|

市場調查報告書

商品編碼

1959290

汽車區域架構及網域控制器市場:機會、成長要素、產業趨勢分析及2026年至2035年預測Automotive Zonal Architecture and Domain Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球汽車區域架構和網域控制器市場價值為 49 億美元,預計到 2035 年將達到 207 億美元,年複合成長率為 16.1%。

市場成長的驅動力在於汽車電子設備設計和整合方式的根本性轉變。汽車製造商正從高度分散的電子系統轉向更集中、以軟體為中心的架構。傳統的汽車設計依賴眾多獨立的電控系統,這些單元透過龐大的線路網路連接,導致車輛重量增加、生產複雜性提高以及製造成本上升。區域架構重新思考了這種方法,它基於車輛的實體區域組織電子設備,並透過高速資料網路連接它們,從而顯著減少了佈線需求。這種精簡的結構有助於提高能源效率、簡化組裝流程,並推動向具有數位化可更新功能的軟體定義車輛的過渡。先進的通訊協定加速了來自感測器和車載系統的數據處理,而改進的電源分配則有助於最佳化車輛性能,尤其是在電動平台上。這些綜合優勢正在加速全球汽車產業的採用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 49億美元 |

| 預測金額 | 207億美元 |

| 複合年成長率 | 16.1% |

網域控制器架構市場佔有率高達 64.2%,預計到 2025 年將創造 32 億美元的市場規模。汽車製造商傾向於集中式運算系統,因為這種系統可以將多種車輛功能整合到少量高性能單元中。透過將駕駛輔助、資訊娛樂和車身電子設備等領域整合到單一控制器中,製造商可以降低系統複雜性和佈線密度。與傳統的汽車電子設計相比,這種方法還提高了可擴展性,並有助於實現更高級的軟體功能。

預計到2025年,乘用車市佔率將達到89.7%,到2035年市場規模將達到181億美元。由於先進數位功能和互聯技術的日益集中化,該領域的普及率很高。高產量和消費者對創新的需求使得乘用車成為實施基於區域和集中式電子系統的主要平台,從而能夠高效管理複雜的車輛功能。

美國汽車業專用架構域控制器市場預計到2025年將達到14億美元。軟體定義汽車平臺的強勁發展正在重塑該地區市場,製造商優先採用集中式電子架構以支援遠端軟體更新和快速功能部署。這種轉變正在推動電動車和下一代汽車對網域控制器解決方案的需求不斷成長。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 車輛電氣化進展

- 軟體定義車輛的普及應用不斷擴大

- 對ADAS(高級駕駛輔助系統)的需求不斷成長

- 增強的空中下載 (OTA) 更新功能

- 產業潛在風險與挑戰

- 網路安全與功能安全挑戰

- 開發和整合高度複雜

- 市場機遇

- 電動汽車和混合動力汽車平台的發展

- 汽車乙太網路技術的進步

- 擴展以軟體為中心的汽車生態系統

- 自動駕駛商用車領域的新機遇

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 聯邦通訊委員會

- 美國國家公路交通安全管理局(NHTSA)

- 加州空氣資源委員會(CARB)

- 加拿大運輸部

- 歐洲

- 歐盟委員會

- 聯合國歐洲經濟委員會世界汽車法規協調論壇

- 車輛認證機構

- 亞太地區

- 中華人民共和國工業與資訊化部(工信部)

- 日本汽車標準化國際中心

- 汽車業標準(AIS)

- 拉丁美洲

- 巴西汽車工業協會(ANFAVEA)

