|

市場調查報告書

商品編碼

1936572

升級再造食品市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Upcycled Food Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

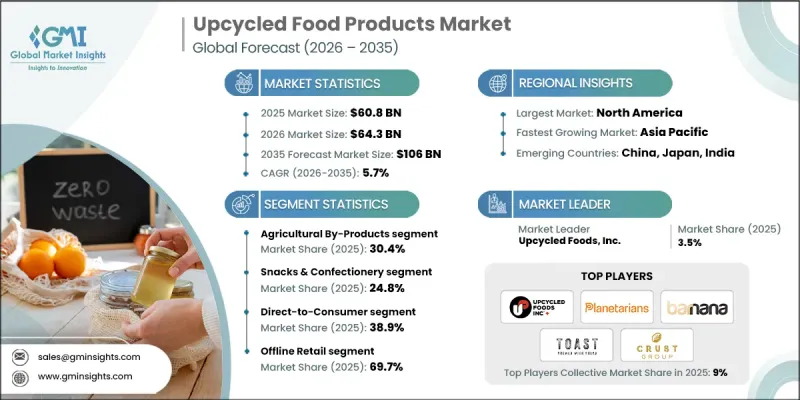

全球升級再造食品市場預計到 2025 年將達到 608 億美元,到 2035 年將達到 1,060 億美元,年複合成長率為 5.7%。

隨著永續性計劃、日益增強的環保意識和持續創新推動全球食品產業轉型,市場呈現強勁的成長動能。製造商正加速將剩餘食品原料、農業殘渣和加工產品轉化為高附加價值食品原料,這些原料不僅營養價值更高、保存期限更長,而且應用範圍更廣。消費者對永續生產食品的接受度不斷提高,促使各大品牌擴大生產規模,並將升級再造原料融入主流產品。先進的加工技術能夠將傳統上價值較低的食品廢棄物轉化為營養成分和穩定性較佳的功能性原料。在競爭日益激烈的背景下,技術差異化已成為成功的關鍵因素,推動了對創新、策略合作和智慧財產權開發的投資。這些變化使升級再造食品成為一種既能減少廢棄物又能滿足消費者對永續和功能性營養不斷變化的需求的商業性可行解決方案。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 608億美元 |

| 預測金額 | 1060億美元 |

| 複合年成長率 | 5.7% |

預計到2025年,農業副產品市佔率將達到30.4%,並在2035年之前維持6%的複合年成長率。該細分市場憑藉著穩定的原料供應、可靠的採購管道和高效的生產擴張能力,持續保持主導地位。可預測的供應鏈和完善的工業加工系統支撐著其持續成長,使農業衍生原料繼續成為多個產品類型中升級再造食品製造的基礎。

預計到2025年,零食和糖果甜點類產品將佔據24.8%的市場佔有率,並在2034年之前以5.5%的複合年成長率成長。消費者較高的認知度、頻繁的衝動性購買行為以及有效的以永續發展為中心的品牌推廣,都支撐著該細分市場的領先地位。持續的創新以及與潔淨標示和環保理念的契合,預計將推動該細分市場與整體市場成長保持同步,實現穩步擴張。

預計2025年,北美再生食品市場規模將達到243億美元,在預測期內維持強勁成長。該地區受益於消費者對永續性的高度重視、旨在減少食物廢棄物的有利法規結構以及先進的食品加工能力。完善的供應鏈和創新主導的食品製造生態系統持續推動再生原料和成品在各個品類中的應用。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 消費者對永續和符合倫理的食品消費需求迅速成長

- 全球減少食物廢棄物的指令支持循環經濟商業經營模式。

- 企業環境、社會及公司治理(ESG)措施:在產品配方中增加永續成分的使用

- 產業潛在風險與挑戰

- 消費者對升級再造產品的安全性、品質和口味持懷疑態度

- 食品加工副產品的供應與品質有波動

- 全球市場中針對升級再造食品的法規結構碎片化

- 市場機遇

- 拓展高利潤B2B原料市場(面向食品飲料生產商)

- 利用生物活性廢棄物開發機能性食品和營養保健品

- 與大型食品加工企業建立策略夥伴關係,以實現廢棄物貨幣化

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按原料

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 依原料分類的市場估算與預測,2022-2035年

- 食物廢棄物

- 農業副產品

- 釀酒廠和蒸餾廠廢棄物

- 食品加工副產品

- 其他

第6章 依產品類型分類的市場估算與預測,2022-2035年

- 零嘴零食和糖果甜點

- 烘焙食品和穀物產品

- 乳製品替代品及冷凍食品

- 成分和補充劑

- 已調理食品和餐食

- 個人保健產品

- 寵物食品

- 家居用品

第7章 依最終用戶分類的市場估算與預測,2022-2035年

- 直接面對消費者

- 餐飲服務及旅館業

- 原料製造商(B2B)

- 公共和政府機構

- 寵物護理業

- 美容及個人護理

第8章 按分銷管道分類的市場估算與預測,2022-2035年

- 線上/電子商務

- 線下零售

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Barnana

- CRUST Group Pte. Ltd.

