|

市場調查報告書

商品編碼

1936662

高位脛骨截骨鋼板市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)High Tibial Osteotomy Plates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

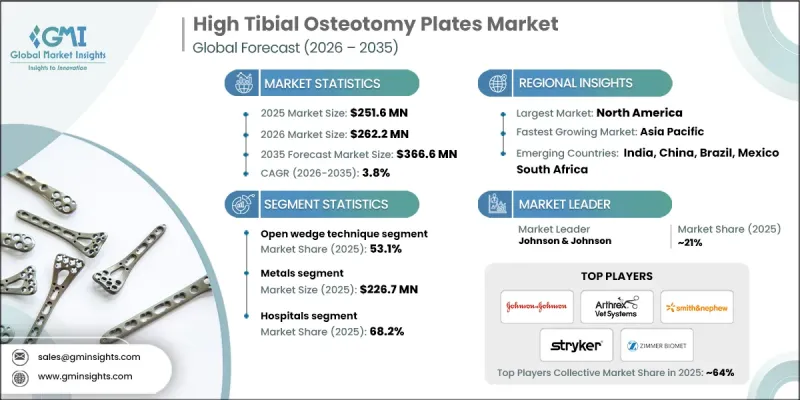

全球高位脛骨截骨板市場預計到 2025 年將達到 2.516 億美元,預計到 2035 年將達到 3.666 億美元,年複合成長率為 3.8%。

這種穩定成長主要得益於人們越來越傾向於選擇保留關節的手術方式而非全膝關節置換術,以及鋼板設計、固定技術和手術技巧的不斷創新。此外,隨著年輕且活躍人群中膝骨關節炎發病率的上升,患者和外科醫生都在尋求能夠保留關節功能、延緩或避免全膝關節置換術的替代方案,這也推動了市場需求。高位脛骨截骨術(HTO)鋼板是一種專門用於在矯正性截骨術後穩定脛骨的整形外科器械,確保在恢復期間實現最佳的骨骼對位和負荷分佈。改進的解剖形狀、低輪廓設計和鎖定螺絲系統提高了穩定性,減少了癒合併發症,並增強了外科醫生的信心。隨著技術的進步,現代HTO鋼板因其能夠促進康復、提供良好的長期關節功能,同時最大限度地降低骨不連、植入失效和術後畸形等風險,而得到更廣泛的認可。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 3.666億美元 |

| 預測金額 | 3.666億美元 |

| 複合年成長率 | 3.8% |

2025年,開放式楔形截骨術市佔率達到53.1%,這主要得益於其相較於其他技術的優勢,例如手術柔軟性、肢體對線矯正精準以及神經血管損傷風險低。該技術能夠精確調整脛骨角度,使外科醫生能夠實現理想的力學對線,避免過度矯正或矯正不足。這種精準性能夠改善術後效果,促進功能恢復,使其成為現代整形外科實踐中優於閉合式楔形截骨術的首選技術。

預計到2025年,金屬骨科鋼板市場規模將達到2.267億美元,2026年至2035年的複合年成長率(CAGR)為4%。金屬高位脛骨截骨(HTO)鋼板主要由鈦或不銹鋼製成,具有卓越的強度和剛度,即使在早期負重階段也能確保穩定的固定。這些鋼板與現代鎖定螺絲系統相容,可提供角度穩定性和長期矯正效果,從而實現安全的早期活動和加速康復。由於金屬鋼板具有機械可靠性、耐用性以及與先進手術技術的兼容性,外科醫生通常更傾向於為活動量大的患者選擇金屬鋼板。

預計到2025年,北美高位脛骨截骨板市場將佔45%的佔有率。膝骨關節炎盛行率的不斷上升,尤其是在中老年人群中,加上膝蓋內翻畸形和內側間室退化的發生率不斷增加,推動了該地區對保膝手術的需求。醫院和整形外科專家擴大採用具有解剖學形狀和鎖定螺絲設計的先進高位脛骨截骨板,作為早期全膝關節置換術的替代方案。先進的醫療基礎設施和對創新整形外科解決方案的高度認知,進一步推動了該地區市場的擴張。

目錄

第1章調查方法

- 研究途徑

- 品質保證

- GMI人工智慧政策與資料完整性承諾

- 資訊來源完整性通訊協定

- GMI人工智慧政策與資料完整性承諾

- 調查可追溯性和可靠性評分

- 勘測和步道組成部分

- 評分組成部分

- 數據收集

- 主要資訊的部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估計值與計算

- 兩種方法的基準年計算均適用。

- 預測模型

- 量化市場影響分析

- 生長參數對預測值的數學影響

- 量化市場影響分析

- 研究透明度附錄

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 膝骨關節炎和肌肉骨骼疾病的盛行率不斷上升

- 運動相關傷害和膝關節畸形發生率增加

- 對保關節手術的需求日益成長

- 植入設計與材料的技術進步

- 產業潛在風險與挑戰

- 昂貴的高位脛骨截骨術鋼板和手術費用

- 潛在的手術風險和併發症

- 市場機遇

- 採用微創手術技術

- 個性化和病人特異性植入的發展

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 價值鏈分析

- Start-Ups場景

- 波特五力分析

- PESTEL 分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 公司市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按技術分類的市場估算與預測,2022-2035年

