|

市場調查報告書

商品編碼

1936618

丙烯酸酯市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Acrylate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

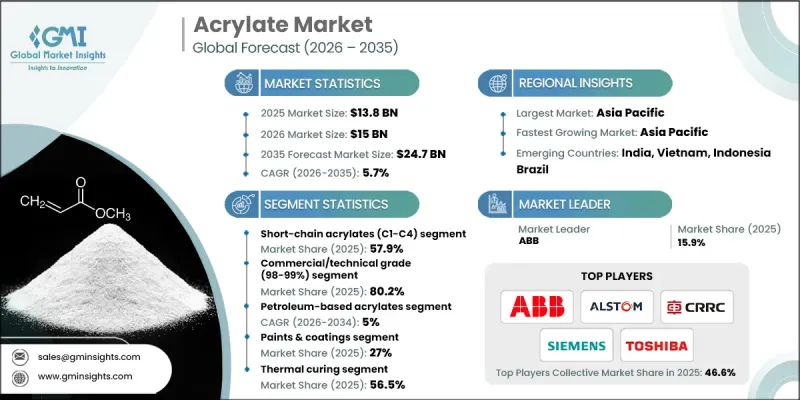

全球丙烯酸酯市場預計到 2025 年將達到 138 億美元,到 2035 年將達到 247 億美元,年複合成長率為 5.7%。

丙烯酸酯已從一種應用範圍狹窄的化學品發展成為支撐各種現代工業流程的基礎材料。其多功能性、耐久性和優異的性能使其成為多個製造生態系統中不可或缺的組成部分。近年來,製造商致力於開發新一代配方,以提高效率並滿足日益嚴格的環境和監管要求。製造流程的不斷改進使製造商能夠在性能最佳化和永續性目標之間取得平衡,使丙烯酸酯成為尖端材料科學的關鍵組成部分。市場持續受益於多元化產業價值鏈的穩定需求,這得益於創新主導的產品差異化以及對環保製造實踐日益成長的關注。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 138億美元 |

| 預測金額 | 247億美元 |

| 複合年成長率 | 5.7% |

永續性已成為影響丙烯酸酯產業的決定性因素。旨在限制排放的監管壓力正在加速向環境友善配方的轉型。製造商正積極投資研發,以開發既符合監管標準又能維持機械強度、耐久性和長期性能的解決方案。這些創新有助於實現更廣泛的全球脫碳目標,並強化丙烯酸酯在永續工業轉型中的作用。隨著環境合規性成為一項競爭優勢,更環保的丙烯酸酯解決方案在全球市場的應用勢頭持續強勁。

預計到2025年,純度為98-99%的商用和技術級丙烯酸酯將佔據80.2%的市場佔有率,並在2026年至2035年間以4.8%的複合年成長率成長。這些等級的產品因其成本效益高、適應性強和性能均衡等優點而備受青睞。其廣泛的應用範圍支撐了多個終端用戶領域的大量需求。同時,高純度等級的產品繼續應用於對均勻性、可靠性和功能性能要求極高的應用領域,從而滿足了專業行業的穩定需求。

預計到2025年,熱固性樹脂將佔據56.5%的市場佔有率,並在2035年之前以4.7%的複合年成長率成長。由於其能夠增強黏合強度和長期耐久性,這種固化方法仍然是工業規模生產的首選。隨著製造商尋求更快的加工速度和更高的能源效率,其他固化技術正日益受到關注。在對性能精度和耐化學性要求極高的特殊工業應用中,先進的固化方法也變得越來越重要。

預計到2025年,北美丙烯酸酯市場將佔據19.6%的市場佔有率,體現了其作為成熟且具有重要戰略意義的地區的地位。先進的製造基礎設施、穩定的工業需求以及促進永續材料使用的健全法規結構為該市場提供了支撐。持續的技術創新和對環境標準的遵守將維持該地區的成長,並繼續鞏固北美在全球競爭格局中的主導地位。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 油漆和塗料行業的需求不斷成長

- 擴大超吸收性聚合物在衛生用品上的應用

- 在黏合劑和密封劑領域不斷擴大應用

- 產業潛在風險與挑戰

- 原物料(丙烯)價格波動

- 嚴格的環境法規

- 市場機遇

- 生物基丙烯酸酯的開發與商業化

- 電動汽車電池黏合劑的成長

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 短鏈丙烯酸酯(C1-C4)

