|

市場調查報告書

商品編碼

1936553

聲學面板市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Acoustic Panel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

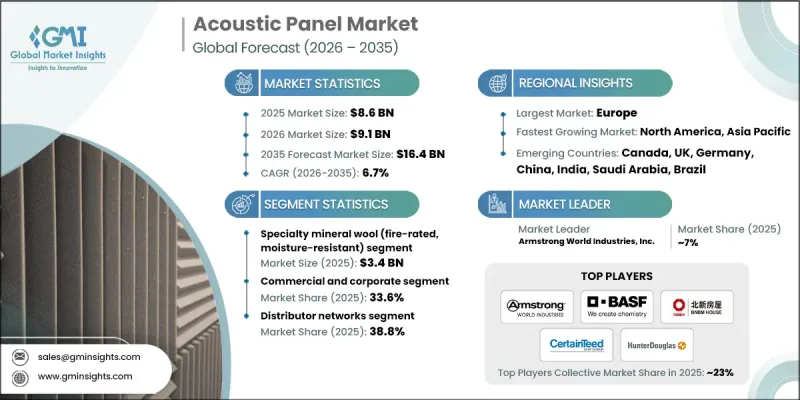

全球聲學面板市場預計到 2025 年將達到 86 億美元,到 2035 年將達到 164 億美元,年複合成長率為 6.7%。

都市化的加速和都市區密度的增加導致住宅和商業環境中的噪音水平不斷上升。隨著城市噪音日益嚴重,對有效隔音解決方案的需求也變得比以往任何時候都更加迫切。世界衛生組織(WHO)已將噪音列為一項重要的環境健康風險,長期暴露於噪音環境中與壓力、睡眠障礙、心血管疾病和其他健康問題密切相關。人們對噪音危害的認知不斷提高,促使吸音板的應用激增。這些吸音板廣泛應用於辦公室、住宅、學校、醫院和公共場所,用於吸收聲音、減少混響並改善室內聲學舒適度。此外,商業建築和維修計劃的擴張也推動了市場需求,因為在現代建築中,聲學品質與設計和功能性一樣日益受到重視。製造商們積極響應市場需求,提供符合嚴格性能、美觀性和永續性要求的吸音板,從而創造了充滿活力的市場環境。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 86億美元 |

| 預測金額 | 164億美元 |

| 複合年成長率 | 6.7% |

預計到2025年,特種礦物棉市場規模將達到34億美元,2026年至2035年的複合年成長率將達到7%。各國政府和監管機構正在商業、公共和高密度住宅領域,尤其是在機場、醫院、教育設施、飯店、資料中心和交通樞紐等場所,實施更為嚴格的消防安全標準。礦物棉的不可燃特性(通常達到歐洲A1級或同等防火等級)使其成為這些應用的理想材料。憑藉其固有的耐火性、熱穩定性和隔音性能,該市場能夠滿足不斷發展的安全法規和永續性目標的需求。

分銷網路佔據了38.8%的市場佔有率,預計到2035年將保持6.7%的複合年成長率。這些網路擁有廣泛的地域覆蓋、深厚的市場知識以及與建築師、承包商、室內設計師和設施管理人員建立的穩固關係。經銷商在大規模建築和維修計劃中發揮關鍵作用,能夠及時提供供應、技術指導和售後支援。由於吸音板需要客製化,例如防火性能、防潮性能、吸聲係數(NRC)等級和設計飾面,分銷商在確保符合當地建築規範的同時,還能透過捆綁相關產品來幫助簡化計劃執行流程。

美國吸音板市場預計到2025年將達到22億美元,2026年至2035年的複合年成長率(CAGR)為6.6%。持續的商業、公共和綜合用途建築的建設和維修需求是推動市場成長的主要動力。對辦公大樓、醫療設施、教育機構、飯店基礎設施和公共建築的投資,推動了吸音板的應用,以改善室內環境品質、語音清晰度和居住者舒適度。此外,提高老舊商業建築的聲學性能也是翻新維修的首要任務,以滿足現代建築規範和職場的需求。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 對噪音控制和隔音的需求日益成長

