, By Cloud Service Model, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 IaaS

- 8.3 PaaS

- 8.4 SaaS

- 8.5 FaaS

Chapter 9 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 Large Enterprises

- 9.3 SMEs

Chapter 10 Market Estimates & Forecast, By Vertical, 2022 - 2035 ($ Bn)

- 10.1 Key trends

- 10.2 BFSI

- 10.3 Healthcare

- 10.4 Retail & E-commerce

- 10.5 Telecom

- 10.6 IT & Software Services

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Singapore

- 11.4.6 South Korea

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Global Player

- 12.1.1 Alibaba Cloud

- 12.1.2 Amazon Web Services (AWS)

- 12.1.3 Dassault Systemes

- 12.1.4 Google Cloud Platform (GCP)

- 12.1.5 IBM Cloud

- 12.1.6 Microsoft Azure

- 12.1.7 Oracle Cloud

- 12.1.8 PTC

- 12.1.9 Salesforce

- 12.1.10 Siemens

- 12.2 Regional Player

- 12.2.1 ANSYS

- 12.2.2 Baidu Cloud

- 12.2.3 EZ Crusher

- 12.2.4 Hexagon

- 12.2.5 Huawei Cloud

- 12.2.6 Keestrack

- 12.2.7 NEC

- 12.2.8 OverBuilt

- 12.2.9 SAP

- 12.2.10 Tata Consultancy Services

- 12.3 Emerging Players

- 12.3.1 CloudSigma

- 12.3.2 Cohesity

- 12.3.3 DigitalOcean

- 12.3.4 Nutanix

- 12.3.5 OutSystems

付費電視服務市場:2026-2032年全球市場預測(按服務類型、訂閱方案、裝置類型、影像品質和最終用戶分類)

付費電視服務市場:2026-2032年全球市場預測(按服務類型、訂閱方案、裝置類型、影像品質和最終用戶分類) 付費電視市場規模、佔有率、趨勢和預測:按類型、技術、應用和地區分類,2026-2034 年

付費電視市場規模、佔有率、趨勢和預測:按類型、技術、應用和地區分類,2026-2034 年 2026年全球付費電視市場報告

2026年全球付費電視市場報告 2026-2030年全球訂閱服務市場

2026-2030年全球訂閱服務市場 付費電視市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶和解決方案分類訂閱服務市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和交付類型分類

付費電視市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶和解決方案分類訂閱服務市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和交付類型分類 付費電視市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

付費電視市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 全球電視分發模式市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球電視分發模式市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 2026-2030年全球付費電視市場影片編輯與剪輯軟體市場:按部署模式、平台、定價模式、最終用戶和應用程式分類,全球預測,2026-2032年

2026-2030年全球付費電視市場影片編輯與剪輯軟體市場:按部署模式、平台、定價模式、最終用戶和應用程式分類,全球預測,2026-2032年