|

市場調查報告書

商品編碼

1936596

國內增壓幫浦市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Domestic Booster Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

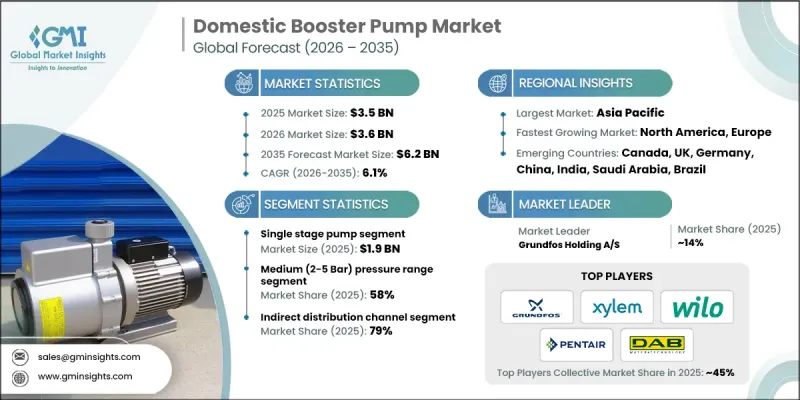

全球國內增壓幫浦市場預計到 2025 年將達到 35 億美元,到 2035 年將達到 62 億美元,年複合成長率為 6.1%。

全球都市化加快,都市區密度不斷增加,推動了住宅增壓幫浦的需求成長。多層住宅、封閉式社區和高層公寓大樓的擴展給市政供水系統帶來了壓力,難以維持穩定的供水。現代住宅的設計旨在容納多戶居住者,通常配備多個浴室和耗水量大的電器,所有這些都需要穩定的水壓。如今,住宅希望在淋浴設備、水龍頭、洗衣機和洗碗機同時使用時,能夠獲得中等水壓的供水,這使得住宅增壓泵從可選升級方案轉變為必備系統。新建住宅和城市住宅的不斷增加,以及節水技術的應用,進一步強化了這一趨勢,確保了舒適性、可靠性和能源效率。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 35億美元 |

| 預測金額 | 62億美元 |

| 複合年成長率 | 6.1% |

單級幫浦市場預計到2025年將達到19億美元,到2035年將以6%的複合年成長率成長。單級增壓幫浦經濟高效、易於安裝,是中低壓住宅應用的理想選擇。它們只需一個葉輪即可高效滿足所需的揚程和流量,因此廣泛應用於獨棟住宅、低層建築、別墅和小規模多用戶住宅。

預計到2025年,中壓(2-5巴)供水系統將佔據58%的市場佔有率,並在2035年之前以6%的複合年成長率成長。這些系統為多衛浴住宅、中低層公寓和住宅社區提供高效率的供水服務,在多個進水口提供穩定的水流,同時避免過度能耗。 2-5巴的壓力範圍符合現代管道標準,可減輕管道壓力,最大限度地減少洩漏,並降低維護成本,使其成為都市區住宅環境的理想選擇。

美國住宅增壓幫浦市場預計到2025年將達到8億美元,到2035年將以5.9%的複合年成長率成長。需求主要來自多層住宅、高層公寓大樓和需要穩定水壓的大型獨棟住宅。老化的城市基礎設施和長距離輸水的挑戰進一步增加了人們對增壓幫浦的依賴。新建住宅計劃、智慧建築開發和維修正朝著採用節能型變頻驅動裝置(VFD)水泵的方向發展,以符合永續性和成本效益的目標。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 快速的都市化和住宅建設

- 水壓不足及供水基礎設施老化

- 多浴室住宅和現代住宅設計的興起

- 智慧家庭和建築自動化的擴展

- 產業潛在風險與挑戰

- 較高的初始安裝和更換成本

- 維護需求和對售後服務的依賴

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 單級泵浦

- 多級泵浦

第6章 依額定產量分類的市場估計與預測,2022-2035年

- 10~50 W

- 50~150 W

- 150~300 W

- 超過300瓦

第7章 依壓力範圍分類的市場估計與預測,2022-2035年

- 低壓(低於 2 巴)