- Green Bowl Foods

- I Am Grounded

- Matriark Foods

- Planetarians

- Rootly ApS

- Rubies in the Rubble Ltd.

- Toast Ale Ltd.

- Upcycled Foods, Inc.

The Global Upcycled Food Products Market was valued at USD 60.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 106 billion by 2035.

The market is witnessing strong momentum as sustainability initiatives, rising environmental awareness, and ongoing innovation reshape the global food industry. Manufacturers are increasingly converting surplus food materials, agricultural residues, and processing outputs into value-added food ingredients that offer improved nutrition, extended shelf life, and broader product applications. Growing consumer acceptance of sustainably produced foods has encouraged brands to scale production and incorporate upcycled inputs into mainstream offerings. Advanced processing technologies are enabling companies to convert previously low-value food waste into functional ingredients with enhanced nutritional profiles and stability. As competition intensifies, technological differentiation has become a critical success factor, driving investments in innovation, strategic partnerships, and intellectual property development. These shifts are positioning upcycled foods as a commercially viable solution for waste reduction while meeting evolving consumer demand for sustainable and functional nutrition.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $60.8 Billion |

| Forecast Value | $106 Billion |

| CAGR | 5.7% |

The agricultural by-products segment accounted for 30.4% share in 2025 and is expected to grow at a CAGR of 6% through 2035. This segment continues to lead due to consistent raw material availability, reliable sourcing channels, and the ability to scale production efficiently. Predictable supply chains and established industrial processing frameworks support sustained growth, allowing agriculture-derived inputs to remain a cornerstone of upcycled food manufacturing across multiple product categories.

The snacks and confectionery segment held 24.8% share in 2025 and is projected to grow at a CAGR of 5.5% through 2034. Strong consumer familiarity, frequent impulse purchasing behavior, and effective sustainability-focused branding have supported segment dominance. Continued innovation and alignment with clean-label and eco-conscious trends are expected to drive steady expansion in line with overall market growth.

North America Upcycled Food Products Market reached USD 24.3 billion in 2025 and is expected to experience strong growth over the forecast period. The region benefits from high consumer awareness of sustainability, supportive regulatory frameworks aimed at reducing food waste, and advanced food processing capabilities. Well-developed supply chains and innovation-driven food manufacturing ecosystems continue to support the expansion of upcycled ingredients and finished products across diverse categories.

Key companies operating in the Global Upcycled Food Products Market include Upcycled Foods, Inc., Barnana, Planetarians, Toast Ale Ltd., Rubies in the Rubble Ltd., Rootly ApS, Matriark Foods, CRUST Group Pte. Ltd., Green Bowl Foods, and I Am Grounded. Companies in the upcycled food products market are adopting a range of strategies to strengthen their competitive position and expand market presence. Significant investment is being directed toward research and development to enhance ingredient functionality, nutritional value, and shelf stability. Strategic partnerships with food processors, retailers, and agricultural suppliers help secure consistent raw material streams and expand distribution networks. Firms are also focusing on product diversification to address multiple food categories and consumer segments. Branding strategies centered on sustainability, transparency, and waste reduction are being leveraged to build consumer trust and loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source Type

- 2.2.3 Product Type

- 2.2.4 End User

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid Growth in Consumer Demand for Sustainable and Ethical Food Consumption

- 3.2.1.2 Global Food Waste Reduction Mandates Supporting Circular Economy Business Models

- 3.2.1.3 Corporate ESG Commitments Increasing Use of Sustainable Ingredients in Product Formulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Consumer Skepticism Around Safety, Quality, and Taste of Upcycled Products

- 3.2.2.2 Inconsistent Availability and Quality of Food Processing By-Product Feedstocks

- 3.2.2.3 Fragmented Regulatory Frameworks for Upcycled Foods Across Global Markets

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of High-Margin B2B Ingredients for Food and Beverage Manufacturers

- 3.2.3.2 Development of Functional Foods and Nutraceuticals from Bioactive Waste Compounds

- 3.2.3.3 Strategic Partnerships with Large Food Processors to Monetize Waste Streams

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By source type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Food Waste

- 5.3 Agricultural By-Products

- 5.4 Brewery & Distillery Waste

- 5.5 Food Processing By-Products

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Snacks & Confectionery

- 6.3 Bakery & Cereal Products

- 6.4 Dairy Alternatives & Frozen

- 6.5 Ingredients & Supplements

- 6.6 Prepared Foods & Meals

- 6.7 Personal Care Products

- 6.8 Pet Food

- 6.9 Household Products

Chapter 7 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct-to-Consumer

- 7.3 Food Service & Hospitality

- 7.4 Ingredient Manufacturers (B2B)

- 7.5 Institutional & Government

- 7.6 Pet Care Industry

- 7.7 Beauty & Personal Care

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online / E-Commerce

- 8.3 Offline Retail

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Barnana

- 10.2 CRUST Group Pte. Ltd.

- 10.3 Green Bowl Foods

- 10.4 I Am Grounded

- 10.5 Matriark Foods

- 10.6 Planetarians

- 10.7 Rootly ApS

- 10.8 Rubies in the Rubble Ltd.

- 10.9 Toast Ale Ltd.

- 10.10 Upcycled Foods, Inc.