|

市場調查報告書

商品編碼

1936615

無塵室設備市場機會、成長要素、產業趨勢分析及2026年至2035年預測Cleanroom Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

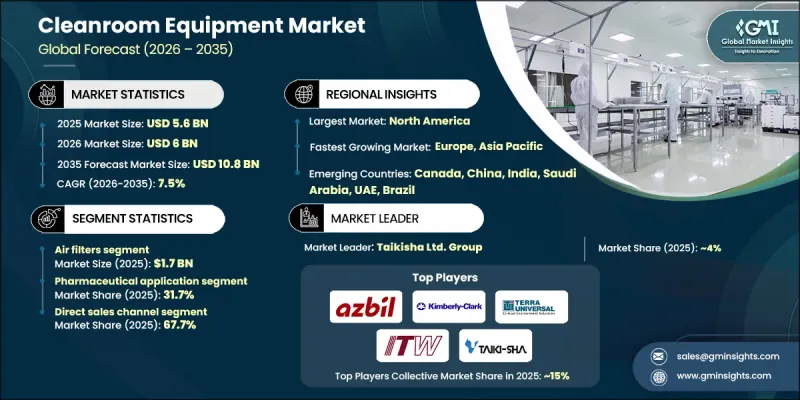

全球無塵室設備市場預計到 2025 年將達到 56 億美元,到 2035 年將達到 108 億美元,年複合成長率為 7.5%。

由於全球製藥、生物技術和先進治療方法製造業的擴張,市場正經歷快速成長。無菌注射劑、生物製藥、疫苗、個人化藥物以及細胞和基因療法的產量增加,顯著提升了對受控生產環境的需求。此類生產空間需要配備最先進的空調系統、HEPA 和 ULPA 過濾器、先進的空氣調節機以及持續的環境監控。推動成長的另一個關鍵因素是模組化和靈活潔淨室解決方案的日益普及。製造商之所以青睞模組化潔淨室,是因為它們安裝成本低、部署快捷,並且能夠根據不斷變化的法規和生產需求擴展生產空間。柔軟性快速擴展或重新配置潔淨室佈局以適應不斷成長的產量和法規要求,是其在全球範圍內廣泛應用的主要驅動力。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 56億美元 |

| 預測金額 | 108億美元 |

| 複合年成長率 | 7.5% |

預計到2025年,空氣濾清器市場規模將達到17億美元,2026年至2035年的複合年成長率將達到7.7%。製藥、生物技術、半導體製造和醫療保健行業嚴格的污染控制法規推動了對高效HEPA和ULPA過濾器的需求。精密電子產品、奈米技術元件和醫療設備的製造業需要超乾淨的空氣環境,這推動了對先進過濾解決方案的需求,無論是新建無塵室還是現有設施的維修,都需要這些解決方案。

截至2025年,直銷通路佔了67.7%的市場佔有率,預計到2035年將以7.2%的複合年成長率成長。直銷模式使企業能夠提供客製化解決方案,例如專用空氣處理機組、整合層流系統以及具備即時監控功能的自動化系統。這種模式確保符合GMP、FDA、EMA、ISO和特定產業標準,同時提供來自單一來源的完整文件、驗證和資格確認。 OEM製造商透過設計、安裝、試運行和全生命週期維護為客戶提供支持,最大限度地降低關鍵無塵室操作中的污染風險和停機時間。

美國潔淨室設備市場預計到2025年將達到15億美元,2026年至2035年的複合年成長率(CAGR)為7.2%。美國強大的製藥和生物技術產業,包括生物製藥、疫苗、無菌注射和先進治療方法,正在推動對無塵室設備的穩定需求。對合約研發生產力機構(CDMO)日益成長的依賴,正在加速開發靈活的多產品無塵室設施,進一步促進市場擴張。對先進的暖氣、通風和空調(HVAC)、高效能空氣微粒過濾器(HEPA/ULPA)、層流空氣系統和即時環境監測的投資,是美國市場成長要素。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 擴大製藥和生物技術製造