- 中等壓力(2至5巴)

- 高壓(超過 5 巴)

第8章 依最終用途分類的市場估算與預測,2022-2035年

- 住宅

- 商業

- 衛生保健

- HoReCa

- 服務中心

- 大型零售空間

- 其他

- 產業

- 其他(政府等)

第9章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接銷售

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章 公司簡介

- CRI Pumps Private Limited

- DAB Pumps SpA

- Danfoss A/S

- Davey Water Products Pty Ltd.

- Ebara Corporation

- Franklin Electric Co., Inc.

- Grundfos Holding A/S

- Kirloskar Brothers Limited

- KSB SE &Co. KGaA

- Pedrollo SpA

- Pentair plc

- Shimge Pump Industry Group Co., Ltd.

- Wilo SE

- Xylem Inc.

- Zhejiang Dayuan Pumps Industrial Co., Ltd.

The Global Domestic Booster Pump Market was valued at USD 3.5 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 6.2 billion by 2035.

Increasing urbanization and rising population densities in cities worldwide are driving demand for domestic booster pumps. Expanding multi-story residential buildings, gated communities, and high-rise apartments are placing pressure on municipal water systems, making a consistent water supply a challenge. Modern homes are designed to accommodate multiple occupants with several bathrooms and water-intensive appliances, requiring constant water pressure across all fixtures. Homeowners now expect medium-pressure water delivery for showers, faucets, washing machines, and dishwashers simultaneously, shifting domestic booster pumps from optional upgrades to essential systems. This trend is further reinforced by the growing construction of new homes, urban residential complexes, and the adoption of water-efficient technologies to ensure comfort, reliability, and energy efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.5 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 6.1% |

The single-stage pump segment generated USD 1.9 billion in 2025 and is expected to grow at a CAGR of 6% through 2035. Single-stage booster pumps are cost-effective, easy to install, and well-suited for low- to medium-pressure residential applications. They are widely used in single-family homes, low-rise buildings, villas, and smaller apartment complexes where a single impeller meets the required head and flow efficiently.

The medium-pressure range (2-5 Bar) accounted for 58% share in 2025 and is forecasted to grow at a CAGR of 6% through 2035. These systems efficiently serve multi-bathroom homes, low- to mid-rise apartments, and residential complexes, providing consistent water flow across multiple outlets while avoiding excessive energy use. The 2-5 Bar range aligns with modern plumbing codes, prevents pipe stress, minimizes leakage, and reduces maintenance costs, making it ideal for urban residential setups.

U.S. Domestic Booster Pump Market reached USD 0.8 billion in 2025 and is projected to grow at a CAGR of 5.9% through 2035. The demand is driven by multi-story residential buildings, high-rise apartments, and large single-family homes that require stable water pressure. Aging municipal infrastructure and long-distance water transmission challenges are further increasing reliance on booster pumps. New housing projects, smart building developments, and retrofitting initiatives favor energy-efficient pumps with variable frequency drives (VFDs), aligning with sustainability and cost-efficiency goals.

Key players operating in the Global Domestic Booster Pump Market include Grundfos Holding A/S, Franklin Electric Co., Inc., Kirloskar Brothers Limited, Danfoss A/S, Pedrollo S.p.A., Xylem Inc., DAB Pumps S.p.A., and C.R.I. Pumps Private Limited, KSB SE & Co. KGaA, Wilo SE, Ebara Corporation, Pentair plc, Shimge Pump Industry Group Co., Ltd., Zhejiang Dayuan Pumps Industrial Co., Ltd., and Davey Water Products Pty Ltd. Companies in the domestic booster pump market are strengthening their foothold by investing in advanced energy-efficient and VFD-integrated pumps, targeting residential, commercial, and high-rise segments. Strategic partnerships with real estate developers and municipal authorities help expand distribution channels and gain large-scale project contracts. Firms are focusing on R&D to improve pump reliability, reduce noise, and enhance smart control systems for IoT-enabled monitoring. Product portfolio diversification, geographic expansion into urbanizing regions, and after-sales service enhancement allow companies to capture new customers and retain loyalty. Marketing initiatives emphasizing energy savings, sustainability, and compliance with water regulations are boosting market presence and brand reputation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Rated power