- 甲基丙烯酸甲酯(MA)

- 丙烯酸乙酯(EA)

- 丙烯酸丁酯(BA)

- 丙烯酸異丁酯(iBA)

- 中鏈丙烯酸酯(C6-C10)

- 2-乙基己基丙烯酸酯(2-EHA)

- 2-辛基丙烯酸酯

- 異癸基丙烯酸酯(iDA)

- 長鏈丙烯酸酯(C12-C22)

- 月桂基丙烯酸酯(C12)

- 硬脂酸丙烯酸酯(C18)

- 山嵛基丙烯酸酯(C22)

第6章 各等級市場估算與預測,2022-2035年

- 商業/技術級(98-99%)

- 高純度等級(99%以上)

- 超高純度等級(超過99.5%)

第7章 依原料分類的市場估計與預測,2022-2035年

- 石油衍生的丙烯酸酯

- 生物性丙烯酸酯

- 甘油衍生(丙烯醛法)

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 黏合劑和密封劑

- 壓敏黏著劑(PSA)

- 黏合劑

- 結構性黏著劑

- 水性黏合劑

- 密封劑

- 油漆和塗料

- 建築塗料

- 工業塗料

- 汽車塗料

- 木器漆

- 線圈塗布

- 船舶塗料

- 招牌油漆

- 特殊塗層

- 超吸收性聚合物(SAP)

- 纖維和不織布

- 紡織加工

- 功能性纖維

- 不織布黏合劑

- 地毯背襯

- 塑膠和聚合物

- 衝擊改質劑

- 加工輔助工具

- 壓克力板(PMMA)

- 丙烯酸樹脂

- 紙和紙板

- 個人護理及化妝品

- 護髮

- 護膚

- 彩妝品

- 建築材料

- 混凝土添加劑

- 填縫材料及密封劑

- 防水膜

- 磁磚黏合劑

- 水泥漿和砂漿

- 電學

- 鋰離子電池正極黏合劑

- 半導體塗層

- 顯示技術

- 連接器組裝黏合劑

- 封裝材料

- 醫療保健

- 醫療設備塗層

- 牙科材料

- 傷口敷料黏合劑

- 藥物輸送系統

- 其他

9. 依固化技術分類的市場估算與預測,2022-2035 年

- 熱固化

- 紫外線固化

- 電子束(EB)固化

- 濕固化

- 室溫固化

第10章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 批發商和經銷商

- 線上平台

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第12章:公司簡介

- BASF SE

- The Dow Chemical Company

- Arkema Group

- Nippon Shokubai Co Ltd

- LG Chem Ltd

- Formosa Plastics Corporation

- Jiangsu Jurong Chemical Co Ltd

- Sasol Limited

- Sartomer

- Allnex Group

- Toagosei Co Ltd

- Osaka Organic Chemical Industry Ltd

The Global Acrylate Market was valued at USD 13.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 24.7 billion by 2035.

Acrylates have evolved from a narrowly used chemical category into a foundational material supporting a wide range of modern industrial processes. Their versatility, durability, and performance characteristics make them indispensable across multiple manufacturing ecosystems. Over time, producers have shifted their focus toward developing next-generation formulations that deliver enhanced efficiency while aligning with tightening environmental and regulatory expectations. Continuous improvements in production methods have allowed manufacturers to balance performance optimization with sustainability goals, positioning acrylates as a critical component in advanced material science. The market continues to benefit from consistent demand across diverse industrial value chains, supported by innovation-driven product differentiation and increasing emphasis on environmentally responsible manufacturing practices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.8 Billion |

| Forecast Value | $24.7 Billion |

| CAGR | 5.7% |

Sustainability has become a defining force influencing the acrylate industry. Regulatory pressure aimed at limiting emissions has accelerated the transition toward environmentally compatible formulations. Manufacturers are actively investing in research to develop solutions that meet regulatory thresholds while maintaining mechanical strength, durability, and long-term performance. These innovations contribute to broader global decarbonization objectives and reinforce the role of acrylates in sustainable industrial transformation. As environmental compliance becomes a competitive differentiator, the adoption of greener acrylate solutions continues to gain momentum across global markets.