- 推出模組化、靈活的無塵室解決方案

- 嚴格的監管和品質合規要求

- 醫療機構更加重視感染控制

- 產業潛在風險與挑戰

- 高資本投資及營運成本

- 能源消耗和永續性

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 透過裝置

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按設備分類的市場估算與預測,2022-2035年

- 空氣浴塵室

- 空氣過濾器

- 高效能空氣過濾器

- ULPA過濾器

- 風機過濾機組

- 吸頂式HEPA過濾器空調機組

- 層流罩

- 水平層流罩

- 垂直層流罩

- 烘乾櫃

- 不銹鋼烘乾機櫃

- 壓克力烘乾櫃

- 直通

- 化學通風櫃

- 潔淨室門

- 捲門

- 自動滑動門

- 其他(水槽、檯面、門聯鎖系統等)

6. 2022-2035年按無塵室類型分類的市場估算與預測

- 傳統無塵室

- 模組化潔淨室

- 模組化軟牆潔淨室

- 移動無塵室

- 混合無塵室

7. 2022-2035年按無塵室類型分類的市場估算與預測

- ISO 1至3級

- ISO 4-5級

- ISO 6-7級

- ISO 8-9級

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 製藥

- 半導體

- 生物技術

- 醫院

- 航太

- 車

- 其他(生命科學、軍事設施、研究實驗室等)

9. 2022-2035年按分銷管道分類的市場估算與預測

- 直銷

- 間接銷售

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章 公司簡介

- Abtech

- Airomax Airborne LLP

- Alpiq holding AG

- Angstrom Technology

- Ardmac Ltd.

- Azbil Corporation

- Camfil AB Source

- Clean Air Products

- HVAX

- Illinois Tool Works Inc.

- Integrated Cleanroom Technologies Pvt. Ltd.

- Kimberly-Clark Corporation

- Labconco

- M+W Group

- Taikisha Ltd.

- Terra Universal Inc.

The Global Cleanroom Equipment Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 7.5% to reach USD 10.8 billion by 2035.

The market is witnessing rapid growth due to the worldwide expansion of pharmaceutical, biotechnology, and advanced therapy manufacturing. The increasing production of sterile injectables, biologics, vaccines, personalized medicines, and cell and gene therapies has created significant demand for controlled manufacturing environments. These production spaces require state-of-the-art HVAC systems, HEPA and ULPA filtration, advanced air handling units, and continuous environmental monitoring. Another key factor fueling growth is the rising adoption of modular and flexible cleanroom solutions. Manufacturers prefer modular cleanrooms for their lower installation costs, rapid deployment, and ability to scale production spaces according to evolving regulatory or production demands. The flexibility to quickly expand or reconfigure cleanroom layouts to meet increasing output requirements or regulatory compliance is driving strong adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 7.5% |

The air filters segment generated USD 1.7 billion in 2025 and is anticipated to grow at a CAGR of 7.7% from 2026 to 2035. Stringent contamination control regulations in pharmaceuticals, biotechnology, semiconductor manufacturing, and healthcare industries are driving demand for high-efficiency HEPA and ULPA filtration. Industries producing sensitive electronics, nanotechnology components, and medical devices require ultra-clean air environments, fueling the need for advanced filtration solutions in both new cleanroom installations and retrofitted facilities.

The direct sales segment held a 67.7% share in 2025 and is expected to grow at a CAGR of 7.2% through 2035. Direct sales allow companies to provide customized solutions such as specialized air handling units, integrated laminar flow systems, and automation with real-time monitoring. This approach ensures compliance with GMP, FDA, EMA, ISO, and industry-specific standards while providing complete documentation, validation, and qualification from a single source. OEMs support customers throughout design, installation, commissioning, and lifecycle maintenance, minimizing contamination risks and downtime in mission-critical cleanroom operations.

U.S. Cleanroom Equipment Market reached USD 1.5 billion in 2025 and is expected to grow at a CAGR of 7.2% from 2026 to 2035. The country's robust pharmaceutical and biotechnology sectors, including biologics, vaccines, sterile injectables, and advanced therapies, drive consistent demand for cleanroom equipment. Increasing reliance on contract development and manufacturing organizations (CDMOs) has accelerated the establishment of multi-product, flexible cleanroom facilities, further supporting market expansion. Investments in advanced HVAC, HEPA/ULPA filtration, laminar airflow systems, and real-time environmental monitoring are key growth drivers in the U.S.

