|

市場調查報告書

商品編碼

1936657

全球氫能市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Global Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

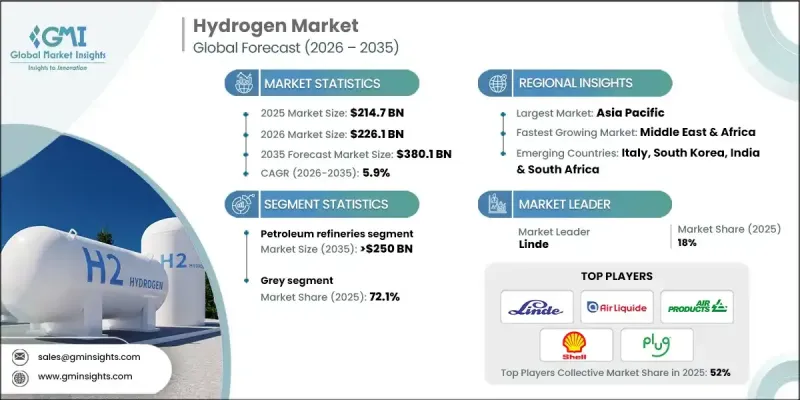

預計到 2025 年,全球氫能市場規模將達到 2,147 億美元,並以 5.9% 的複合年成長率成長,到 2035 年達到 3,801 億美元。

市場擴張的驅動力在於氫氣生產正從石化燃料基到低碳路徑轉型,而這項轉型又受到氣候變遷計劃、技術進步和政策框架演變的推動。氫氣在能源密集產業和化學製造(包括氨和甲醇生產)的日益普及,正推動著強勁的成長動能。企業正日益關注藍氫解決方案,即將天然氣與捕碳封存(CCS)技術相結合,以最大限度地減少排放。同時,綠氫的應用也在加速推進,以符合脫碳目標。低碳氫化合物生產成本的下降,加上政府的支持措施和清潔能源政策,正在增強市場動態。中國在全球產能中佔據主導地位,約佔電解裝機量的三分之二和總產量的60%。國內年產量超過20吉瓦,超過全球總需求。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 2147億美元 |

| 預測金額 | 3801億美元 |

| 複合年成長率 | 5.9% |

2025年,由於對傳統煉油和原油消費的持續依賴,灰氫市場將佔據72.1%的佔有率。然而,蒸汽甲烷重整的高碳排放強度正在加速綠氫的轉型。減少溫室氣體排放和實現永續性目標的壓力促使各行業尋求低排放的氫能替代方案,從而創造了新的成長機會。

預計到2035年,石油煉製產業的規模將達到2,500億美元,主要得益於氫氣在脫硫製程中日益廣泛的應用。氫氣對於降低燃料中的硫含量至關重要,煉油廠正逐步採用綠色氫氣以實現淨零排放目標。這一持續的轉型正在推動整體市場成長。

在政府主導和清潔能源政策的支持下,預計到2025年,北美氫能市場將佔據12.1%的市場佔有率。加州等地區在燃料電池汽車的普及和基礎設施建設方面主導,而加拿大正在成為全球清潔氫能的主要出口國。各地區對脫碳、能源轉型和技術創新的堅定承諾預計將推動氫能的普及應用。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系統

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 成長潛力分析

- 價格趨勢分析

- 按產能

- 按地區

- 成本結構分析

- 波特五力分析

- PESTEL 分析

- 新的機會與趨勢

- 數位化和物聯網整合

- 拓展新興市場

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 戰略儀錶板

- 策略舉措

- 創新與科技趨勢

第5章 依類型分類的市場規模及預測(2023-2035年)

- 灰色的

- 藍色的

- 綠色的

第6章 依應用領域分類的市場規模及預測(2023-2035年)

- 煉油廠

- 化學

- 其他

第7章 2023-2035年各地區市場規模及預測

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 伊朗

- 阿拉伯聯合大公國

- 南非

- 卡達

- 科威特

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第8章 公司簡介

- Air Liquide

- Air Products &Chemicals

- Ally Hi Tech

- Ballard Power Systems

- Caloric

- Claind

- Cummins

- ENGIE

- HyGear

- Infinite Green Energy

- Iwatani Corporation

- Linde

- Mahler AGS

- Mcphy Energy

- Messer

- Nel ASA

- Nuvera Fuel Cells

- Plug Power

- Resonac Holdings Corporation

- Taiyo Nippon Sanso Corporation

- Teledyne Technologies Incorporated

- Xebec Adsorption

The Global Hydrogen Market was valued at USD 214.7 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 380.1 billion by 2035.

Market expansion is driven by the ongoing transition from fossil-fuel-based hydrogen production to low-carbon pathways, fueled by climate commitments, technological advancements, and evolving policy frameworks. Increased adoption of hydrogen in energy-intensive industries and in chemical manufacturing, including ammonia and methanol production, is creating strong growth momentum. Companies are increasingly focusing on blue hydrogen solutions, combining natural gas with carbon capture and storage (CCS) to minimize emissions, while green hydrogen deployment is accelerating in line with decarbonization goals. Falling production costs for low-carbon hydrogen, combined with supportive government incentives and clean energy mandates, are strengthening market dynamics. China dominates global capacity, accounting for nearly two-thirds of electrolyzer installations and around 60% of production, with domestic manufacturing exceeding 20 GW annually, surpassing total global demand.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $214.7 Billion |

| Forecast Value | $380.1 Billion |

| CAGR | 5.9% |

The grey hydrogen segment accounted for 72.1% share in 2025, due to continued reliance on conventional refining and crude oil consumption. However, the high carbon intensity of steam methane reforming is accelerating the shift toward green hydrogen. Pressure to reduce greenhouse gas emissions and meet sustainability targets is prompting industries to explore low-emission hydrogen alternatives, creating new growth opportunities.

