|

市場調查報告書

商品編碼

1936641

雷射切割機市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Laser Cutting Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

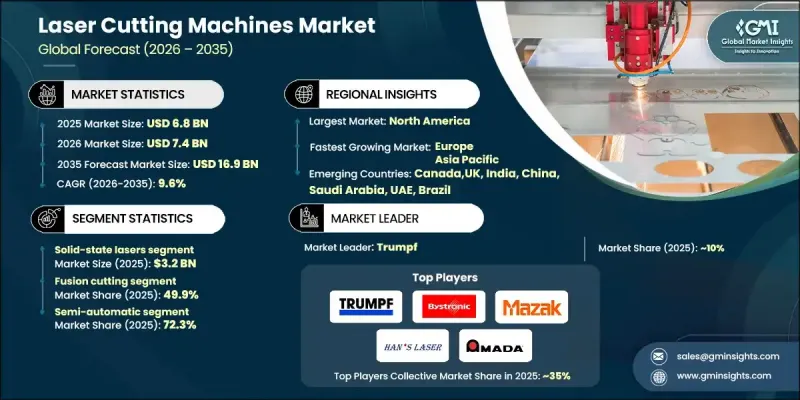

全球雷射切割機市場預計到 2025 年將達到 68 億美元,到 2035 年將達到 169 億美元,年複合成長率為 9.6%。

隨著各行業製造商積極採用自動化技術和工業4.0實踐,市場正在迅速擴張。雷射切割機正成為智慧工廠營運的核心,透過實現設備互聯、即時監控和進階分析,最佳化效率並透過預測性維護減少停機時間。這些機器能夠無縫整合到自動化工作流程中,提供微米級精度、高品質且後處理極少的精確切割。汽車、航太、電子和工業機械等行業的需求不斷成長,推動了市場成長。這些產業需要輕量化、複雜且精密的組裝,而傳統切割方法無法一致地實現這一目標。雷射系統能夠實現乾淨俐落的邊緣和卓越的幾何精度,從而提高生產效率並減少材料浪費,使其成為現代製造業不可或缺的工具。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 68億美元 |

| 預測金額 | 169億美元 |

| 複合年成長率 | 9.6% |

預計到2025年,固體雷射器市場規模將達到32億美元,並在2026年至2035年間以10%的複合年成長率成長。與傳統的氣體雷射系統相比,固體雷射器,尤其是光纖雷射和碟片雷射,因其卓越的光束品質、快速的切割速度、低營運成本和高能源效率而備受青睞。這些特性使其非常適合高精度工業應用和全自動生產線。固體雷射正被廣泛應用於金屬加工、汽車、航太和電子製造等眾多產業,協助數位轉型並提升工業效率。

預計到2025年,熔切市場佔有率將達到49.9%,並在2035年之前以9.9%的複合年成長率成長。熔切憑藉其多功能性、高速性、高精度、可加工多種金屬以及切割邊緣光滑(最大限度減少後處理)等優點,仍然是首選的加工方法。其高效性滿足了汽車、航太、電子和工業製造等行業對減少材料廢棄物、提高公差和簡化生產流程的需求。

美國雷射切割機市場預計到2025年將達到19億美元,2026年至2035年的複合年成長率(CAGR)為9.8%。汽車、航太、電子和金屬加工等產業對精密切割零件和複雜設計的強勁需求是推動市場成長的主要動力。雷射光源、軟體整合和自動化功能的持續技術創新,促進了雷射切割機的廣泛應用,並鼓勵製造商升級和擴展現有系統。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 自動化和工業4.0的日益普及

- 高精度加工的需求日益成長

- 向節能型光纖和固體雷射過渡

- 對減少材料廢棄物和提高生產力的需求

- 產業潛在風險與挑戰

- 高昂的營運和維護成本

- 材料限制與加工挑戰

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 透過技術

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按技術分類的市場估算與預測,2022-2035年

- 固體雷射

- 氣體雷射

- 半導體雷射

第6章 依製造流程分類的市場估算與預測,2022-2035年

- 熔切

- 火焰切割

- 熱昇華切割

第7章 依功能類型分類的市場估計與預測,2022-2035年

- 半自動

- 機器人技術

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 車

- 家用電子電器

- 國防和航太

- 工業的

- 其他(醫療、能源/電力等)

第9章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接銷售

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- Amada

- Bystronic

- Coherent

- Epilog Laser

- Han's Laser

- IPG Photonics

- Jenoptik

- LVD Company

- Mazak Optonics

- Mitsubishi Electric Corporation

- Prima Power

- Tanaka

- Trotec Laser

- Trumpf

- Universal Laser Systems

The Global Laser Cutting Machines Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 16.9 billion by 2035.