Key players shaping the Global Cleanroom Equipment Market include Abtech, Airomax Airborne LLP, Alpiq Holding AG, Angstrom Technology, Ardmac Ltd., Azbil Corporation, Camfil AB Source, Clean Air Products, HVAX, Illinois Tool Works Inc., Integrated Cleanroom Technologies Pvt. Ltd., Kimberly-Clark Corporation, Labconco, M + W Group, Taikisha Ltd., and Terra Universal Inc. Companies in the cleanroom equipment market strengthen their presence by focusing on product innovation, regulatory compliance, and turnkey solutions. Providers develop modular, scalable, and energy-efficient cleanroom systems to meet evolving industry needs. Strategic collaborations with pharmaceutical, biotech, and semiconductor manufacturers allow co-development of customized solutions. Expanding distribution networks across emerging and established markets improves accessibility, while strong after-sales and maintenance services reinforce customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment

- 2.2.3 Type of cleanroom

- 2.2.4 Cleanroom classification

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expanding pharmaceutical & biotechnology manufacturing

- 3.2.1.2 Adoption of modular & flexible cleanroom solutions

- 3.2.1.3 Stringent regulatory & quality compliance requirements

- 3.2.1.4 Increasing focus on infection control in healthcare facilities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital expenditure & operating costs

- 3.2.2.2 Energy consumption & sustainability constraints

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Air showers

- 5.3 Air filters

- 5.3.1 HEPA filter

- 5.3.2 ULPA filter

- 5.3.3 Fan filter unit

- 5.3.4 Ceiling HEPA filter AC unit

- 5.4 Laminar flow hood

- 5.4.1 Horizontal laminar flow hood

- 5.4.2 Vertical laminar flow hood

- 5.5 Desiccator cabinet

- 5.5.1 Stainless steel desiccator cabinet

- 5.5.2 Acrylic desiccator cabinet

- 5.6 Pass through

- 5.7 Chemical fume hood

- 5.8 Cleanroom doors

- 5.8.1 Roll up doors

- 5.8.2 Automatic sliding doors

- 5.9 Others (sink, bench, door interlock system, etc.)

Chapter 6 Market Estimates & Forecast, By Type of Cleanroom, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Traditional cleanroom

- 6.3 Modular cleanroom

- 6.4 Modular softwall cleanrooms

- 6.5 Mobile cleanrooms

- 6.6 Hybrid cleanrooms

Chapter 7 Market Estimates & Forecast, By Cleanroom Classification, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 ISO Class 1-3

- 7.3 ISO Class 4-5

- 7.4 ISO Class 6-7

- 7.5 ISO Class 8-9

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Pharmaceutical

- 8.3 Semiconductors

- 8.4 Biotechnology

- 8.5 Hospital

- 8.6 Aerospace

- 8.7 Automotive

- 8.8 Others (Life sciences, Military facilities, Research laboratories, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Abtech

- 11.2 Airomax Airborne LLP

- 11.3 Alpiq holding AG

- 11.4 Angstrom Technology

- 11.5 Ardmac Ltd.

- 11.6 Azbil Corporation

- 11.7 Camfil AB Source

- 11.8 Clean Air Products

- 11.9 HVAX

- 11.10 Illinois Tool Works Inc.

- 11.11 Integrated Cleanroom Technologies Pvt. Ltd.

- 11.12 Kimberly-Clark Corporation

- 11.13 Labconco

- 11.14 M + W Group

- 11.15 Taikisha Ltd.

- 11.16 Terra Universal Inc.

全球無塵室設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球無塵室設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球無塵室設備市場報告

2026年全球無塵室設備市場報告 全球無塵室設備市場

全球無塵室設備市場 美國商用無塵室設備市場評估:依產品類型、最終用戶、地區、機會、預測(2017-2031)

美國商用無塵室設備市場評估:依產品類型、最終用戶、地區、機會、預測(2017-2031)