|

市場調查報告書

商品編碼

1959287

清真原料市場機會、成長要素、產業趨勢分析及2026年至2035年預測。Halal Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

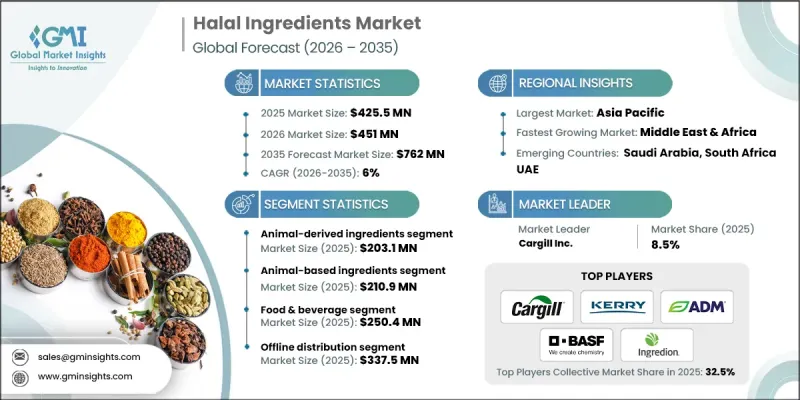

2025 年全球清真原料市場價值為 4.255 億美元,預計到 2035 年將達到 7.62 億美元,年複合成長率為 6%。

該市場被定義為負責生產和供應食品飲料、藥品、化妝品及相關領域清真合規原料的全球生態系統。清真原料的發展遵循嚴格的倫理和宗教框架,其採購、加工和分銷均保證符合公認的清真原則。這個合規框架被認為是建立消費者信任的關鍵要素。市場成長的驅動力來自全球對清真認證產品日益成長的需求,而收入水平的提高、城市化的快速發展以及跨境貿易的擴張則為其提供了支持。東南亞、中東和北非的消費趨勢尤其強勁,而歐洲和北美的需求也因消費者對清真標準的信心不斷增強而加速成長。此外,認證系統和標籤規範的協調統一提高了透明度,也為市場提供了支持,從而增強了產品在傳統和非傳統消費者中的可信度。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 4.255億美元 |

| 預測金額 | 7.62億美元 |

| 複合年成長率 | 6% |

預計到2025年,動物性原料市場規模將達到2.031億美元。此類別所包含的原料需要對採購慣例、可追溯性和品質保證系統進行嚴格監控,以符合國際清真法規。同時,受飲食習慣改變和人們對植物來源營養日益成長的興趣推動,植物來源原料的需求持續成長。採用微生物和發酵方法生產的原料也越來越受到關注,生產商透過認證的生產環境和受控的生產流程來確保合規性。

預計到2025年,線下通路的銷售額將達到3.375億美元。儘管市場結構涵蓋實體和數位銷售平台,但由於工業買家長期採購的習慣,面對面購買仍佔據主導地位。實體零售和B2B通路繼續發揮核心作用,尤其是在大批量採購中優先考慮直接驗證產品真偽的情況下。

預計到2035年,北美清真原料市場規模將達8,010萬美元。該地區的成長與日益成長的文化多樣性以及公眾對清真標準的認知不斷提高密切相關。食品零售商和服務供應商正在擴大其清真認證產品的種類,消費者也對符合道德規範的植物來源配方產品表現出越來越濃厚的興趣。都市區仍然是主要的需求中心,這得益於標籤規範的改進以及零售環境中清真產品的專門陳列。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球對符合清真標準產品的需求不斷成長

