|

市場調查報告書

商品編碼

1936601

生成式人工智慧市場機會、成長要素、產業趨勢分析及2026年至2035年預測Generative AI Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

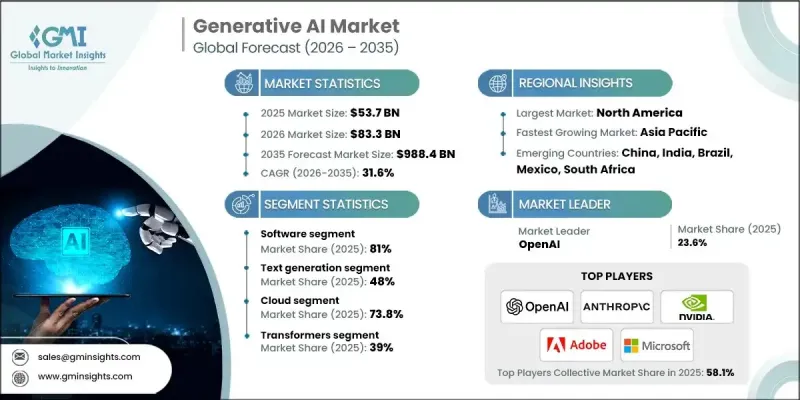

全球生成式人工智慧市場預計到 2025 年將達到 537 億美元,到 2035 年將達到 9,884 億美元,年複合成長率為 31.6%。

各行各業的企業正日益利用生成式人工智慧來簡化營運、加快決策速度並減少人工作業。運算基礎設施、專用人工智慧晶片和模型架構的不斷進步正在提升生成式人工智慧系統的效能和擴充性。處理速度的提升、工作流程的簡化以及先進演算法的運用,使企業能夠處理複雜的人工智慧應用、分析大型資料集並開發創新解決方案,從而加速人工智慧的普及應用並擴大市場。結構化和非結構化數位資料的指數級成長,使得人工智慧模型能夠產生更豐富、產業專用的輸出。人工智慧領導企業與企業軟體供應商之間的策略聯盟和投資,透過將人工智慧整合到關鍵工作流程中,提高了生產力,並在分析、客戶體驗和軟體開發等領域解鎖了新的應用可能性,從而加速了市場發展勢頭。生成式人工智慧正從以文字為中心的工具發展成為能夠在統一環境中生成文字、圖像和語音的多模態模型。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 537億美元 |

| 預測金額 | 9884億美元 |

| 複合年成長率 | 31.6% |

預計到 2025 年,軟體領域將佔 81% 的市場佔有率,並在 2035 年前保持強勁成長,複合年成長率達 30.5%。生成式人工智慧軟體包括開發平台、API、預訓練模型和應用工具,使組織能夠在各個業務職能中部署和擴展人工智慧能力。

預計到2025年,文字產生領域將佔據48%的市場佔有率,並在2026年至2035年間以28%的複合年成長率成長。文字生成技術的普及得益於其在聊天機器人、內容創作、搜尋和企業生產力應用等領域的廣泛應用。其卓越的擴充性、高效性和即時效果,使其成為銀行、醫療保健、零售和IT服務等行業應用最廣泛的人工智慧模式。

預計到2025年,美國生成式人工智慧市場規模將達239億美元。無論是大型企業、Start-Ups或數服務供應商,各組織都在將人工智慧融入核心業務流程,以提高效率、自動化重複性任務並加速創新。隨著企業採用人工智慧解決方案進行數據分析、創造性應用和改進業務,生成式人工智慧已成為美國數位轉型的重要驅動力。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 對自動化和效率的需求日益成長

- 運算能力和演算法的進步

- 數位資料的爆炸性成長

- 增加企業投資和採用

- 產業潛在風險與挑戰

- 資料隱私、安全和監管問題

- 高昂的基礎設施和運算成本

- 市場機遇

- 與現有企業軟體和工作流程的整合

- 拓展至新的工業領域

- 開發多模態人工智慧能力

- 人工智慧工具在中小企業中的引入和推廣

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國聯邦貿易委員會(FTC)指南

- NIST人工智慧風險管理框架

- 美國商務部/工業與安全局(BIS)