- 商業建築和維修活動的成長

- 娛樂、媒體和內容製作產業的擴張

- 越來越重視永續和環保產品

- 產業潛在風險與挑戰

- 優質吸音板的初始成本較高

- 終端使用者缺乏意識和技術理解

- 機會

- 擴大綠建築與永續建築

- 來自住宅和在家工作領域的需求增加

- 客製化和架構整合的機會

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 2022-2035年按產品分類的市場估算與預測

- 木質吸音板

- 穿孔人造板

- 木纖維複合板

- 礦棉吸音板

- 高性能礦物棉(NRC熱阻係數>0.85)

- 標準性能礦物棉(NRC 0.65-0.85)

- 特製礦物棉(防火防潮)

- 織物吸音板

- 自訂裝飾系統

- 標準軟墊面板

- 聚酯吸音板

- 智慧物聯網聲學面板

第6章 按設備類型分類的市場估算與預測,2022-2035年

- 壁掛式吸音板

- 直接安裝系統

- 浮動面板系統

- 天花板吸音板

- 嵌入式天花板片

- 直裝式天花板面板

- 吊掛式和專用系統

- 吊掛式的擋板和雲

- 弧形和雕塑狀系統

- 模組化和整合系統

- 可拆卸隔板系統

- 一體化家具解決方案

第7章 按應用領域分類的市場估算與預測,2022-2035年

- 醫療保健設施

- 醫院和醫療中心

- 診斷中心和檢查室

- 老年護理和復健設施

- 教學環境

- 小學和中學以及教室

- 高等教育機構和大學

- 圖書館與學習中心

- 商業和公司

- 辦公大樓和工作空間

- 客服中心和客戶服務

- 會議和會展設施

- 飯店和娛樂

- 飯店和度假村

- 餐廳及食品服務

- 娛樂和劇院

- 工業和製造業

- 製造工廠

- 資料中心和伺服器機房

- 研究與開發設施

- 交通基礎設施

- 機場和交通樞紐

- 汽車和鐵路應用

第8章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 經銷商網路

- 專業零售商

- 線上和數位管道

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Armstrong World Industries, Inc.

- BASF SE

- Beijing New Building Material(Group)Co., Ltd.(BNBM)

- CertainTeed

- Ecophon Group

- Hunter Douglas NV

- Kingspan Group

- Knauf Insulation

- Owens Corning

- Quietstone UK Ltd

- Rockwool International A/S

- Saint-Gobain SA

- Troldtekt A/S

- USG Corporation

- Vicoustic

The Global Acoustic Panel Market was valued at USD 8.6 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 16.4 billion by 2035.

The increasing pace of urbanization and higher population density in cities are contributing to elevated noise levels in residential and commercial environments. As urban noise intensifies, the need for effective sound control solutions has become more critical than ever. The World Health Organization highlights noise as a major environmental health risk, with prolonged exposure linked to stress, disrupted sleep, cardiovascular issues, and other health complications. Growing awareness of these impacts has led to a surge in the adoption of acoustic panels. These panels are widely used in offices, homes, schools, hospitals, and public spaces to absorb sound, reduce reverberation, and enhance indoor acoustic comfort. Additionally, the expansion of commercial construction and renovation projects has fueled demand, as modern buildings increasingly prioritize acoustic quality alongside design and functionality. Manufacturers are responding by offering panels that meet strict performance, aesthetic, and sustainability requirements, creating a dynamic market environment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.6 Billion |

| Forecast Value | $16.4 Billion |

| CAGR | 6.7% |

The specialty mineral wool segment reached USD 3.4 billion in 2025 and is expected to grow at a CAGR of 7% from 2026 to 2035. Governments and regulatory authorities are enforcing stricter fire safety standards across commercial, institutional, and high-density residential sectors, particularly in airports, hospitals, educational facilities, hotels, data centers, and transportation hubs. Mineral wool's non-combustible properties, typically achieving Euroclass A1 or equivalent fire ratings, position it as a highly preferred material for these applications. The segment benefits from its inherent fire resistance, thermal stability, and acoustic performance, aligning with evolving safety regulations and sustainability goals.

