|

市場調查報告書

商品編碼

1936557

手術導航系統市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Surgical Navigation Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

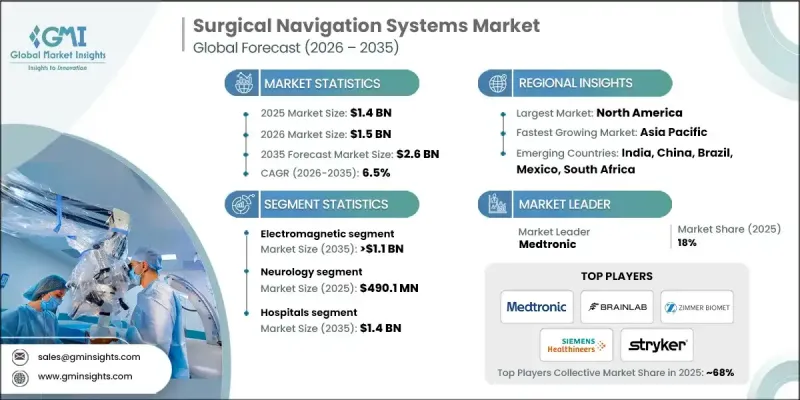

全球手術導航系統市場預計到 2025 年將達到 14 億美元,到 2035 年將達到 26 億美元,年複合成長率為 6.5%。

市場成長的驅動力來自複雜外科手術數量的增加、微創手術的日益普及以及影像和導航技術的不斷進步。手術導航系統提供電腦輔助的即時視覺化,幫助外科醫生更精準、安全、有效率地規劃和執行手術。透過將術前或術中影像與先進的追蹤設備結合,這些系統能夠改善整形外科、神經外科、耳鼻喉科和脊椎外科手術的療效。 3D影像、人工智慧軟體、即時追蹤以及CT/MRI融合等創新技術正在提升系統的易用性和精準度。擴增實境(AR)和虛擬實境(VR)技術正被擴大應用於將數位導板疊加到手術視野上,從而減輕外科醫生的認知負荷,最佳化術中決策,並增強手術規劃。人們對精準微創手術益處的認知不斷提高,推動了醫院對先進導航技術的投資,進而促進了全球市場的持續成長。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 14億美元 |

| 預測金額 | 26億美元 |

| 複合年成長率 | 6.5% |

到2025年,電磁導航市場佔有率將達到44.5%。其受歡迎程度主要得益於其無需視線限制的高追蹤精度、在複雜解剖區域易於導航以及在耳鼻喉科、神經外科和微創手術中的廣泛應用。電磁導航系統使外科醫生能夠即時準確地觀察器械位置,即使在難以直接觀察的情況下也能如此。這種精準的定位能力提高了手術安全性,並確保在狹窄深部手術區域內進行精確導航,使其成為複雜手術中不可或缺的技術。

預計到2025年,神經外科市場規模將達到4.901億美元,2026年至2035年的複合年成長率(CAGR)為5.9%。腦腫瘤、癲癇、中風和神經退化性疾病的日益增多,推動了對精準神經外科手術的需求。導航系統能夠精準標靶化病灶,同時避免重要的腦組織結構,進而減少併發症並改善術後恢復。即時導航技術使得在最大限度降低重要組織損傷風險的情況下進行精細手術成為可能,直接改善臨床療效並保障病人安全。

預計到2025年,美國手術導航系統市場規模將達到4.971億美元,反映出導航系統在北美醫療機構的廣泛應用。該地區的醫院優先進行微創手術和精準干預,以改善患者預後,這推動了他們對手術導航系統的依賴。此外,北美在先進外科技術的臨床研究和試驗方面處於主導。這些研究的證據支持了導航系統的有效性,從而推動了其在臨床醫生中的廣泛應用。政府的支持、先進的醫院基礎設施和高額的醫療保健支出進一步鞏固了該地區的市場主導地位。

