|

市場調查報告書

商品編碼

1936647

電動出行設備市場機會、成長要素、產業趨勢分析及2026年至2035年預測Powered Mobility Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

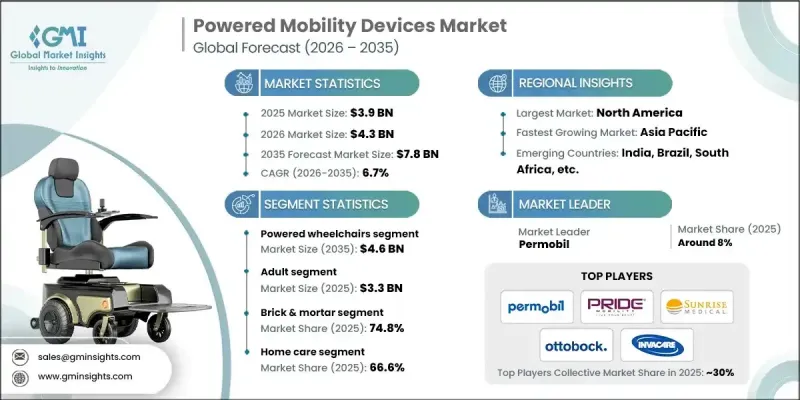

全球電動旅遊設備市場預計到 2025 年將達到 39 億美元,到 2035 年將達到 78 億美元,年複合成長率為 6.7%。

市場成長的促進因素包括行動不便疾病的日益增多以及老年人口的不斷擴大,老年人越來越依賴電動代步設備來維持獨立的日常生活。與基礎型代步工具不同,電動代步設備正迅速邁向智慧醫療設備領域,製造商不斷整合長續航電池系統、高效率馬達、符合人體工學的座椅系統以及可程式設計控制設備等功能,從而提升舒適度並減輕看護者的負擔。居家照護的普及也推動了市場的發展。患者及其家人越來越傾向於選擇實用且便利的代步解決方案,幫助老年人繼續在熟悉的環境中生活,減少往返養老機構的次數,並確保室內外活動的安全性。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 39億美元 |

| 預測金額 | 78億美元 |

| 複合年成長率 | 6.7% |

從產品和市場接受度來看,市場受益於各種嚴重程度的需求,從需要持續電力支援的使用者到尋求輔助設備的使用者。與關節炎、中風後遺症、脊髓損傷和神經退化性疾病通常需要長期可靠的行動輔助,而非短期復健支持。技術進步也是推動需求成長的因素。現代設備越來越注重輕量化材料、更高的操控性和安全性,例如智慧煞車、座椅個人化調節、防跌倒和穩定性控制,從而推動電動代步設備不僅在醫療機構中,而且在日常生活中廣泛應用。

預計到2025年,電動輪椅市場規模將達到46億美元。對於行動嚴重受限或進行性行動能力的使用者而言,電動輪椅仍然是他們的首選解決方案。這些用戶需要先進的操控功能、強大的姿勢支撐以及在室內外環境中可靠的性能。隨著照護模式逐漸轉向家庭,舒適性、可靠性和個人化與臨床規格同等重要,電動輪椅產品在驅動機制、座椅模組和安全系統等方面的差異化程度日益提高,並受到越來越多的關注。

到2025年,居家照護市佔率將達到66.6%,這主要得益於老年人傾向於留在熟悉的住宅環境中、慢性病盛行率不斷上升,以及住宅生活便利性(對日常生活、安全和獨立性至關重要)的需求。此外,設備易用性的提升也推動了居家照護需求的成長,例如設備面積小巧、室內轉彎半徑更小、操作智慧以及充電便利等。同時,送貨上門、安裝和維護等服務模式也有助於減少老年人和看護者使用設備的障礙,為他們提供輕鬆便捷的使用體驗。

預計到2025年,北美電動出行設備市佔率將達到41.3%,主要得益於更完善的醫療基礎設施、更高的行動障礙疾病診斷和治療率,以及相對良好的報銷途徑和成熟的復健/居家照護體系。此外,該地區市場實力的增強也得益於技術先進設備的快速普及,這些設備強調安全性、互聯性和舒適性。醫療專業人員和消費者都非常重視這些特性,他們期望這些設備能夠實際改善日常生活功能和生活品質。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 神經系統疾病呈上升趨勢