The distributor networks segment held 38.8% share and is projected to maintain a CAGR of 6.7% through 2035. These networks offer extensive geographic reach, deep market knowledge, and established relationships with architects, contractors, interior designers, and facility managers. Distributors play a crucial role in large-scale construction and renovation projects, providing timely availability, technical guidance, and after-sales support. With acoustic panels requiring customization for fire resistance, moisture control, NRC ratings, and design finishes, distributors help ensure compliance with local building codes while bundling complementary products to streamline project execution.

U.S. Acoustic Panel Market generated USD 2.2 billion in 2025 and is projected to grow at a CAGR of 6.6% from 2026 to 2035. Strong growth is fueled by ongoing construction and renovation across commercial, institutional, and mixed-use buildings. Investments in office complexes, healthcare facilities, educational institutions, hospitality infrastructure, and public buildings are driving the adoption of acoustic panels to improve indoor environmental quality, speech intelligibility, and occupant comfort. Additionally, renovations of aging commercial structures are prioritizing acoustic performance upgrades to align with modern building standards and workplace expectations.

Key players in the Global Acoustic Panel Market include Saint-Gobain S.A., Armstrong World Industries, Inc., Knauf Insulation, BASF SE, Quietstone UK Ltd, Vicoustic, Hunter Douglas N.V., Rockwool International A/S, USG Corporation, CertainTeed, Beijing New Building Material (Group) Co., Ltd. (BNBM), Troldtekt A/S, Kingspan Group, Owens Corning, and Ecophon Group. Companies in the acoustic panel market are strengthening their foothold by prioritizing innovation in materials and panel designs, including fire-rated, moisture-resistant, and eco-friendly solutions. Strategic partnerships with architects, contractors, and distributors allow them to expand market penetration and accelerate adoption across commercial and institutional projects. Many firms are also investing in digital design tools and acoustical modeling to offer application-specific solutions that optimize performance while meeting local building codes. Geographic expansion, enhanced technical support, and bundled product offerings are additional strategies driving brand recognition and long-term customer loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Installation

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for noise control and soundproofing

- 3.2.1.2 Growth in commercial construction and renovation activities

- 3.2.1.3 Expansion of entertainment, media, and content creation industries

- 3.2.1.4 Increasing emphasis on sustainable and eco-friendly products

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost of premium acoustic panels

- 3.2.2.2 Limited awareness and technical understanding among end users

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of green buildings and sustainable construction

- 3.2.3.2 Rising demand from residential and home office segments

- 3.2.3.3 Customization and architectural integration opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Wooden acoustic panel

- 5.2.1 Perforated wood panels

- 5.2.2 Wood fiber composite panels

- 5.3 Mineral wool acoustic panel

- 5.3.1 High-performance mineral wool (NRC >0.85)

- 5.3.2 Standard performance mineral wool (NRC 0.65-0.85)

- 5.4 Specialty mineral wool (Fire-rated, Moisture-resistant)

- 5.4.1 Fabric acoustic panel

- 5.4.2 Custom decorative systems

- 5.4.3 Standard fabric-wrapped panels

- 5.5 Polyester acoustic panel

- 5.6 Smart and IoT-enabled acoustic panels

Chapter 6 Market Estimates & Forecast, By Installation, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Wall-mounted acoustic panels

- 6.2.1 Direct-mount systems

- 6.2.2 Floating panel systems

- 6.3 Ceiling acoustic panels

- 6.3.1 Drop-in ceiling tiles

- 6.3.2 Direct-mount ceiling panels

- 6.4 Suspended and specialty systems

- 6.4.1 Hanging baffles and clouds

- 6.4.2 Curved and sculptural systems

- 6.5 Modular and integrated systems

- 6.5.1 Demountable partition systems

- 6.5.2 Integrated furniture solutions

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Healthcare and medical facilities