- 開放楔形截骨術

- 閉合楔形截骨術

- 漸進式骨融合組織牽引法

- 穹頂法

- 人字形截骨術

第6章 按材料分類的市場估算與預測,2022-2035年

- 金屬

- 鈦

- 不銹鋼

- 聚合物

7. 依最終用途分類的市場估計與預測,2022-2035 年

- 醫院

- 門診手術中心

- 其他最終用戶

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Amplitude Surgical

- Arthrex

- Auxein

- B. BRAUN

- Hankil Tech Medical

- Intercus

- Johnson &Johnson

- Medacta International

- Miraclus

- Nebula Surgical

- Newclip Technics

- Science and Bio Materials(SBM)

- Smith+Nephew

- Stryker

- ZIMMER BIOMET

The Global High Tibial Osteotomy Plates Market was valued at USD 251.6 million in 2025 and is estimated to grow at a CAGR of 3.8% to reach USD 366.6 million by 2035.

The steady growth is driven by the increasing preference for joint-preserving surgeries over total knee replacements, alongside ongoing innovations in plate design, fixation technologies, and surgical techniques. Rising incidences of knee osteoarthritis in younger and more active populations are also fueling demand, as patients and surgeons seek alternatives that maintain joint functionality and delay or avoid full knee replacement. HTO plates are specialized orthopedic devices designed to stabilize the tibia following corrective osteotomy procedures, ensuring optimal bone alignment and load distribution during recovery. Improved anatomical contours, low-profile designs, and locking screw systems have enhanced stability, reduced healing complications, and increased surgeon confidence. As technology continues to advance, modern HTO plates are gaining wider acceptance due to their ability to minimize risks like non-union, implant failure, and postoperative misalignment, while promoting faster recovery and better long-term joint outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $366.6 Million |

| Forecast Value | $366.6 Million |

| CAGR | 3.8% |

In 2025, the open wedge technique segment held a 53.1% share, owing to its surgical flexibility, precision in limb alignment correction, and reduced risk of neurovascular injuries compared to alternative approaches. This method allows exact angular adjustment of the tibia, enabling surgeons to achieve the desired mechanical alignment and avoid over- or under-correction. Such precision improves postoperative outcomes and accelerates functional recovery, making it the preferred technique over closed wedge methods in modern orthopedic practices.

The metals segment generated USD 226.7 million in 2025 and is expected to grow at a CAGR of 4% during 2026-2035. Metal HTO plates, typically made from titanium or stainless steel, provide superior strength and rigidity, ensuring stable fixation even during early weight-bearing phases. These plates support modern locking screw systems, delivering angular stability and long-term correction, which enables safe early mobilization and enhanced recovery. Surgeons often favor metal plates for active patients due to their mechanical reliability, durability, and compatibility with advanced surgical techniques.

North America High Tibial Osteotomy Plates Market accounted for 45% share in 2025. The region's growing prevalence of knee osteoarthritis, particularly among middle-aged and elderly populations, combined with increasing rates of varus deformities and medial compartment degeneration, has amplified the demand for joint-preserving procedures. Hospitals and orthopedic specialists are progressively adopting advanced HTO plates with anatomical contouring and locking screw designs to provide alternatives to early total knee replacement. The presence of sophisticated healthcare infrastructure and high awareness of innovative orthopedic solutions further drives market expansion in this region.

Key companies in the Global High Tibial Osteotomy Plates Market include Arthrex, Smith+Nephew, Medacta International, Stryker, ZIMMER BIOMET, Amplitude Surgical, Johnson & Johnson, B. BRAUN, Intercus, Newclip Technics, Hankil Tech Medical, Science and Bio Materials (SBM), Nebula Surgical, Auxein, and Miraclus. Companies in the High Tibial Osteotomy Plates Market strengthen their position by focusing on research and development to enhance plate design, incorporating advanced materials, anatomical contouring, and locking screw systems. Strategic collaborations with orthopedic hospitals and surgical centers enable demonstration of efficacy and foster surgeon trust. Manufacturers also invest in training programs and workshops to educate surgeons on modern osteotomy techniques and device usage.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technique trends

- 2.2.3 Material trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of knee osteoarthritis and musculoskeletal disorders

- 3.2.1.2 Increasing incidence of sports-related injuries and knee deformities

- 3.2.1.3 Growing demand for joint-preserving surgical procedures

- 3.2.1.4 Technological advancements in implant design and materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of HTO plates and procedures

- 3.2.2.2 Potential surgical risks and complications

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of minimally invasive surgical techniques

- 3.2.3.2 Growth in personalized and patient-specific implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Value chain analysis

- 3.8 Start-up scenarios

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technique, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Open wedge technique

- 5.3 Closed wedge technique

- 5.4 Progressive callus distraction

- 5.5 Dome technique

- 5.6 Chevron osteotomy

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Metals

- 6.2.1 Titanium

- 6.2.2 Stainless steel

- 6.3 Polymers

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amplitude Surgical

- 9.2 Arthrex

- 9.3 Auxein

- 9.4 B. BRAUN

- 9.5 Hankil Tech Medical

- 9.6 Intercus

- 9.7 Johnson & Johnson

- 9.8 Medacta International

- 9.9 Miraclus

- 9.10 Nebula Surgical

- 9.11 Newclip Technics

- 9.12 Science and Bio Materials (SBM)

- 9.13 Smith+Nephew

- 9.14 Stryker

- 9.15 ZIMMER BIOMET