- 主要市場的可支配所得增加和都市化進程加快

- 健康意識的提高和對符合道德規範的產品的偏好

- 產業潛在風險與挑戰

- 清真認證和合規高成本

- 日益複雜的供應鏈所帶來的營運挑戰

- 市場機遇

- 利用區塊鏈和物聯網實現供應鏈可追溯性

- 食品加工和品管的自動化提高了效率

- 利用植物來源和種植技術開發清真認證替代品

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 動物源性原料

- 肉

- 乳製品

- 明膠

- 膠原蛋白

- 酵素

- 植物來源原料

- 蛋白質

- 糧食

- 油脂

- 提煉

- 源自微生物和發酵

- 酵素

- 培養細菌

- 微發酵蛋白

- 合成/化學

- 合成添加劑

- 香味

- 色素

- 其他

第6章 市場估計與預測:依原料來源分類,2022-2035年

- 動物源性原料

- 植物來源原料

- 微生物/發酵衍生原料

- 合成/化學合成原料

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 飲食

- 肉類和家禽產品

- 乳製品和乳製品替代品

- 麵包和糖果甜點

- 飲料

- 小吃和開胃菜

- 加工食品和蒸餾食品

- 調味料和醬汁

- 其他

- 製藥

- 明膠膠囊

- 添加劑

- 藥物原料藥(API)

- 維生素和補充劑

- 其他

- 化妝品和個人護理

- 護膚和身體保養

- 護髮

- 口腔護理

- 香水/香氛

- 彩妝品(化妝品)

- 其他

- 飼料和寵物食品

- 牲畜飼料(牛、羊、山羊)

- 家禽飼料(雞、火雞)

- 水產飼料(魚、蝦)

- 其他

第8章 市場估算與預測:依通路分類,2022-2035年

- 線下分發

- 大賣場和超級市場

- 便利商店

- 清真專賣店

- 傳統市場與集市

- 對於餐飲服務業

- 其他

- 線上發行

- 電子商務市場

- 直接面對消費者 (DTC) 的品牌網站

- 線上訂餐服務

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- ADM

- Ajinomoto

- BASF SE

- Cargill Inc.

- Corbion

- DSM-Firmenich

- Givaudan

- Ingredion

- Kerry Group

- Roquette

The Global Halal Ingredients Market was valued at USD 425.5 million in 2025 and is estimated to grow at a CAGR of 6% to reach USD 762 million by 2035.

The market is defined as the worldwide ecosystem responsible for the production and supply of ingredients used across food and beverages, pharmaceuticals, cosmetics, and related sectors that comply with halal requirements. Halal ingredients are positioned as being developed under strict ethical and religious frameworks, ensuring that sourcing, processing, and logistics adhere to recognized halal principles. This compliance framework is presented as a key factor in building consumer confidence. Market growth is attributed to expanding global demand for halal-certified offerings, supported by rising income levels, rapid urban development, and growing cross-border trade. Strong consumption trends are noted across Southeast Asia as well as the Middle East and North Africa, while demand is also accelerating in Europe and North America due to broader consumer trust in halal standards. The market is further supported by increased transparency enabled through harmonized certification systems and labeling practices, which reinforce product credibility among both traditional and non-traditional consumers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $425.5 Million |

| Forecast Value | $762 Million |

| CAGR | 6% |

The animal-based ingredients segment reached USD 203.1 million in 2025. This category includes materials that require strict oversight of sourcing practices, traceability, and quality assurance systems to align with international halal regulations. At the same time, demand for plant-origin ingredients continues to rise, driven by changing dietary preferences and the growing appeal of plant-forward nutrition. Ingredients produced through microbial and fermentation-based methods are also gaining attention, with manufacturers ensuring compliance through certified production environments and controlled processes.

The offline distribution segment generated USD 337.5 million in 2025. The market structure includes both physical and digital sales platforms; however, in-person purchasing remains dominant due to long-standing procurement habits among industrial buyers. Physical retail and business-to-business channels continue to play a central role, as buyers prioritize direct verification of certification, particularly when sourcing large volumes.

North America Halal Ingredients Market is expected to reach USD 80.1 million by 2035. Growth in this region is linked to increasing cultural diversity and greater public understanding of halal standards. Food retailers and service providers are expanding halal-certified portfolios, while consumers show heightened interest in ethically sourced and plant-focused formulations. Urban centers remain the primary demand hubs, supported by improved labeling practices and dedicated halal product placements in retail environments.

