|

市場調查報告書

商品編碼

1936581

醫療設備冷卻市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Medical Equipment Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

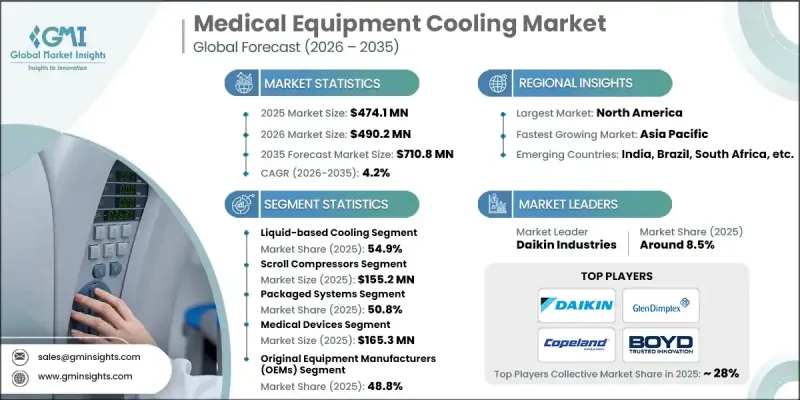

全球醫療設備冷卻市場預計到 2025 年將達到 4.741 億美元,到 2035 年將達到 7.108 億美元,年複合成長率為 4.2%。

市場成長受多種相互關聯的因素驅動,包括慢性病發病率上升、微創手術日益普及、診斷影像設備技術進步以及醫療機構對精確溫度控制的需求不斷成長。溫度控管系統對於維持先進醫療設備的可靠性、使用壽命和最佳性能至關重要,因此推動了對冷卻解決方案的持續投資。癌症和其他慢性病發病率的上升,推動了對需要高容量冷卻解決方案的設備的需求,例如核磁共振造影系統)、CT掃描儀、直線加速器、PET-CT系統和實驗室設備。光是高場核磁共振造影系統每個系統就需要30至50千瓦的冷卻能力,凸顯了強大溫度控管的重要性。此外,全球醫療基礎設施的擴展、技術創新和臨床標準的提高也促進了對醫療設備冷卻解決方案的持續需求。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 4.741億美元 |

| 預測金額 | 7.108億美元 |

| 複合年成長率 | 4.2% |

由於其高效的散熱性能,預計到2025年,液冷系統市佔率將達到54.9%。這些系統包括冷水冷卻器、乙二醇冷卻裝置和直接冷媒技術,非常適合磁振造影(MRI)、電腦斷層掃描(CT)和直線加速器等高熱負荷應用。與風冷系統相比,液冷系統結構緊湊、運作噪音更低,因此是醫院和臨床環境的理想選擇。人們對能源效率、低噪音和高密度散熱的日益關注,進一步加速了液冷技術在全球醫療機構的應用。

預計到2025年,渦捲式壓縮機市場規模將達到1.552億美元,並繼續在製冷量為5至60噸的中小型應用領域保持主導地位。由於其高可靠性、低振動和低噪音運行,渦旋壓縮機被廣泛應用於核磁共振成像(MRI)冰箱、CT掃描儀和精密實驗室空調系統。渦捲式壓縮機壓縮機的平均故障間隔時間(MTBF)高達10萬小時,在關鍵醫療環境中能夠提供可靠的效能。渦旋技術之所以備受青睞,還在於其在低噪音水平下能夠提供穩定的製冷性能,這對於患者照護區和實驗室環境至關重要。

預計到2025年,北美醫療設備冷卻市場將佔據34.4%的市場佔有率,並在預測期內保持強勁成長。該地區擁有先進的診斷成像基礎設施,並不斷更新老舊設備,從而推動了對先進冷卻解決方案的需求。北美醫院和研究中心需要高性能、高可靠性的冷卻系統,以支援高階功能並確保設備的最佳運作狀態。監管標準和對營運效率的重視也推動了對先進溫度控管系統的投資,進一步促進了市場擴張。