- 歐洲

- 歐盟人工智慧法

- GDPR(一般資料保護規則)

- EN/ISO AI 標準

- 國家監管機構

- 亞太地區

- 中國國家人工智慧標準(GB/T)

- 日本工業標準(JIS)人工智慧

- 韓國人工智慧系統KS認證

- 印度資訊科技部(MeitY)人工智慧諮詢

- 新加坡人工智慧管治框架

- 拉丁美洲

- 巴西:通用資料保護法(LGPD)

- 阿根廷:個人資訊保護法

- 墨西哥:NOM 標準

- 中東和非洲

- 阿拉伯聯合大公國和海灣國家的人工智慧政策

- 沙烏地阿拉伯—國家人工智慧戰略

- 非洲聯盟(非盟)人工智慧策略

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢分析

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 經營模式和獲利框架

- 收入模式

- 價值鍊和生態系統

- 打入市場策略

- 資料管治、網路安全與模型風險

- 資料隱私與合規

- 模型安全

- 人工智慧風險與倫理考量

- 操作風險和系統性風險

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

5. 按資料模式分類的市場估算與預測,2022-2035 年

- 文字生成

- 影像生成

- 語音生成

- 影片生成

- 程式碼生成

- 多模態

第6章 依產品類型分類的市場估算與預測,2022-2035年

- 軟體

- 服務

第7章 依實施類型分類的市場估計與預測,2022-2035年

- 雲

- 本地部署

第8章 按技術分類的市場估算與預測,2022-2035年

- 生成對抗網路(GAN)

- 變壓器

- 變分自編碼器

- 擴散網路

- 其他

第9章 按應用領域分類的市場估算與預測,2022-2035年

- 內容創作與創新設計

- 互動式人工智慧和虛擬助手

- 程式碼產生和軟體開發

- 數據增強和合成數據生成

- 預測分析與決策支持

- 設計、模擬和原型製作

- 知識管理和企業搜尋

第10章 依應用領域分類的市場估計與預測,2022-2035年

- 媒體與娛樂

- BFSI

- IT/通訊

- 醫學與生命科學

- 汽車/運輸設備

- 零售與電子商務

- 法律與專業服務

- 其他

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 挪威

- 丹麥

- 荷蘭

- 比利時

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 新加坡

- 馬來西亞

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 世界公司

- OpenAI

- Microsoft

- Amazon Web Services(AWS)

- Meta

- NVIDIA

- Anthropic

- Adobe

- IBM

- Salesforce

- Autodesk

- Accenture

- Capgemini

- Hewlett Packard Enterprise(HPE)

- 區域玩家

- Baidu

- Alibaba Cloud

- Tencent

- Naver

- Mistral AI

- Aleph Alpha

- G42

- 新興企業

- Cohere

- Midjourney

- Perplexity AI

- Hugging Face

- Grok(xAI)

- Runway ML

- Synthesia

The Global Generative AI Market was valued at USD 53.7 billion in 2025 and is estimated to grow at a CAGR of 31.6% to reach USD 988.4 billion by 2035.

Enterprises across industries are increasingly leveraging generative AI to streamline operations, speed up decision-making, and reduce manual tasks. Continuous advancements in computing infrastructure, specialized AI chips, and model architectures are enhancing the performance and scalability of generative AI systems. Faster processing, more efficient workflows, and advanced algorithms allow businesses to handle complex AI applications, analyze larger datasets, and develop innovative solutions, accelerating adoption and expanding the market. The exponential growth of structured and unstructured digital data enables AI models to generate richer, industry-focused outputs. Strategic alliances and investments between AI leaders and enterprise software providers are driving market momentum by integrating AI into critical workflows, boosting productivity, and unlocking new applications across analytics, customer experience, and software development. Generative AI is evolving from text-focused tools to multimodal models capable of producing text, images, and audio in a unified environment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.7 Billion |

| Forecast Value | $988.4 Billion |

| CAGR | 31.6% |

The software segment held 81% share in 2025 and is expected to maintain strong growth at a CAGR of 30.5% through 2035. Generative AI software includes development platforms, APIs, pre-trained models, and application tools that empower organizations to deploy and scale AI capabilities across business functions.