- INMETRO

- 國家公路安全委員會

- 中東和非洲

- 海灣標準組織

- 南非標準局

- 北美洲

- 波特的分析

- PESTEL 分析

- 技術與創新展望

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 永續性和環境影響

- 環境影響評估

- 社會影響和對社區的貢獻

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 架構與系統設計

- 網域控制器架構基礎知識

- 區域建築設計原則

- 混合架構實施策略

- 集中式和分散式計算模型

- 高效能運算(HPC)的整合

- 車輛伺服器架構

- 區域閘道器設計與部署

- 軟體定義車輛(SDV)策略

- 服務導向架構(SOA)的實施

- 中介軟體平台和標準

- 自動駕駛車輛中的區域架構

- ADAS領域在區域系統中的整合

- 自動駕駛的感測器融合架構

- 即時數據處理要求

- 冗餘和容錯系統

- 專注的感知與決策

- 案例研究

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估價與預測:依建築類型分類,2022-2035年

- 網域控制器架構

- 區域建築

- 混合架構

第6章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車

- 中型商用車

- 大型商用車輛

第7章 市場估計與預測:依促進因素分類,2022-2035年

- 內燃機車

- 電動車和混合動力汽車

- 電池式電動車(BEV)

- 插電式混合動力車(PHEV)

- 燃料電池電動車(FCEV)

第8章 市場估算與預測:依自動駕駛等級分類,2022-2035年

- 一級

- 二級

- 3級

- 4級和5級

第9章 市場估算與預測:依通訊協定,2022-2035年

- 基於 CAN/LIN 的系統

- 以乙太網路為基礎的系統

第10章 市場估價與預測:依電壓分類,2022-2035年

- 12V系統

- 48V系統

第11章 市場估計與預測:依應用領域分類,2022-2035年

- ADAS領域

- 動力傳動系統/電動車續航里程

- 身體與舒適類別

- 駕駛座/資訊娛樂區域

- 安全場

- 底盤和運動場

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 捷克共和國

- 比利時

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 世界公司

- Robert Bosch

- Continental

- Aptiv

- NXP Semiconductors

- Infineon

- Valeo

- STMicroelectronics

- Texas Instruments

- Visteon

- Harman

- Panasonic

- NVIDIA

- Qualcomm

- onsemi

- 區域玩家

- HiRain

- SemiDrive

- Sonatus

- ETAS

- Elektrobit

- Lear

- Magna

- Marelli

- DENSO

- 新興企業

- TTTech

- GuardKnox

- Ambarella

- Aurora Labs

- Rivian

- AUMOVIO

- Molex

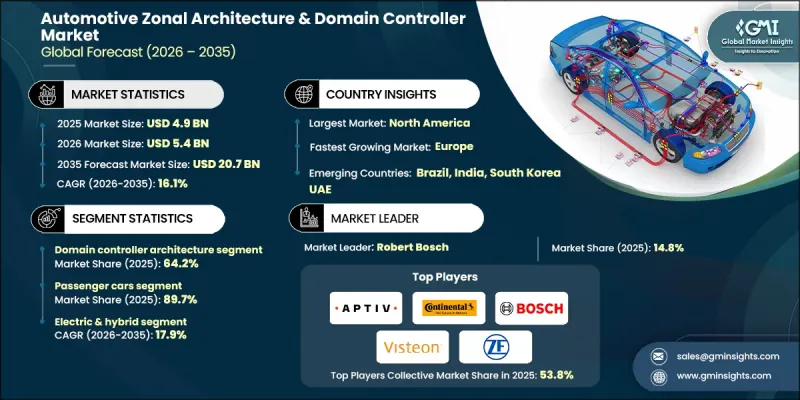

The Global Automotive Zonal Architecture & Domain Controller Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 16.1% to reach USD 20.7 billion by 2035.

Market growth is driven by a fundamental shift in how vehicle electronics are designed and integrated. Automakers are moving away from highly fragmented electronic systems toward more centralized and software-focused architectures. Traditional vehicle designs relied on many independent electronic control units connected through extensive wiring networks, which increased vehicle weight, production complexity, and manufacturing costs. Zonal architecture restructures this approach by organizing electronics based on physical vehicle zones and connecting them through high-speed data networks, significantly reducing wiring requirements. This streamlined structure improves energy efficiency, simplifies assembly processes, and supports the transition toward software-defined vehicles where functionality can be updated digitally. Advanced communication protocols enable faster data handling from sensors and onboard systems, while improved power distribution helps optimize vehicle performance, particularly in electrified platforms. Together, these benefits are accelerating adoption across the global automotive industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 16.1% |

The domain controller architecture segment held 64.2% share, generating USD 3.2 billion in 2025. Automakers are favoring centralized computing systems because they consolidate multiple vehicle functions into fewer, high-performance units. By integrating areas such as driver assistance, infotainment, and body electronics into unified controllers, manufacturers reduce system complexity and wiring density. This approach also enhances scalability and makes it easier to deploy advanced software capabilities compared to legacy vehicle electronics designs.