- 7.2.1 Hospitals and medical centers

- 7.2.2 Diagnostic centers and laboratories

- 7.2.3 Elderly care and rehabilitation facilities

- 7.3 Education and learning environments

- 7.3.1 K-12 schools and classrooms

- 7.3.2 Higher education and universities

- 7.3.3 Libraries and study centers

- 7.4 Commercial and corporate

- 7.4.1 Office buildings and workspaces

- 7.4.2 Call centers and customer service

- 7.4.3 Meeting and conference facilities

- 7.5 Hospitality and entertainment

- 7.5.1 Hotels and resorts

- 7.5.2 Restaurants and dining

- 7.5.3 Entertainment venues and theaters

- 7.6 Industrial and manufacturing

- 7.6.1 Manufacturing facilities

- 7.6.2 Data centers and server rooms

- 7.6.3 Research and development facilities

- 7.7 Transportation infrastructure

- 7.7.1 Airports and transit hubs

- 7.7.2 Automotive and railway applications

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Distributor networks

- 8.4 Specialty retailers

- 8.5 Online and digital channels

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Armstrong World Industries, Inc.

- 10.2 BASF SE

- 10.3 Beijing New Building Material (Group) Co., Ltd. (BNBM)

- 10.4 CertainTeed

- 10.5 Ecophon Group

- 10.6 Hunter Douglas N.V.

- 10.7 Kingspan Group

- 10.8 Knauf Insulation

- 10.9 Owens Corning

- 10.10 Quietstone UK Ltd

- 10.11 Rockwool International A/S

- 10.12 Saint-Gobain S.A.

- 10.13 Troldtekt A/S

- 10.14 USG Corporation

- 10.15 Vicoustic

聚乙烯絕緣材料市場規模、佔有率和成長分析(按類型、材料類型、應用、最終用途產業和地區分類)-2026-2033年產業預測

聚乙烯絕緣材料市場規模、佔有率和成長分析(按類型、材料類型、應用、最終用途產業和地區分類)-2026-2033年產業預測 全球隔音市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球隔音市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球隔音材料市場報告

2026年全球隔音材料市場報告 外牆複合隔熱系統市場-全球產業規模、佔有率、趨勢、機會及預測(依材料類型、應用、通路、地區及競爭格局分類,2021-2031年)

外牆複合隔熱系統市場-全球產業規模、佔有率、趨勢、機會及預測(依材料類型、應用、通路、地區及競爭格局分類,2021-2031年) NVH隔音材料市場按材料類型、應用、車輛類型和分銷管道分類-2026-2032年全球預測吸音天花板擋板市場按產品類型、材料類型、安裝方式、分銷管道、應用和最終用戶行業分類,全球預測(2026-2032年)吸音織物面板市場:按產品類型、材料、吸音性能、安裝類型、最終用戶和分銷管道分類,全球預測,2026-2032年外牆保溫一體化板材市場:按類型、材質、應用、通路、厚度和密度分類-2026-2032年全球預測室內吸音板市場按材料類型、安裝類型、密度等級、板材厚度、應用和最終用途分類,全球預測(2026-2032年)室內吸音板市場:依產品類型、材質類型、安裝類型、應用、最終用戶和分銷管道分類-2026-2032年全球預測

NVH隔音材料市場按材料類型、應用、車輛類型和分銷管道分類-2026-2032年全球預測吸音天花板擋板市場按產品類型、材料類型、安裝方式、分銷管道、應用和最終用戶行業分類,全球預測(2026-2032年)吸音織物面板市場:按產品類型、材料、吸音性能、安裝類型、最終用戶和分銷管道分類,全球預測,2026-2032年外牆保溫一體化板材市場:按類型、材質、應用、通路、厚度和密度分類-2026-2032年全球預測室內吸音板市場按材料類型、安裝類型、密度等級、板材厚度、應用和最終用途分類,全球預測(2026-2032年)室內吸音板市場:依產品類型、材質類型、安裝類型、應用、最終用戶和分銷管道分類-2026-2032年全球預測