The commercial and technical grade acrylates with purity levels of 98-99% accounted for 80.2% share in 2025 and are forecast to grow at a CAGR of 4.8% from 2026 to 2035. These grades remain widely preferred due to their cost efficiency, adaptability, and balanced performance characteristics. Their broad usability supports high-volume consumption across multiple end-use segments. In contrast, higher-purity variants continue to serve applications requiring superior consistency, reliability, and functional performance, supporting steady demand from specialized industrial segments.

The thermal curing segment held 56.5% share in 2025 and is expected to grow at a CAGR of 4.7% through 2035. This curing method remains a preferred option for industrial-scale operations due to its ability to enhance bonding strength and long-term durability. Alternative curing technologies are gaining traction as manufacturers seek faster processing times and improved energy efficiency. Advanced curing methods are also finding increasing relevance in specialized industrial applications where performance precision and chemical resistance are essential.

North America Acrylate Market accounted for a 19.6% share in 2025, reflecting its status as a mature and strategically significant region. The market is supported by advanced manufacturing infrastructure, stable industrial demand, and strong regulatory frameworks promoting sustainable material use. Ongoing innovation and compliance with environmental standards continue to sustain regional growth and reinforce North America's competitive position in the global landscape.

Key companies operating in the Global Acrylate Market include Arkema Group, BASF SE, LG Chem Ltd, The Dow Chemical Company, Formosa Plastics Corporation, Nippon Shokubai Co Ltd, Sasol Limited, Allnex Group, Sartomer, Toagosei Co Ltd, Jiangsu Jurong Chemical Co Ltd, and Osaka Organic Chemical Industry Ltd. These players maintain strong market positions through continuous innovation, capacity expansion, and diversified product portfolios To strengthen their foothold, acrylate manufacturers are prioritizing strategic investments in research and development to create high-performance and environmentally compliant formulations. Many companies are expanding production capacities and optimizing supply chains to ensure cost efficiency and consistent product availability. Strategic partnerships, acquisitions, and collaborations are commonly used to enhance technological capabilities and expand geographic reach. Firms are also focusing on portfolio diversification to address evolving customer requirements while improving sustainability credentials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Grade

- 2.2.4 Feedstock

- 2.2.5 Application

- 2.2.6 Curing technology

- 2.2.7 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand from paints & coatings industry

- 3.2.1.2 Expanding superabsorbent polymer applications in hygiene products

- 3.2.1.3 Rising adoption in adhesives & sealants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in raw material (propylene) prices

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Bio-based acrylates development & commercialization

- 3.2.3.2 Growth in electric vehicle battery binders

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Short-Chain Acrylates (C1-C4)

- 5.2.1 Methyl Acrylate (MA)

- 5.2.2 Ethyl Acrylate (EA)

- 5.2.3 Butyl Acrylate (BA)

- 5.2.4 iso-Butyl Acrylate (iBA)

- 5.3 Medium-Chain Acrylates (C6-C10)

- 5.3.1 2-Ethylhexyl Acrylate (2-EHA)

- 5.3.2 2-Octyl Acrylate

- 5.3.3 iso-Decyl Acrylate (iDA)

- 5.4 Long-Chain Acrylates (C12-C22)

- 5.4.1 Lauryl Acrylate (C12)

- 5.4.2 Stearyl Acrylate (C18)

- 5.4.3 Behenyl Acrylate (C22)

Chapter 6 Market Estimates and Forecast, By Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Commercial/technical grade (98-99%)

- 6.3 High purity grade (>99%)

- 6.4 Ultra-pure grade (>99.5%)

Chapter 7 Market Estimates and Forecast, By Feedstock, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Petroleum-based acrylates

- 7.3 Bio-based acrylates

- 7.4 Glycerol-derived (acrolein route)

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Adhesives & sealants

- 8.2.1 Pressure-sensitive adhesives (PSA)

- 8.2.2 Hot melt adhesives

- 8.2.3 Structural adhesives

- 8.2.4 Water-based adhesives

- 8.2.5 Sealants

- 8.3 Paints & coatings

- 8.3.1 Architectural coatings

- 8.3.2 Industrial coatings

- 8.3.3 Automotive coatings

- 8.3.4 Wood coatings

- 8.3.5 Coil coatings

- 8.3.6 Marine coatings

- 8.3.7 Signage coatings

- 8.3.8 Specialty coatings

- 8.4 Superabsorbent polymers (sap)