The passenger cars segment accounted for 89.7% share in 2025 and is expected to reach USD 18.1 billion by 2035. Adoption is higher in this segment due to the growing concentration of advanced digital features and connected technologies. High production volumes and consumer demand for innovation make passenger vehicles the primary platform for introducing zonal and centralized electronic systems, enabling more efficient management of complex vehicle functions.

U.S. Automotive Zonal Architecture & Domain Controller Market reached USD 1.4 billion in 2025. The regional market is being shaped by strong momentum toward software-defined vehicle platforms, with manufacturers emphasizing centralized electronic architectures to support remote software updates and faster feature deployment. This shift is reinforcing demand for domain controller solutions across electric and next-generation vehicles.

Key companies operating in the Global Automotive Zonal Architecture & Domain Controller Market include Robert Bosch, Aptiv, Continental, ZF, Visteon, Valeo, NXP, Infineon, Qualcomm, and Onsemi. Companies in the automotive zonal architecture and domain controller market are strengthening their market position through heavy investment in advanced semiconductor development and centralized computing platforms. Strategic partnerships with automakers and software providers are helping accelerate the integration of scalable electronic architectures. Many players are expanding research efforts focused on high-speed networking, power management, and cybersecurity to support software-defined vehicles. Portfolio diversification, regional expansion, and early involvement in next-generation vehicle programs are also key priorities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Architecture

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Autonomy level

- 2.2.6 Communication Protocol

- 2.2.7 Voltage

- 2.2.8 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising vehicle electrification

- 3.2.1.2 Increasing software-defined vehicle adoption

- 3.2.1.3 Growing demand for advanced driver assistance systems (ADAS)

- 3.2.1.4 Expansion of over-the-air (OTA) update capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity and functional safety challenges

- 3.2.2.2 High development and integration complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of electric and hybrid vehicle platforms

- 3.2.3.2 Advancements in automotive ethernet technologies

- 3.2.3.3 Expansion of Software-Centric Automotive Ecosystems

- 3.2.3.4 Emerging opportunities in autonomous commercial vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Communications Commission

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 California Air Resources Board (CARB)

- 3.4.1.4 Transport Canada

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 UNECE World Forum for Harmonization of Vehicle Regulations

- 3.4.2.3 Vehicle Certification Agency

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (MIIT), China

- 3.4.3.2 Japan Automobile Standards Internationalization Center

- 3.4.3.3 Automotive Industry Standards (AIS)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian Association of Automotive Vehicle Manufacturers (ANFAVEA)

- 3.4.4.2 INMETRO

- 3.4.4.3 National Road Safety Commission

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Standards Organization

- 3.4.5.2 South African Bureau of Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Architecture & system design

- 3.11.1 Domain controller architecture fundamentals

- 3.11.2 Zonal architecture design principles

- 3.11.3 Hybrid architecture implementation strategies

- 3.11.4 Centralized vs decentralized computing models

- 3.11.5 High-performance computing (HPC) integration

- 3.12 Vehicle server architecture

- 3.12.1 Zonal gateway design and placement

- 3.12.2 Software Defined Vehicle (SDV) Strategy

- 3.12.3 Service-oriented architecture (SOA) implementation

- 3.12.4 Middleware platforms and standards

- 3.13 Zonal architecture in autonomous vehicles

- 3.13.1 ADAS domain integration in zonal systems

- 3.13.2 Sensor fusion architecture for autonomy

- 3.13.3 Real-time data processing requirements

- 3.13.4 Redundancy and fail-operational systems

- 3.13.5 Centralized perception and decision making

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Architecture, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Domain controller architecture

- 5.3 Zonal architecture

- 5.4 Hybrid architecture

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Internal Combustion Engine (ICE) vehicles

