|

市場調查報告書

商品編碼

1936672

血液及血液成分市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Blood and Blood Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

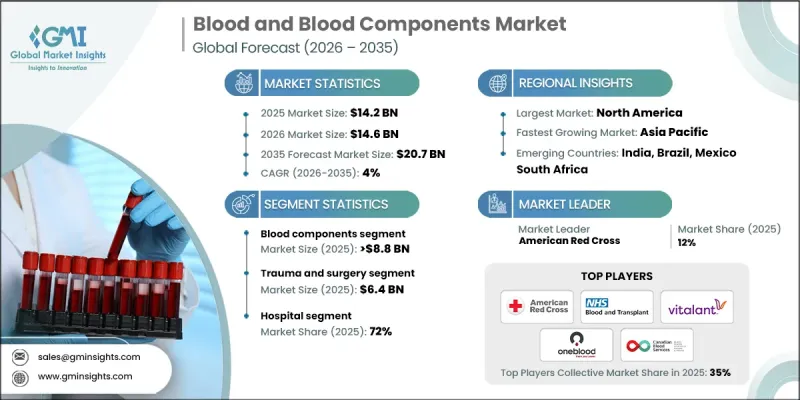

全球血液和血液成分市場預計到 2025 年將達到 142 億美元,到 2035 年將達到 207 億美元,年複合成長率為 4%。

由於全球外科手術數量不斷增加、慢性疾病盛行率上升以及血漿療法在各種臨床環境中的廣泛應用,市場正經歷穩定成長。血液採集機構持續進行的宣傳活動和捐血宣傳活動,為穩定的血液供應提供了保障。血液和血液成分在現代醫療保健系統中仍然至關重要,確保了輸血治療所需的紅血球、血漿和血小板的持續供應。這些產品廣泛應用於包括急救、外科手術、腫瘤治療以及血液相關疾病的長期管理等許多領域。市場在嚴格的品質和安全標準下運作,以確保產品完整性和病人安全。血液採集方法、成分分離、檢測、儲存和物流方面的持續創新,提高了效率,並滿足了全球醫療保健系統日益成長的需求。該行業不斷發展,重點關注可靠性、可追溯性和合規性。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 142億美元 |

| 預測金額 | 207億美元 |

| 複合年成長率 | 4% |

預計到2025年,血液成分業務的收入將達到88億美元。該業務包括紅血球、血漿、血小板和白血球,每種成分都發揮特定的治療作用。由於紅血球在恢復低血紅蛋白患者的氧氣輸送方面發揮著至關重要的作用,因此其需求量仍然很高。全球血液相關疾病的負擔持續沉重,推動了基於血液成分治療方法的長期應用,使該業務成為核心收入來源。

預計2025年,醫院將佔血液及血液成分消費總量的72%。醫療機構在急診護理、外科手術、腫瘤治療和慢性病治療中發揮核心作用,因此仍是血液及血液成分的主要消費群體。複雜醫療干預的增加、創傷病例的增多以及先進治療通訊協定的廣泛應用,共同推動了醫院對血液及血液成分的持續穩定需求,鞏固了其作為終端用戶的主導地位。

預計2025年,北美血液及血液成分市佔率將達到39.8%。該地區受益於完善的醫療保健基礎設施、較高的捐血參與率以及輸血療法在各種臨床應用中的積極使用。先進的醫療實踐、高效的血液管理系統和健全的製度框架持續鞏固該地區的市場主導地位。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 全球手術數量不斷增加。

- 患有慢性疾病(包括癌症)的人數不斷增加。

- 擴大血漿療法在治療各種運動傷害、整形手術和整形外科手術的應用

- 多個血液組織宣傳活動了多次捐血活動

- 產業面臨的潛在風險與挑戰:

- 血液成分的保存期限短

- 與捐血相關的輸血傳染感染(TTI)

- 市場機遇

- 個人化和標靶治療的發展

- 整合數位化解決方案

- 促進要素

- 成長潛力分析

- 監管環境

- 技術進步

- 當前技術趨勢

- 新興技術

- 供應鏈分析

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 合作夥伴關係和合資企業

- 新產品發布

- 擴張計劃

第5章 2022-2035年按產品分類的市場估算與預測

- 全血

- 血液成分

- 紅血球

- 血小板

- 電漿

- 白血球

第6章 按應用領域分類的市場估算與預測,2022-2035年

- 創傷及外科手術

- 血液疾病

- 貧血

- 出血性疾病

- 血友病

- 血管性血友病

- 其他血液疾病

- 癌症治療

- 其他用途

7. 依最終用途分類的市場估計與預測,2022-2035 年

- 醫院

- 門診手術中心

- 其他用途

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- American Red Cross

- America's Blood Centers

- Associazione Volontari Italiani del Sangue(AVIS)

- Bloodworks Northwest

- Canada Blood Services

- Carter BloodCare

- ImpactLife

- Indian Red Cross Society

- NHS Blood and Transplant(NHSBT)

- Northern Ireland Blood Transfusion Service

- OneBlood

- Scottish National Blood Transfusion Service(NHS National Services Scotland)

- Versiti

- Vitalant

- Welsh blood service

The Global Blood and Blood Components Market was valued at USD 14.2 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 20.7 billion by 2035.