- 8.5 Textiles & nonwovens

- 8.5.1 Textile finishing

- 8.5.2 Performance textiles

- 8.5.3 Nonwoven binders

- 8.5.4 Carpet backing

- 8.6 Plastics & polymers

- 8.6.1 Impact modifiers

- 8.6.2 Processing aids

- 8.6.3 Acrylic sheets (PMMA)

- 8.6.4 Acrylic resins

- 8.7 Paper & paperboard

- 8.8 Personal care & cosmetics

- 8.8.1 Hair care

- 8.8.2 Skin care

- 8.8.3 Color cosmetics

- 8.9 Construction materials

- 8.9.1 Concrete additives

- 8.9.2 Caulks & sealants

- 8.9.3 Waterproofing membranes

- 8.9.4 Tile adhesives

- 8.9.5 Grouts & mortars

- 8.10 Electronics & electrical

- 8.10.1 Li-ion battery cathode binders

- 8.10.2 Semiconductor coatings

- 8.10.3 Display technologies

- 8.10.4 Connector assembly adhesives

- 8.10.5 Encapsulation materials

- 8.11 Medical & healthcare

- 8.11.1 Medical device coatings

- 8.11.2 Dental materials

- 8.11.3 Wound care adhesives

- 8.11.4 Drug delivery systems

- 8.12 Others

Chapter 9 Market Estimates and Forecast, By Curing Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Thermal curing

- 9.3 Uv curing

- 9.4 Electron-beam (EB) curing

- 9.5 Moisture curing

- 9.6 Ambient/room temperature curing

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct Sales

- 10.3 Distributors & Resellers

- 10.4 Online Platforms

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 BASF SE

- 12.2 The Dow Chemical Company

- 12.3 Arkema Group

- 12.4 Nippon Shokubai Co Ltd

- 12.5 LG Chem Ltd

- 12.6 Formosa Plastics Corporation

- 12.7 Jiangsu Jurong Chemical Co Ltd

- 12.8 Sasol Limited

- 12.9 Sartomer

- 12.10 Allnex Group

- 12.11 Toagosei Co Ltd

- 12.12 Osaka Organic Chemical Industry Ltd

異壬酸丙烯酸酯市場:依產品形態、功能、應用及最終用途產業分類-2026-2032年全球市場預測丙烯酸酯市場:2026-2032年全球市場預測(依產品類型、製造流程、應用及最終用途產業分類)

異壬酸丙烯酸酯市場:依產品形態、功能、應用及最終用途產業分類-2026-2032年全球市場預測丙烯酸酯市場:2026-2032年全球市場預測(依產品類型、製造流程、應用及最終用途產業分類) 全球丙烯酸酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球丙烯酸酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 丙烯酸酯市場規模、佔有率和成長分析(按產品類型、等級、應用、最終用途和地區分類)-2026-2033年產業預測

丙烯酸酯市場規模、佔有率和成長分析(按產品類型、等級、應用、最終用途和地區分類)-2026-2033年產業預測 丙烯酸異丁酯市場規模、佔有率及成長分析(按應用、終端用戶產業、配方、通路及地區分類)-2026-2033年產業預測單官能酸酐市場按應用、最終用途產業、製程和等級分類 - 全球預測 2026-2032

丙烯酸異丁酯市場規模、佔有率及成長分析(按應用、終端用戶產業、配方、通路及地區分類)-2026-2033年產業預測單官能酸酐市場按應用、最終用途產業、製程和等級分類 - 全球預測 2026-2032 異壬酸丙烯酸酯市場規模、佔有率及成長分析(依產品類型、應用、最終用戶、等級、銷售管道及地區分類)-2026-2033年產業預測

異壬酸丙烯酸酯市場規模、佔有率及成長分析(依產品類型、應用、最終用戶、等級、銷售管道及地區分類)-2026-2033年產業預測 丙烯酸異辛酯:全球市場佔有率和排名、總收入和需求預測(2025-2031年)丙烯酸酯單體:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

丙烯酸異辛酯:全球市場佔有率和排名、總收入和需求預測(2025-2031年)丙烯酸酯單體:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 丙烯酸酯市場-全球產業規模、佔有率、趨勢、機會及預測,依化學成分、最終用戶、地區及競爭情況細分,2020-2030 年預測

丙烯酸酯市場-全球產業規模、佔有率、趨勢、機會及預測,依化學成分、最終用戶、地區及競爭情況細分,2020-2030 年預測