- 動力移動產品的技術進步

- 老年人口比例不斷增加

- 全球殘障人數呈上升趨勢

- 產業潛在風險與挑戰

- 電動輪椅高成本

- 嚴格的法規結構

- 機會

- 專注於輕量折疊式電動輪椅

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價值鏈分析

- 救贖方案

- 消費行為與趨勢

- 2025年產品類型價格分析

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未來市場趨勢

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 公司市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 電動輪椅

- 後輪驅動輪椅

- 中輪驅動輪椅

- 前輪驅動輪椅

- 組合式驅動輪椅

- 電動代步Scooter

- 三輪行動裝置

- 四輪行動裝置

- 動力附加元件或輔助推進裝置

第6章 依病患類型分類的市場估計與預測,2022-2035年

- 成人版

- 兒童

7. 2022-2035年按分銷管道分類的市場估算與預測

- 實體店面

- 線上管道

第8章 依最終用途分類的市場估算與預測,2022-2035年

- 居家照護

- 復健中心

- 醫院

- 其他最終用戶

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Airwheel

- Callidai Motor Works

- Decon

- DriveDeVilbiss Healthcare

- Frido

- Golden Technologies

- INVACARE

- Karman Healthcare

- LEVO

- Merits Health Products

- MEYRA

- Ostrich Mobility Instruments

- Ottobock

- Permobil

- Pride Mobility

- Sunrise medical

The Global Powered Mobility Devices Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a 6.7% CAGR to reach USD 7.8 billion by 2035.

Market growth is supported by the rising prevalence of mobility-impairing conditions and the expanding elderly population that increasingly depends on powered assistance to preserve independence and day-to-day function. Unlike basic mobility aids, powered mobility devices are moving quickly into the smart medical device lane, as manufacturers integrate longer-range battery systems, more efficient motors, ergonomic seating systems, and programmable controls that improve comfort and reduce caregiver strain. The market's momentum is also reinforced by the broader shift toward home-based care, where patients and families prefer practical mobility solutions that support aging-in-place, reduce repeated facility visits, and enable safer indoor/outdoor navigation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 6.7% |

From a product and adoption perspective, the market is benefiting from demand across a wide severity range, from users who need full-time powered support to those who want a boost through add-on units. Clinical need is rising with chronic conditions such as arthritis, post-stroke impairments, spinal cord injuries, and neurodegenerative disorders, which often require long-term, reliable mobility assistance rather than short-duration rehabilitation support. Technology is also helping unlock demand: modern devices increasingly emphasize lightweight materials, better maneuverability, intelligent braking, improved seating customization, and safety-oriented features that reduce falls and enhance stability, making powered mobility devices more acceptable for everyday use, not only in institutional settings.

The powered wheelchairs segment generated USD 4.6 billion in 2025, as it remains the preferred solution for users with severe or progressive mobility limitations who need advanced control options, stronger postural support, and consistent performance across indoor and outdoor environments. These products are increasingly differentiated by drive options, seating modules, and safety systems, and they are gaining further traction as more care pathways move into the home, where comfort, reliability, and customization matter as much as clinical specifications.

The home care segment held 66.6% share in 2025, driven by aging-in-place preferences, growing chronic disease prevalence, and the need for convenient mobility within residential environments where daily routine, safety, and independence are the non-negotiables. Home care demand is also supported by improvements in device usability, such as compact footprints, improved turning radius for indoor navigation, smarter controls, and easier charging, while service models (delivery, installation, maintenance) help reduce barriers for older adults and caregivers who want a low-friction ownership experience.

North America Powered Mobility Devices Market held 41.3% share in 2025, anchored by stronger healthcare infrastructure, higher diagnosis and treatment rates for mobility-impairing conditions, and relatively better access through reimbursement pathways and established rehabilitation/home-care ecosystems. The region's market strength is also reinforced by faster adoption of technology-forward devices that emphasize safety, connectivity, and comfort features that resonate strongly with both clinicians and consumers who expect measurable improvements in daily functioning and quality of life.