The market is experiencing steady growth due to the rising number of surgical procedures worldwide, the increasing prevalence of long-term medical conditions, and the expanding use of plasma-based therapies across a wide range of clinical treatments. Continuous awareness initiatives and donation drives conducted by blood collection organizations are supporting a stable supply pipeline. Blood and blood components remain essential to modern healthcare systems, as they ensure uninterrupted access to red blood cells, plasma, and platelets required for transfusion-based therapies. These products are widely used across emergency care, surgical interventions, oncology treatments, and the long-term management of blood-related disorders. The market operates under strict quality and safety frameworks to maintain product integrity and patient safety. Ongoing innovation in blood collection methods, component separation, testing, storage, and logistics is improving efficiency and meeting the rising demands of global healthcare systems. The industry continues to evolve with a strong focus on reliability, traceability, and regulatory compliance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.2 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 4% |

The blood components segment generated USD 8.8 billion in 2025. This segment includes red blood cells, plasma, platelets, and white blood cells, each fulfilling specialized therapeutic roles. Red blood cells remain in high demand due to their essential function in restoring oxygen delivery in patients with reduced hemoglobin levels. The global burden of blood-related conditions continues to support sustained utilization of component-based therapies, making this segment a core revenue contributor.

The hospitals segment accounted for 72% share in 2025. Healthcare facilities remain the primary consumers of blood and blood components due to their central role in managing emergency care, surgical procedures, oncology services, and chronic disease treatment. The growing volume of complex medical interventions, combined with increasing trauma cases and advanced treatment protocols, continues to drive consistent demand from hospitals, reinforcing their dominance as end users.

North America Blood and Blood Components Market held a 39.8% share in 2025. The region benefits from a well-established healthcare infrastructure, strong donor participation, and high utilization of transfusion therapies across multiple clinical applications. Advanced medical practices, efficient blood management systems, and strong institutional frameworks continue to support regional market leadership.

Key organizations operating in the Global Blood and Blood Components Market include Vitalant, Canada Blood Services, American Red Cross, OneBlood, NHS Blood and Transplant, ImpactLife, America's Blood Centers, Versiti, Bloodworks Northwest, Carter BloodCare, Indian Red Cross Society, Associazione Volontari Italiani del Sangue, Northern Ireland Blood Transfusion Service, Scottish National Blood Transfusion Service, and the Welsh Blood Service. Companies in the blood and blood components market are strengthening their market position by expanding donor networks, improving collection efficiency, and investing in advanced processing and storage technologies. Organizations are focusing on digital donor engagement platforms to improve donor retention and streamline appointment scheduling. Strategic collaborations with hospitals and healthcare systems are enhancing supply reliability and demand forecasting.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing volume of surgeries globally

- 3.2.1.2 Rising number of people suffering from chronic conditions including cancer

- 3.2.1.3 Growing popularity of plasma therapy to treat various sport injuries, cosmetic as well as orthopedic procedures

- 3.2.1.4 Several blood donation campaigns undertaken by various blood organizations

- 3.2.2 Industry Pitfalls and Challenges:

- 3.2.2.1 Short shelf life of blood components

- 3.2.2.2 Transfusion transmitted infection (TTI) related to donated blood

- 3.2.3 Market Opportunities

- 3.2.3.1 Growth in personalized and targeted therapies

- 3.2.3.2 Integration of digital solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Whole blood

- 5.3 Blood components

- 5.3.1 Red blood cells

- 5.3.2 Platelets

- 5.3.3 Plasma

- 5.3.4 White blood cells

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Trauma and Surgery

- 6.3 Blood disorders

- 6.3.1 Anaemia

- 6.3.2 Bleeding disorders

- 6.3.2.1 Hemophilia

- 6.3.2.2 Von willebrand disease

- 6.3.3 Other blood disorders

- 6.4 Cancer treatment

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 American Red Cross

- 9.2 America's Blood Centers

- 9.3 Associazione Volontari Italiani del Sangue (AVIS)

- 9.4 Bloodworks Northwest

- 9.5 Canada Blood Services

- 9.6 Carter BloodCare

- 9.7 ImpactLife

- 9.8 Indian Red Cross Society

- 9.9 NHS Blood and Transplant (NHSBT)

- 9.10 Northern Ireland Blood Transfusion Service

- 9.11 OneBlood

- 9.12 Scottish National Blood Transfusion Service (NHS National Services Scotland)

- 9.13 Versiti

- 9.14 Vitalant

- 9.15 Welsh blood service