The market is experiencing rapid expansion as manufacturers across industries increasingly adopt automation technologies and Industry 4.0 practices. Laser cutting machines are becoming central to smart factory operations, enabling connected equipment, real-time monitoring, and advanced analytics to optimize efficiency and reduce downtime through predictive maintenance. These machines allow seamless integration into automated workflows, delivering precise, high-quality cuts with micron-level accuracy and minimal post-processing. Rising demand from automotive, aerospace, electronics, and industrial machinery sectors is driving growth, as these industries require lightweight, complex, and intricately assembled components that conventional cutting methods cannot achieve consistently. The ability of laser systems to produce clean edges and superior geometric accuracy enhances productivity while reducing material waste, making them indispensable for modern manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $16.9 Billion |

| CAGR | 9.6% |

The solid-state lasers segment generated USD 3.2 billion in 2025 and is expected to grow at a CAGR of 10% from 2026 to 2035. The solid-state segment, particularly fiber and disk lasers, is favored due to superior beam quality, faster cutting speeds, lower operating costs, and enhanced energy efficiency compared with traditional gas-based systems. These characteristics make them highly suitable for high-precision industrial operations and fully automated production lines. Solid-state lasers are increasingly adopted across metal fabrication, automotive, aerospace, and electronics manufacturing, supporting digital transformation and industrial efficiency.

The fusion cutting segment held a 49.9% share in 2025 and is anticipated to grow at a CAGR of 9.9% through 2035. Fusion cutting remains the preferred method due to its versatility, high speed, precision, and ability to handle a wide range of metals while producing smooth edges that require minimal post-processing. Its efficiency aligns with industry needs for reduced material waste, tighter tolerances, and streamlined production in automotive, aerospace, electronics, and industrial manufacturing sectors.

U.S. Laser Cutting Machines Market reached USD 1.9 billion in 2025 and is expected to grow at a CAGR of 9.8% between 2026 and 2035. Strong demand from industries requiring precision-cut components and complex designs, such as automotive, aerospace, electronics, and metal fabrication, is driving growth. Continuous technological advancements in laser sources, software integration, and automation capabilities support widespread adoption and encourage manufacturers to upgrade or expand their existing systems.

Key players in the Global Laser Cutting Machines Market include Bystronic, Coherent, Mitsubishi Electric Corporation, IPG Photonics, Trumpf, Amada, Jenoptik, LVD Company, Tanaka, Mazak Optonics, Trotec Laser, Universal Laser Systems, Prima Power, Han's Laser, and Epilog Laser. Companies in the laser cutting machines market are employing multiple strategies to expand their market presence and maintain a competitive advantage. They are investing heavily in R&D to develop faster, more energy-efficient, and higher-precision laser systems that cater to diverse industrial applications. Strategic collaborations with OEMs and industrial integrators are being used to strengthen distribution networks and ensure seamless integration into smart factories. Manufacturers are expanding production capacity, introducing fiber and hybrid laser technologies, and enhancing software and automation compatibility to attract high-end clients.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Process

- 2.2.4 Function type

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of automation & industry 4.0

- 3.2.1.2 Increasing demand for high-precision fabrication

- 3.2.1.3 Shift toward energy-efficient fiber & solid-state lasers

- 3.2.1.4 Demand for reduced material waste & higher productivity

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High operational & maintenance expenses

- 3.2.2.2 Material limitations & processing challenges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Solid-state lasers

- 5.3 Gas lasers

- 5.4 Semiconductor laser

Chapter 6 Market Estimates & Forecast, By Process, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Fusion cutting

- 6.3 Flame cutting

- 6.4 Sublimation cutting

Chapter 7 Market Estimates & Forecast, By Function Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Semi-automatic

- 7.3 Robotic

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Consumer electronics

- 8.4 Defense and aerospace

- 8.5 Industrial

- 8.6 Others (medical, energy & power etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Amada

- 11.2 Bystronic

- 11.3 Coherent

- 11.4 Epilog Laser

- 11.5 Han's Laser

- 11.6 IPG Photonics

- 11.7 Jenoptik

- 11.8 LVD Company

- 11.9 Mazak Optonics

- 11.10 Mitsubishi Electric Corporation

- 11.11 Prima Power

- 11.12 Tanaka

- 11.13 Trotec Laser

- 11.14 Trumpf

- 11.15 Universal Laser Systems

雷射切割機市場-全球市場預測(2026-2032年)2D雷射切割機市場:按雷射類型、功率輸出、應用、最終用戶和銷售管道,全球預測,2026-2032年FROG超短脈衝測量儀器市場:按雷射類型、技術、測量模式、銷售管道、應用和最終用戶分類,全球預測,2026-2032年超短脈衝雷射材料加工市場:按雷射配置、雷射類型、波長、系統類型、功率範圍、應用和最終用戶分類的全球預測(2026-2032年)

雷射切割機市場-全球市場預測(2026-2032年)2D雷射切割機市場:按雷射類型、功率輸出、應用、最終用戶和銷售管道,全球預測,2026-2032年FROG超短脈衝測量儀器市場:按雷射類型、技術、測量模式、銷售管道、應用和最終用戶分類,全球預測,2026-2032年超短脈衝雷射材料加工市場:按雷射配置、雷射類型、波長、系統類型、功率範圍、應用和最終用戶分類的全球預測(2026-2032年) 2026年全球雷射切割機市場報告

2026年全球雷射切割機市場報告 全球雷射切割機市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球雷射切割機市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 全球雷射切割機市場,2026-2030年雕刻筆市場:按技術、電源、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

全球雷射切割機市場,2026-2030年雕刻筆市場:按技術、電源、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 雷射切割機市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、製程、最終用戶、地區及競爭格局分類,2021-2031年預測)

雷射切割機市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、製程、最終用戶、地區及競爭格局分類,2021-2031年預測) 低功率和中功率雷射切割控制器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

低功率和中功率雷射切割控制器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)