Key players involved in the Global Powered Mobility Devices Market include Airwheel, Callidai Motor Works, Decon, Drive DeVilbiss Healthcare, Frido, Golden Technologies, INVACARE, Karman Healthcare, LEVO, Merits Health Products, MEYRA, Ostrich Mobility Instruments, Ottobock, Permobil, Pride Mobility, Sunrise Medical. Companies are strengthening their market foothold by accelerating product innovation, lightweight/foldable designs, improved battery performance, and smarter controls that enhance safety and comfort for home use. They are also widening access through multi-channel distribution, combining clinician-led brick-and-mortar fitting and service with faster-growing online models that improve reach into underserved geographies. To improve conversion and retention, leading players bundle devices with after-sales maintenance, training, and customization (seating, controls, accessories), reducing user anxiety and improving long-term satisfaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Patient trends

- 2.2.4 Distribution channel trends

- 2.2.5 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of neurological diseases

- 3.2.1.2 Technological advancements in powered mobility products

- 3.2.1.3 Rising percentage of geriatric population

- 3.2.1.4 Increasing prevalence of disabilities worldwide

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of powered wheelchairs

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Opportunities

- 3.2.3.1 Focus on lightweight and foldable electric wheelchairs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Reimbursement scenario

- 3.8 Consumer behavior and trends

- 3.9 Pricing analysis, by product type, 2025

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Powered wheelchairs

- 5.2.1 Rear-wheel drive wheelchairs

- 5.2.2 Mid-wheel drive wheelchairs

- 5.2.3 Front-wheel drive wheelchairs

- 5.2.4 Combination-drive wheelchairs

- 5.3 Power mobility scooters

- 5.3.1 3-wheel devices

- 5.3.2 4-wheel devices

- 5.4 Power add-on or propulsion-assist units

Chapter 6 Market Estimates and Forecast, By Patient, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Brick & mortar

- 7.3 Online channel

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Home care

- 8.3 Rehabilitation centers

- 8.4 Hospitals

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airwheel

- 10.2 Callidai Motor Works

- 10.3 Decon

- 10.4 DriveDeVilbiss Healthcare

- 10.5 Frido

- 10.6 Golden Technologies

- 10.7 INVACARE

- 10.8 Karman Healthcare

- 10.9 LEVO

- 10.10 Merits Health Products

- 10.11 MEYRA

- 10.12 Ostrich Mobility Instruments

- 10.13 Ottobock

- 10.14 Permobil

- 10.15 Pride Mobility

- 10.16 Sunrise medical

電動出行設備市場:2026-2032年全球市場預測(依設備類型、推進方式、應用、最終用戶及通路分類)

電動出行設備市場:2026-2032年全球市場預測(依設備類型、推進方式、應用、最終用戶及通路分類) 亞太地區「未來工廠」行動解決方案市場:按最終用戶產業、車輛類型、解決方案類型、部署模式和國家分類的分析和預測(2025-2035 年)

亞太地區「未來工廠」行動解決方案市場:按最終用戶產業、車輛類型、解決方案類型、部署模式和國家分類的分析和預測(2025-2035 年) 歐洲「未來工廠」移動性解決方案市場:按最終用戶產業、車輛類型、解決方案類型、部署模式和國家分類-分析與預測(2025-2035年)

歐洲「未來工廠」移動性解決方案市場:按最終用戶產業、車輛類型、解決方案類型、部署模式和國家分類-分析與預測(2025-2035年) 互聯出行安全與網路安全市場預測至2034年:依解決方案類型、車輛類型、部署模式、安全層級與區域分類的全球分析全自主互聯軌道運輸系統市場:系統元件、車輛類型、通訊技術、運行模式和應用分類-全球預測,2026-2032年

互聯出行安全與網路安全市場預測至2034年:依解決方案類型、車輛類型、部署模式、安全層級與區域分類的全球分析全自主互聯軌道運輸系統市場:系統元件、車輛類型、通訊技術、運行模式和應用分類-全球預測,2026-2032年 2026年全球電動出行設備市場報告2026年全球連網自動駕駛汽車市場報告

2026年全球電動出行設備市場報告2026年全球連網自動駕駛汽車市場報告 針對未來工廠的行動解決方案市場—全球及區域分析:依最終用戶產業、車輛類型、解決方案類型、部署模式和國家分類—分析與預測(2025-2035 年)

針對未來工廠的行動解決方案市場—全球及區域分析:依最終用戶產業、車輛類型、解決方案類型、部署模式和國家分類—分析與預測(2025-2035 年) 現場行動解決方案市場 - 2025 年至 2030 年預測

現場行動解決方案市場 - 2025 年至 2030 年預測 基於車輛的企業移動解決方案

基於車輛的企業移動解決方案