目錄

第1章調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策與資料完整性承諾

- 資訊來源完整性通訊協定

- GMI人工智慧政策與資料完整性承諾

- 調查可追溯性和可靠性評分

- 勘測和步道組成部分

- 評分組成部分

- 數據收集

- 主要資訊的部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估計值與計算

- 兩種方法的基準年計算均適用。

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 研究透明度附錄

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 對微創手術的需求日益成長

- 手術導航系統的技術進步

- 整形外科和神經系統疾病病例增加

- 耳鼻喉疾病目標患者群快速成長

- 產業潛在風險與挑戰

- 昂貴的設備和手術費用

- 嚴格的政府法規

- 市場機遇

- 新興市場的擴張

- 在非傳統專業領域擴大應用

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 科技趨勢

- 當前技術趨勢

- 新興技術

- Start-Ups場景

- 未來市場趨勢

- 價值鏈分析

- 波特五力分析

- PESTEL 分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 公司市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按技術分類的市場估算與預測,2022-2035年

- 電磁

- 光科技

- 混合

第6章 按應用領域分類的市場估算與預測,2022-2035年

- 神經病學

- 整形外科

- 膝蓋

- 髖關節

- 肩膀

- 耳鼻喉科

- 牙科

- 其他用途

7. 依最終用途分類的市場估計與預測,2022-2035 年

- 醫院

- 門診手術中心

- 其他用途

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Amplitude Surgical

- B. BRAUN

- BRAINLAB

- Corin

- Fiagon

- Johnson &Johnson

- KARL STORZ

- Medtronic

- Philips

- Siemens Healthineers

- Smith+Nephew

- Stryker

- Zimmer Biomet

The Global Surgical Navigation Systems Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 2.6 billion by 2035.

Market growth is driven by the rising number of complex surgical procedures, increasing adoption of minimally invasive surgeries, and continuous technological advancements in imaging and navigation. Surgical navigation systems provide computer-assisted, real-time visualization, helping surgeons plan and execute procedures with higher accuracy, safety, and efficiency. By combining pre-operative or intraoperative imaging with advanced tracking devices, these systems improve outcomes in orthopedic, neurosurgical, ENT, and spinal interventions. Innovations such as 3D imaging, AI-enabled software, real-time tracking, and integration with CT/MRI have enhanced usability and precision. Augmented reality and virtual reality are increasingly incorporated to overlay digital guides onto the surgical field, enabling surgeons to reduce cognitive load, optimize intraoperative decision-making, and enhance surgical planning. Rising awareness of the benefits of accurate, minimally invasive procedures is prompting hospitals to invest in advanced navigation technologies, fueling sustained market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 6.5% |

The electromagnetic navigation segment held 44.5% share in 2025. Its popularity stems from high tracking accuracy without line-of-sight limitations, ease of use in complex anatomical regions, and strong adoption in ENT, neurosurgery, and minimally invasive procedures. Electromagnetic systems allow surgeons to visualize the exact position of instruments in real-time, even when direct visual access is blocked. This precise localization enhances safety and ensures accurate navigation through deep or restricted surgical sites, making it indispensable for complex interventions.

The neurology segment generated USD 490.1 million in 2025 and is expected to grow at a CAGR of 5.9% from 2026 to 2035. The increasing prevalence of brain tumors, epilepsy, stroke, and degenerative neurological disorders is driving demand for precise neurosurgical procedures. Navigation systems enable surgeons to accurately target lesions while avoiding critical brain structures, reducing complications, and improving postoperative recovery. Real-time guidance ensures delicate operations are performed with minimal risk to vital tissues, directly enhancing clinical outcomes and patient safety.

U.S. Surgical Navigation Systems Market was valued at USD 497.1 million in 2025, reflecting strong adoption of navigation systems in North American healthcare facilities. Hospitals in the region prioritize minimally invasive procedures and accurate interventions to improve patient outcomes, which has increased the reliance on surgical navigation systems. Additionally, North America leads in clinical research and trials involving advanced surgical technologies. Evidence generated from these studies validates the effectiveness of navigation systems, encouraging widespread adoption among clinicians. Government support, advanced hospital infrastructure, and high healthcare expenditure further strengthen the region's market dominance.