- 7.3 Electric & hybrid vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Fuel Cell Electric Vehicles (FCEV)

Chapter 8 Market Estimates & Forecast, By Autonomy level, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Level 1

- 8.3 Level 2

- 8.4 Level 3

- 8.5 Level 4 & Level 5

Chapter 9 Market Estimates & Forecast, By Communication protocol, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 CAN / LIN-based system

- 9.3 Ethernet-based system

Chapter 10 Market Estimates & Forecast, By Voltage, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 12V system

- 10.3 48V system

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 ADAS domain

- 11.3 Powertrain / EV power domain

- 11.4 Body & comfort domain

- 11.5 Cockpit / infotainment domain

- 11.6 Safety domain

- 11.7 Chassis & motion domain

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Czech Republic

- 12.3.7 Belgium

- 12.3.8 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 Robert Bosch

- 13.1.2 Continental

- 13.1.3 Aptiv

- 13.1.4 NXP Semiconductors

- 13.1.5 Infineon

- 13.1.6 Valeo

- 13.1.7 STMicroelectronics

- 13.1.8 Texas Instruments

- 13.1.9 Visteon

- 13.1.10 Harman

- 13.1.11 Panasonic

- 13.1.12 NVIDIA

- 13.1.13 Qualcomm

- 13.1.14 onsemi

- 13.2 Regional players

- 13.2.1 HiRain

- 13.2.2 SemiDrive

- 13.2.3 Sonatus

- 13.2.4 ETAS

- 13.2.5 Elektrobit

- 13.2.6 Lear

- 13.2.7 Magna

- 13.2.8 Marelli

- 13.2.9 DENSO

- 13.3 Emerging players

- 13.3.1 TTTech

- 13.3.2 GuardKnox

- 13.3.3 Ambarella

- 13.3.4 Aurora Labs

- 13.3.5 Rivian

- 13.3.6 AUMOVIO

- 13.3.7 Molex

電子控制管理市場:2026-2032年全球市場預測(依產品類型、技術、安裝類型、應用及最終用戶產業分類)汽車電控系統市場:2026-2032年全球市場預測(依車輛類型、動力系統、自動駕駛等級、電子架構、應用與銷售管道)硬體在環 (HIL) 模擬市場:按類型、組件、測試類型、應用和最終用戶分類-2026-2032 年全球市場預測

電子控制管理市場:2026-2032年全球市場預測(依產品類型、技術、安裝類型、應用及最終用戶產業分類)汽車電控系統市場:2026-2032年全球市場預測(依車輛類型、動力系統、自動駕駛等級、電子架構、應用與銷售管道)硬體在環 (HIL) 模擬市場:按類型、組件、測試類型、應用和最終用戶分類-2026-2032 年全球市場預測 2026年全球汽車ECU市場報告2026年全球汽車智慧駕駛座系統晶片(SoC)市場報告汽車電子控制系統高度感測器市場:依產品類型、技術、車輛類型、應用和銷售管道分類-2026-2032年全球市場預測球柵陣列封裝市場:依封裝類型、基板材料、間距、I/O數量、互連結構及最終用途產業分類-2026年至2032年全球預測全球空氣彈簧壓縮機ECU市場(按車輛類型、ECU類型、應用和分銷管道分類)預測(2026-2032年)

2026年全球汽車ECU市場報告2026年全球汽車智慧駕駛座系統晶片(SoC)市場報告汽車電子控制系統高度感測器市場:依產品類型、技術、車輛類型、應用和銷售管道分類-2026-2032年全球市場預測球柵陣列封裝市場:依封裝類型、基板材料、間距、I/O數量、互連結構及最終用途產業分類-2026年至2032年全球預測全球空氣彈簧壓縮機ECU市場(按車輛類型、ECU類型、應用和分銷管道分類)預測(2026-2032年) 汽車電控系統市場機會、成長要素、產業趨勢分析及2026年至2035年預測

汽車電控系統市場機會、成長要素、產業趨勢分析及2026年至2035年預測 全球汽車電控系統(ECU)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球汽車電控系統(ECU)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)