The text generation segment held a 48% share in 2025 and is anticipated to grow at a CAGR of 28% from 2026 to 2035. The popularity of text generation is driven by its widespread use in chatbots, content creation, search, and enterprise productivity applications. Its proven scalability, efficiency, and immediate returns make it the most widely adopted AI modality across industries such as banking, healthcare, retail, and IT services.

U.S. Generative AI Market reached USD 23.9 billion in 2025. Organizations across enterprises, startups, and digital service providers are embedding AI into core workflows to boost efficiency, automate repetitive tasks, and accelerate innovation. Companies are using AI-powered solutions for data analysis, creative applications, and operational improvements, making generative AI an essential driver of digital transformation in the United States.

Key players in the Global Generative AI Market include Accenture, Adobe, Amazon (AWS), Anthropic, Autodesk, Capgemini, Google, Microsoft, NVIDIA, and OpenAI. Companies in the generative AI market are strengthening their presence by investing heavily in research and development to enhance model capabilities and performance. They are forming strategic partnerships with enterprise software vendors to expand their reach and integrate AI into core workflows. Mergers and acquisitions are being used to broaden technology portfolios and gain access to new markets. Firms are also emphasizing scalability, quality assurance, and compliance with data and AI governance standards. Additionally, they are leveraging cloud platforms and AI-as-a-service models to offer flexible solutions, attract new customers, and maintain a competitive edge in a rapidly evolving market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Data Modality

- 2.2.3 Offering

- 2.2.4 Deployment

- 2.2.5 Technology

- 2.2.6 Application

- 2.2.7 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased demand for automation and efficiency

- 3.2.1.2 Advancements in computation power and algorithms

- 3.2.1.3 Explosion of digital data availability

- 3.2.1.4 Growing enterprise investment & adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy, security & regulatory concerns

- 3.2.2.2 High infrastructure & compute costs

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with existing enterprise software & workflows

- 3.2.3.2 Expansion into new industry verticals

- 3.2.3.3 Development of multimodal AI capabilities

- 3.2.3.4 SME adoption and democratization of AI tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Trade Commission (FTC) Guidelines

- 3.4.1.2 National Institute of Standards and Technology (NIST) AI Risk Management Framework

- 3.4.1.3 U.S. Department of Commerce / Bureau of Industry and Security (BIS)

- 3.4.2 Europe

- 3.4.2.1 EU AI Act

- 3.4.2.2 GDPR (General Data Protection Regulation)

- 3.4.2.3 EN / ISO AI Standards

- 3.4.2.4 National Regulatory Authorities

- 3.4.3 Asia Pacific

- 3.4.3.1 China National Standards for AI (GB/T)

- 3.4.3.2 JIS (Japanese Industrial Standards) for AI

- 3.4.3.3 South Korea KS Certification for AI Systems

- 3.4.3.4 India’s MeitY AI Advisory

- 3.4.3.5 Singapore Model AI Governance Framework

- 3.4.4 Latin America

- 3.4.4.1 Brazil: LGPD (Lei Geral de Protecao de Dados)

- 3.4.4.2 Argentina: Personal Data Protection Law

- 3.4.4.3 Mexico: NOM Standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE & Gulf States AI Policies

- 3.4.5.2 Saudi Arabia - National AI Strategy

- 3.4.5.3 African Union (AU) AI Strategy

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing trend analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Business Models and Monetization Framework