Key companies active in the Global Halal Ingredients Market include Cargill Inc., ADM, DSM-Firmenich, BASF SE, Ingredion, Kerry Group, Ajinomoto, Corbion, Roquette, and Givaudan. Companies operating in the halal ingredients market are strengthening their market positions through strategic investments in certification, supply chain transparency, and portfolio diversification. Many players are prioritizing compliance management by aligning production facilities with globally recognized halal standards. Product innovation focused on clean-label, plant-based, and ethically sourced ingredients is being used to attract a wider consumer base. Firms are also expanding their geographic reach through partnerships with regional distributors and food manufacturers. Branding efforts centered on trust, traceability, and quality assurance are helping companies reinforce credibility, while digital tools are increasingly used to improve documentation, audit readiness, and customer engagement across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Source Origin

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for halal-compliant products

- 3.2.1.2 Increasing disposable incomes and urbanization in key markets

- 3.2.1.3 Growing health consciousness and preference for ethically sourced products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs associated with Halal certification and compliance

- 3.2.2.2 Complex supply chains that increase operational challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of blockchain and IoT for supply chain traceability

- 3.2.3.2 Automation in food processing and quality control for efficiency

- 3.2.3.3 Development of plant-based and lab-grown Halal-compliant alternatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Product type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Animal-derived ingredients

- 5.2.1 Meat

- 5.2.2 Dairy

- 5.2.3 Gelatin

- 5.2.4 Collagen

- 5.2.5 Enzymes

- 5.3 Plant-derived ingredients

- 5.3.1 Proteins

- 5.3.2 Grains

- 5.3.3 Oils

- 5.3.4 Extracts

- 5.4 Microbial/fermentation-derived

- 5.4.1 Enzymes

- 5.4.2 Cultures

- 5.5 Precision fermentation proteins

- 5.5.1 Synthetic/chemical

- 5.5.2 Synthetic additives

- 5.5.3 Flavors

- 5.5.4 Colors

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Source Origin, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Animal-based ingredients

- 6.3 Plant-based ingredients

- 6.4 Microbial/fermentation-derived ingredients

- 6.5 Synthetic/chemically synthesized ingredients

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.2.1 Meat and poultry products

- 7.2.2 Dairy and dairy alternatives

- 7.2.3 Bakery and confectionery

- 7.2.4 Beverages

- 7.2.5 Snacks and savory foods

- 7.2.6 Processed and ready meals

- 7.2.7 Condiments and sauces

- 7.2.8 Others

- 7.3 Pharmaceuticals

- 7.3.1 Gelatin capsules

- 7.3.2 Excipients

- 7.3.3 Active pharmaceutical ingredients (APIs)

- 7.3.4 Vitamins and supplements

- 7.3.5 Others

- 7.4 Cosmetics & personal care

- 7.4.1 Skincare and body care

- 7.4.2 Haircare

- 7.4.3 Oral care

- 7.4.4 Fragrances and perfumes

- 7.4.5 Color cosmetics (makeup)

- 7.4.6 Others

- 7.5 Animal feed & pet food

- 7.5.1 Livestock feed (cattle, sheep, goat)

- 7.5.2 Poultry feed (chicken, turkey)

- 7.5.3 Aquaculture feed (fish, shrimp)

- 7.5.4 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Offline distribution

- 8.2.1 Hypermarkets and supermarkets

- 8.2.2 Convenience stores

- 8.2.3 Specialty halal stores

- 8.2.4 Traditional markets and bazaars

- 8.2.5 Foodservice

- 8.2.6 Others

- 8.3 Online distribution

- 8.3.1 E-commerce marketplaces

- 8.3.2 Direct-to-consumer (DTC) brand websites

- 8.3.3 Online grocery delivery

- 8.3.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 ADM

- 10.2 Ajinomoto

- 10.3 BASF SE

- 10.4 Cargill Inc.

- 10.5 Corbion

- 10.6 DSM-Firmenich

- 10.7 Givaudan

- 10.8 Ingredion

- 10.9 Kerry Group

- 10.10 Roquette