目錄

第1章調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策與資料完整性承諾

- 資訊來源完整性通訊協定

- GMI人工智慧政策與資料完整性承諾

- 調查可追溯性和可靠性評分

- 勘測和步道組成部分

- 評分組成部分

- 數據收集

- 主要資訊的部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估計值與計算

- 基準年計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測值的數學影響

- 量化市場影響分析

- 研究透明度附錄

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 慢性病發生率呈上升趨勢

- 診斷顯像模式技術進步

- 對溫度控制的需求日益成長

- 擴大微創手術技術的應用

- 產業潛在風險與挑戰

- 購買和安裝醫療設備冷卻系統的初始成本

- 監理合規挑戰

- 機會

- 增加對新型醫學影像診斷設備的投資

- 拓展冷卻系統在新興醫療技術的應用

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價值鏈分析

- 定價分析

- 環境與永續性考量

- 政策環境

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未來市場趨勢

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 按壓縮機分類的公司市佔率分析

- 往復式壓縮機

- 渦旋壓縮器

- 螺旋壓縮機

- 離心式壓縮機

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 2022-2035年按產品分類的市場估算與預測

- 液冷法

- 空氣冷卻法

第6章 壓縮機市場估算與預測(2022-2035年)

- 往復式壓縮機

- 渦卷式壓縮器

- 螺旋壓縮機

- 離心式壓縮機

7. 按產品類型分類的市場估算與預測,2022-2035 年

- 軟體包系統

- 模組化系統

- 分離式系統

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 醫療設備

- 醫學影像診斷系統

- 磁振造影造影(MRI)

- 電腦斷層掃描器(CT)

- 正子斷層掃描(PET)系統

- 醫用雷射器

- 直線加速器

- 醫學影像診斷系統

- 冷藏保管和測試

- 除濕

- 分析和實驗室設備

9. 依最終用途分類的市場估計與預測,2022-2035 年

- 原始設備製造商 (OEM)

- 醫院

- 診斷檢查室

- 其他最終用途

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章 公司簡介

- American Chillers

- Atlas Copco

- Boyd

- Copeland

- Daikin Industries

- Drake Refrigeration

- Ecochillers

- EKS Thermal Systems

- ELGi Equipments Limited

- Filtrine

- General Air Products

- Glen Dimplex Group

- Haskris

- Ingersoll Rand

- KKT chillers

- Legacy Chillers

- Motivair Corporation

- Tark Thermal Solutions

- Thermal Care

The Global Medical Equipment Cooling Market was valued at USD 474.1 million in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 710.8 million by 2035.

Market growth is fueled by several interconnected factors, including the rising prevalence of chronic diseases, expanding adoption of minimally invasive surgeries, technological advancements in diagnostic imaging devices, and the growing need for precise temperature control in healthcare facilities. Thermal management systems are critical in maintaining the reliability, longevity, and peak performance of sophisticated medical equipment, driving ongoing investment in cooling solutions. Increasing cancer incidence and other chronic conditions are boosting the demand for MRI units, CT scanners, linear accelerators, PET-CT systems, and laboratory equipment, all of which require high-capacity cooling solutions. High-field MRI units alone demand 30-50 kW of cooling per system, highlighting the importance of robust thermal management. Additionally, the expanding global healthcare infrastructure, technological innovation, and rising clinical standards contribute to sustained demand for medical equipment cooling solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $474.1 Million |

| Forecast Value | $710.8 Million |

| CAGR | 4.2% |

The liquid-based cooling systems segment accounted for 54.9% share in 2025, driven by their high heat removal efficiency. These systems, including chilled water chillers, glycol cooling units, and direct refrigerant technologies, are ideal for applications with high thermal loads, such as MRI and CT machines or linear accelerators. Liquid cooling offers compact designs and quieter operation compared to air-cooled systems, making them well-suited for hospital and clinical environments. The growing focus on energy efficiency, reduced noise levels, and high-density heat dissipation further accelerates the adoption of liquid-based cooling technologies across healthcare facilities globally.