The petroleum refinery sector is expected to reach USD 250 billion by 2035, driven by increasing integration of hydrogen in desulfurization processes. Hydrogen remains essential for reducing sulfur content in fuels, and refineries are progressively adopting green hydrogen to align with net-zero ambitions. This ongoing transformation is supporting broader market growth.

North America Hydrogen Market held 12.1% share in 2025, supported by government-led initiatives and clean energy policies. Regions like California are spearheading fuel cell vehicle deployment and infrastructure expansion, while Canada is positioning itself as a major clean hydrogen exporter to global markets. Strong regional commitments to decarbonization, energy transition, and technological innovation are expected to stimulate hydrogen adoption.

Key players in the Global Hydrogen Market include Air Liquide, Air Products & Chemicals, Ally Hi Tech, Ballard Power Systems, Caloric, Claind, Cummins, ENGIE, HyGear, Infinite Green Energy, Iwatani Corporation, Linde, Mahler AGS, McPhy Energy, Messer, Nel ASA, Nuvera Fuel Cells, Plug Power, Resonac Holdings Corporation, Taiyo Nippon Sanso Corporation, Teledyne Technologies Incorporated, and Xebec Adsorption. Companies are strengthening their market presence by investing in research and development to improve electrolyzer efficiency, scaling low-carbon hydrogen production, and forming strategic partnerships across energy and industrial sectors. Firms are focusing on developing both green and blue hydrogen solutions to meet emerging regulatory requirements and sustainability targets. Additionally, market participants are expanding global manufacturing footprints, building strategic supply chains, and enhancing technology portfolios to support fuel cell applications, industrial usage, and export opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.1.2 Mathematical impact of growth parameters on forecast

- 1.3.1 Key trends for market estimates

- 1.4 Primary research & validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2023 - 2035

- 2.2 Business trends

- 2.3 Type trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Price trend analysis

- 3.5.1 By capacity

- 3.5.2 By region

- 3.6 Cost structure analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.9 Emerging opportunities and trends

- 3.9.1 Digitization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2023 - 2035 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Grey

- 5.3 Blue

- 5.4 Green

Chapter 6 Market Size and Forecast, By Application, 2023 - 2035 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Petroleum refinery

- 6.3 Chemical

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2023 - 2035 (USD Billion & MT)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Netherlands

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 Iran

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.5.5 Qatar

- 7.5.6 Kuwait

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Air Liquide

- 8.2 Air Products & Chemicals

- 8.3 Ally Hi Tech

- 8.4 Ballard Power Systems

- 8.5 Caloric

- 8.6 Claind

- 8.7 Cummins

- 8.8 ENGIE

- 8.9 HyGear

- 8.10 Infinite Green Energy

- 8.11 Iwatani Corporation

- 8.12 Linde

- 8.13 Mahler AGS

- 8.14 Mcphy Energy

- 8.15 Messer

- 8.16 Nel ASA

- 8.17 Nuvera Fuel Cells

- 8.18 Plug Power

- 8.19 Resonac Holdings Corporation

- 8.20 Taiyo Nippon Sanso Corporation

- 8.21 Teledyne Technologies Incorporated

- 8.22 Xebec Adsorption

2026年全球氫氣工廠市場報告

2026年全球氫氣工廠市場報告 氫能技術測試、檢驗和認證市場:按服務類型、技術、最終用戶和應用分類-2026-2032年全球市場預測

氫能技術測試、檢驗和認證市場:按服務類型、技術、最終用戶和應用分類-2026-2032年全球市場預測 半導體用高純度氫氣生產市場分析及預測(至2035年):類型、產品、服務、技術、應用、材料類型、製程、最終用戶、功能、安裝類型

半導體用高純度氫氣生產市場分析及預測(至2035年):類型、產品、服務、技術、應用、材料類型、製程、最終用戶、功能、安裝類型 全球氫氣市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球氫氣發生器市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球氫氣鋼瓶(4型)市場規模、佔有率、趨勢與成長分析報告:2026-2034年全球綠松石氫市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球氫氣市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球氫氣發生器市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球氫氣鋼瓶(4型)市場規模、佔有率、趨勢與成長分析報告:2026-2034年全球綠松石氫市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球氫能基礎設施市場:預測(至2034年)-以基礎設施類型、氫能類型、計劃規模、所有權/經營模式、技術、最終用戶和地區進行分析2026年全球pH調節劑市場報告2026年全球氫能市場報告

全球氫能基礎設施市場:預測(至2034年)-以基礎設施類型、氫能類型、計劃規模、所有權/經營模式、技術、最終用戶和地區進行分析2026年全球pH調節劑市場報告2026年全球氫能市場報告