- 2.2.4 Pressure range

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid urbanization and residential construction

- 3.2.1.2 Inadequate municipal water pressure and aging water supply infrastructure

- 3.2.1.3 Growth in multi-bathroom and modern housing designs

- 3.2.1.4 Expansion of smart homes and building automation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial installation and replacement costs

- 3.2.2.2 Maintenance requirements and after-sales dependence

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Single stage pump

- 5.3 Multiple stage pump

Chapter 6 Market Estimates & Forecast, By Rated Power, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 10 - 50 W

- 6.3 50 - 150 W

- 6.4 150 - 300 W

- 6.5 Above 300 W

Chapter 7 Market Estimates & Forecast, By Pressure Range, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Low (Up to 2 Bar)

- 7.3 Medium (2-5 Bar)

- 7.4 High (Above 5 Bar)

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Healthcare

- 8.3.2 HoReCa

- 8.3.3 Service centers

- 8.3.4 Mega retail space

- 8.3.5 others

- 8.4 Industrial

- 8.5 Others (Government, Etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 C.R.I. Pumps Private Limited

- 11.2 DAB Pumps S.p.A.

- 11.3 Danfoss A/S

- 11.4 Davey Water Products Pty Ltd.

- 11.5 Ebara Corporation

- 11.6 Franklin Electric Co., Inc.

- 11.7 Grundfos Holding A/S

- 11.8 Kirloskar Brothers Limited

- 11.9 KSB SE & Co. KGaA

- 11.10 Pedrollo S.p.A.

- 11.11 Pentair plc

- 11.12 Shimge Pump Industry Group Co., Ltd.

- 11.13 Wilo SE

- 11.14 Xylem Inc.

- 11.15 Zhejiang Dayuan Pumps Industrial Co., Ltd.

家用增壓幫浦市場:按泵浦類型、材質、動力來源、額定輸出功率和應用分類-全球預測,2026-2032年

家用增壓幫浦市場:按泵浦類型、材質、動力來源、額定輸出功率和應用分類-全球預測,2026-2032年 國內增壓幫浦市場規模、佔有率及成長分析:按泵運作設計、壓力控制機制、泵體材質、銷售管道、分銷通路和地區分類-2026-2033年產業預測增壓幫浦市場:2026-2032年全球市場預測(按幫浦類型、材質、額定功率、銷售管道、應用和最終用戶產業分類)RO增壓幫浦市場:按泵浦類型、壓力、流量、材質和終端用戶產業分類,全球預測,2026-2032年

國內增壓幫浦市場規模、佔有率及成長分析:按泵運作設計、壓力控制機制、泵體材質、銷售管道、分銷通路和地區分類-2026-2033年產業預測增壓幫浦市場:2026-2032年全球市場預測(按幫浦類型、材質、額定功率、銷售管道、應用和最終用戶產業分類)RO增壓幫浦市場:按泵浦類型、壓力、流量、材質和終端用戶產業分類,全球預測,2026-2032年 2026-2034年全球家用增壓幫浦市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球家用增壓幫浦市場規模、佔有率、趨勢和成長分析報告 2026年全球增壓幫浦市場報告淋浴設備泵市場按泵類型、速度類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

2026年全球增壓幫浦市場報告淋浴設備泵市場按泵類型、速度類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)