The scroll compressors segment generated USD 155.2 million in 2025 and continues to dominate small- to medium-capacity applications ranging from 5 to 60 tons of cooling. They are widely deployed in MRI chillers, CT scanners, and precision laboratory air conditioning systems due to their high reliability, low vibration, and quiet operation. With an average time between failures of 100,000 hours, scroll compressors provide dependable performance in critical healthcare environments. The preference for scroll technology is also driven by its ability to deliver consistent cooling at lower operational noise levels, which is essential in patient care areas and laboratory settings.

North America Medical Equipment Cooling Market held 34.4% share in 2025 and is expected to maintain strong growth during the forecast period. The region leads in diagnostic imaging infrastructure and ongoing replacement of aging equipment, resulting in heightened demand for advanced cooling solutions. Hospitals and research centers in North America increasingly require high-performance, reliable cooling systems that support premium features and ensure optimal equipment functionality. Regulatory standards and a focus on operational efficiency also encourage investment in advanced thermal management systems, further supporting market expansion.

Key players in the Global Medical Equipment Cooling Market include American Chillers, Atlas Copco, Boyd, Copeland, Daikin Industries, Drake Refrigeration, Ecochillers, EKS Thermal Systems, ELGi Equipments Limited, Filtrine, General Air Products, Glen Dimplex Group, Haskris, Ingersoll Rand, KKT Chillers, Legacy Chillers, Motivair Corporation, Tark Thermal Solutions, and Thermal Care. Companies are strengthening market presence through continuous R&D to enhance liquid and air-cooled system efficiency, noise reduction, and compact design. Strategic partnerships with hospitals, diagnostic centers, and medical equipment manufacturers help expand distribution channels. Many players are introducing modular and scalable cooling solutions to cater to diverse healthcare facilities. Investments in energy-efficient, eco-friendly, and low-maintenance technologies help firms differentiate their offerings.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Compressor trends

- 2.2.4 Configuration trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Technological advancements in diagnostic imaging modalities

- 3.2.1.3 Growing demand for temperature control

- 3.2.1.4 Rising adoption of minimally invasive surgical techniques

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Upfront costs associated with purchasing and installing medical equipment cooling systems

- 3.2.2.2 Regulatory compliance challenges

- 3.2.3 Opportunities

- 3.2.3.1 Increased investment in new medical imaging and diagnostic equipment

- 3.2.3.2 Expanding applications of cooling systems in new medical technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Pricing analysis

- 3.8 Environmental and sustainability considerations

- 3.9 Policy landscape

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis, by compressors

- 4.3.1 Reciprocating compressors

- 4.3.2 Scroll compressors

- 4.3.3 Screw compressors

- 4.3.4 Centrifugal compressors

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Liquid-based cooling

- 5.3 Air-based cooling

Chapter 6 Market Estimates and Forecast, By Compressor, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Reciprocating compressors

- 6.3 Scroll compressors

- 6.4 Screw compressors

- 6.5 Centrifugal compressors

Chapter 7 Market Estimates and Forecast, By Configuration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Packaged systems

- 7.3 Modular systems

- 7.4 Split systems

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Medical devices

- 8.2.1 Medical imaging systems

- 8.2.1.1 Magnetic resonance imaging systems (MRI)

- 8.2.1.2 Computed tomography scanners (CT)

- 8.2.1.3 Positron emission tomography systems (PET)

- 8.2.2 Medical lasers

- 8.2.3 Linear accelerators

- 8.2.1 Medical imaging systems

- 8.3 Cold Storage and testing

- 8.4 Dehumidification

- 8.5 Analytical & laboratory equipment

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Original equipment manufacturers (OEMs)

- 9.3 Hospitals

- 9.4 Diagnostic laboratories

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 American Chillers

- 11.2 Atlas Copco

- 11.3 Boyd

- 11.4 Copeland

- 11.5 Daikin Industries

- 11.6 Drake Refrigeration

- 11.7 Ecochillers

- 11.8 EKS Thermal Systems

- 11.9 ELGi Equipments Limited

- 11.10 Filtrine

- 11.11 General Air Products

- 11.12 Glen Dimplex Group

- 11.13 Haskris

- 11.14 Ingersoll Rand

- 11.15 KKT chillers

- 11.16 Legacy Chillers

- 11.17 Motivair Corporation

- 11.18 Tark Thermal Solutions

- 11.19 Thermal Care