Key players operating in the Global Surgical Navigation Systems Market include Philips, Medtronic, Stryker, Zimmer Biomet, Johnson & Johnson, KARL STORZ, Amplitude Surgical, B. BRAUN, Corin, Fiagon, BRAINLAB, Siemens Healthineers, and Smith+Nephew. Companies in the surgical navigation systems market are expanding their presence by focusing on technological innovation, developing AI-enabled and AR/VR-integrated platforms, and enhancing product accuracy and usability. Strategic collaborations with hospitals, research institutes, and clinical trial organizations allow companies to validate solutions and increase adoption. Expanding geographic reach, establishing regional distribution networks, and providing comprehensive after-sales and training services strengthen market foothold. Manufacturers are also investing in modular, customizable systems for diverse surgical specialties to address niche requirements.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for minimally invasive surgical procedures

- 3.2.1.2 Technological advancements in surgical navigation systems

- 3.2.1.3 Rise in orthopedic and neurology disorders

- 3.2.1.4 Surging target patient pool of ENT disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High instrument and procedural costs

- 3.2.2.2 Stringent government regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Increasing use in non-traditional specialties

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Start-up scenarios

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Electromagnetic

- 5.3 Optical

- 5.4 Hybrid

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Neurology

- 6.3 Orthopedic

- 6.3.1 Knee

- 6.3.2 Hip

- 6.3.3 Shoulder

- 6.4 ENT

- 6.5 Dental

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amplitude Surgical

- 9.2 B. BRAUN

- 9.3 BRAINLAB

- 9.4 Corin

- 9.5 Fiagon

- 9.6 Johnson & Johnson

- 9.7 KARL STORZ

- 9.8 Medtronic

- 9.9 Philips

- 9.10 Siemens Healthineers

- 9.11 Smith+Nephew

- 9.12 Stryker

- 9.13 Zimmer Biomet

手術導航系統市場:按組件、導航技術、手術類型、應用和最終用戶分類-2026-2032年全球市場預測手術導航軟體市場:按技術、導航模式、應用和最終用戶分類-2026年至2032年全球市場預測

手術導航系統市場:按組件、導航技術、手術類型、應用和最終用戶分類-2026-2032年全球市場預測手術導航軟體市場:按技術、導航模式、應用和最終用戶分類-2026年至2032年全球市場預測 全球手術導引系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球手術導引系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球電磁追蹤系統市場報告2026年全球手術導航系統市場報告

2026年全球電磁追蹤系統市場報告2026年全球手術導航系統市場報告 日本手術導航系統市場規模、佔有率、趨勢及預測(按技術、應用、最終用戶和地區分類,2026-2034 年)報告格式:PDF+Excel | 報告編號:SR112026A34106支氣管鏡導航系統市場按產品類型、技術、部署環境、分銷管道、最終用戶和應用分類-全球預測,2026-2032年

日本手術導航系統市場規模、佔有率、趨勢及預測(按技術、應用、最終用戶和地區分類,2026-2034 年)報告格式:PDF+Excel | 報告編號:SR112026A34106支氣管鏡導航系統市場按產品類型、技術、部署環境、分銷管道、最終用戶和應用分類-全球預測,2026-2032年 手術導航系統市場規模、佔有率和成長分析(按用途、應用和地區分類)-2026-2033年產業預測

手術導航系統市場規模、佔有率和成長分析(按用途、應用和地區分類)-2026-2033年產業預測 神經導航系統市場規模、佔有率和成長分析(按技術、應用、最終用戶和地區分類)—2026-2033年產業預測

神經導航系統市場規模、佔有率和成長分析(按技術、應用、最終用戶和地區分類)—2026-2033年產業預測 門診顯微外科手術機器人市場預測至2032年:按機器人類型、技術、應用、最終用戶和地區分類的全球分析

門診顯微外科手術機器人市場預測至2032年:按機器人類型、技術、應用、最終用戶和地區分類的全球分析