- 3.12.1 Revenue Models

- 3.12.2 Value Chain and Ecosystem

- 3.12.3 Go-to-Market Strategy

- 3.13 Data Governance, Cybersecurity, and Model Risk

- 3.13.1 Data Privacy and Compliance

- 3.13.2 Model Security

- 3.13.3 AI Risk and Ethical Considerations

- 3.13.4 Operational and Systemic Risks

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Data Modality, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Text generation

- 5.3 Image generation

- 5.4 Audio generation

- 5.5 Video generation

- 5.6 Code generation

- 5.7 Multimodal

Chapter 6 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Software

- 6.3 Services

Chapter 7 Market Estimates & Forecast, By Deployment, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Generative Adversarial Networks (GANs)

- 8.3 Transformers

- 8.4 Variational Auto-encoders

- 8.5 Diffusion Networks

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Content generation & creative design

- 9.3 Conversational AI & virtual assistants

- 9.4 Code generation & software development

- 9.5 Data augmentation & synthetic data generation

- 9.6 Predictive analytics & decision support

- 9.7 Design, simulation & prototyping

- 9.8 Knowledge management & enterprise search

Chapter 10 Market Estimates & Forecast, By End-Use, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Media & entertainment

- 10.3 BFSI

- 10.4 It & telecom

- 10.5 Healthcare & life sciences

- 10.6 Automotive & transportation

- 10.7 Retail & e-commerce

- 10.8 Legal and professional services

- 10.9 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Norway

- 11.3.9 Denmark

- 11.3.10 Netherlands

- 11.3.11 Belgium

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.4.8 Singapore

- 11.4.9 Malaysia

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 OpenAI

- 12.1.2 Google

- 12.1.3 Microsoft

- 12.1.4 Amazon Web Services (AWS)

- 12.1.5 Meta

- 12.1.6 NVIDIA

- 12.1.7 Anthropic

- 12.1.8 Adobe

- 12.1.9 IBM

- 12.1.10 Salesforce

- 12.1.11 Autodesk

- 12.1.12 Accenture

- 12.1.13 Capgemini

- 12.1.14 Hewlett Packard Enterprise (HPE)

- 12.2 Regional players

- 12.2.1 Baidu

- 12.2.2 Alibaba Cloud

- 12.2.3 Tencent

- 12.2.4 Naver

- 12.2.5 Mistral AI

- 12.2.6 Aleph Alpha

- 12.2.7 G42

- 12.3 Emerging players

- 12.3.1 Cohere

- 12.3.2 Midjourney

- 12.3.3 Perplexity AI

- 12.3.4 Hugging Face

- 12.3.5 Grok (xAI)

- 12.3.6 Runway ML

- 12.3.7 Synthesia

生成式人工智慧市場:按組件、類型、部署模式、應用和產業分類-2026-2032年全球市場預測

生成式人工智慧市場:按組件、類型、部署模式、應用和產業分類-2026-2032年全球市場預測 2026年全球房地產生成式人工智慧市場報告2026年全球生成式人工智慧(AI)聊天機器人市場報告2026年全球生成式人工智慧(AI)自動化市場報告2026年全球生成式人工智慧(AI)與機器人流程自動化(RPA)市場報告2026年全球生成式人工智慧(AI)藝術市場報告2026年全球生成式人工智慧(AI)資料標註解決方案與服務市場報告2026年全球生成式人工智慧(AI)驅動的3D資產市場報告2026年全球產品設計生成式人工智慧(AI)市場報告2026年全球組織協作領域生成式人工智慧市場報告

2026年全球房地產生成式人工智慧市場報告2026年全球生成式人工智慧(AI)聊天機器人市場報告2026年全球生成式人工智慧(AI)自動化市場報告2026年全球生成式人工智慧(AI)與機器人流程自動化(RPA)市場報告2026年全球生成式人工智慧(AI)藝術市場報告2026年全球生成式人工智慧(AI)資料標註解決方案與服務市場報告2026年全球生成式人工智慧(AI)驅動的3D資產市場報告2026年全球產品設計生成式人工智慧(AI)市場報告2026年全球組織協作領域生成式人工智慧市場報告