|

市場調查報告書

商品編碼

1936540

液體包裝市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Liquid Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

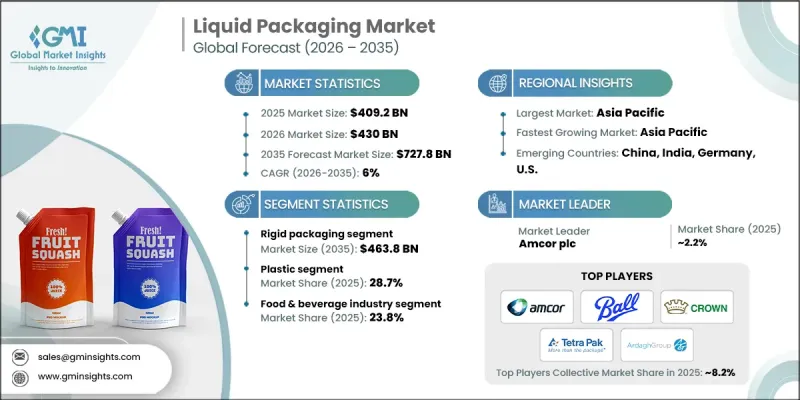

全球液體包裝市場預計到 2025 年將達到 4,092 億美元,到 2035 年將達到 7,278 億美元,年複合成長率為 6%。

市場成長的驅動力來自食品、飲料、醫藥和消費品領域對安全、便利且環保的包裝解決方案日益成長的需求。已開發經濟體和新興經濟體預包裝液體的消費量持續成長,進一步推動了市場需求,而與永續性相關的監管壓力正在重塑材料選擇和包裝設計。隨著製造商不斷調整以滿足消費者對輕巧、耐用和可回收包裝形式的偏好,市場格局正在迅速變化。材料科學和生產效率的進步使企業能夠在保持性能標準的同時減輕包裝重量。電子商務的成長進一步推動了對能夠承受複雜物流和配送網路的液體保護性包裝的需求。同時,包裝供應商正在採用智慧、可追溯的包裝解決方案,以提高產品透明度、加強供應鏈監管並提升品牌信任。這些發展,加上成本最佳化和永續性目標,正在加速全球的普及,並重塑長期市場動態。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 4092億美元 |

| 預測金額 | 7278億美元 |

| 複合年成長率 | 6% |

預計到2035年,硬質包裝市場規模將達到4,638億美元。該市場憑藉其結構強度高、保存期限長以及消費者對從高階到大眾市場液體產品等各類產品的廣泛認可,持續保持強勁的市場地位。材料工程的進步使製造商能夠在保持包裝耐用性和性能的同時,減輕包裝的整體重量。這些優勢有助於提高填充效率、簡化運輸流程並確保產品品質的穩定性,從而使硬質包裝繼續成為大規模生產和分銷的首選。

到2025年,塑膠包裝市佔率將達到28.7%,並在2035年之前維持6.5%的複合年成長率。其持續佔據主導地位主要得益於成本效益、多功能性以及與高速生產系統的兼容性。製造商青睞塑膠包裝解決方案,因為它們能夠在擴大生產規模的同時保持穩定的品質標準。這些優勢促使塑膠包裝在各種液體應用領域中廣泛應用,從而鞏固了塑膠在全球包裝生態系統中的核心材料地位。

預計到2025年,北美液體包裝市場規模將達到881億美元。該地區受益於成熟的消費市場、先進的製造基礎設施以及對包裝創新持續不斷的投資。強大的包裝製造商、材料供應商和品牌所有者網路積極支持永續設計、提升阻隔性能以及實用化高效填充技術。這些因素共同推動了北美對全球市場擴張的貢獻。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 永續阻隔塗層的應用日益廣泛

- 消費者越來越偏好小包裝尺寸

- 電子商務的興起正在推動對先進液體包裝解決方案的需求。

- 物聯網和即時物流感測器整合推動液體包裝領域的創新

- 提升客戶體驗正在推動用戶友善液體包裝的普及。

- 產業潛在風險與挑戰

- 關鍵原料成本上漲影響液體包裝市場

- 回收基礎設施不足阻礙了液體包裝市場的成長

- 市場機遇

- 利用即時供應鏈洞察和數據驅動的預測規劃來改善分銷和效率

- 智慧倉儲管理和機器人技術:最佳化液體包裝安全性和效率的策略性機會

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 歷史價格分析(2022-2025)

- 價格趨勢背後的因素

- 區域價格波動

- 價格預測(2026-2035)

- 定價策略

- 新興經營模式

- 合規要求

- 永續性措施

- 永續材料評估

- 碳足跡分析

- 採取循環經濟模式

- 永續性認證和標準

- 永續性投資報酬率分析

- 全球消費者心理分析

- 專利分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 地理分佈比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2022-2025 年主要發展動態

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張與投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競賽的趨勢

5. 液體包裝市場按類型分類的估算與預測,2022-2035年

- ,

- 軟包裝

- 硬包裝

6. 液體包裝市場依材料分類的估算與預測,2022-2035年

- 塑膠

- 紙和紙板

- 玻璃

- 金屬

- 其他

7. 2022-2035年按終端用戶產業分類的液體包裝市場估算與預測

- 食品/飲料

- 個人護理

- 製藥

- 家居用品

- 工業的

- 其他

8. 2022-2035年各地區液體包裝市場估計與預測

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章

- 安姆公司

- 波爾公司

- 皇冠控股有限公司

- 利樂國際有限公司

- 阿達格集團

- 歐文斯伊利諾伊玻璃公司(OI玻璃)

- SIG Combiblock Group AG

- 埃爾奧帕克

- 大景無菌包裝有限公司

- 常青包裝有限公司

- 斯道拉恩索株式會社

- 日本製紙株式會社

- 斯莫菲卡帕Group Limited

- 韋斯特羅克公司

- 國際紙業公司

- ALPLA集團

- 富田卷株式會社

- Rikibox 公司

- 科默有限責任公司

The Global Liquid Packaging Market was valued at USD 409.2 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 727.8 billion by 2035.

Market growth is supported by rising demand for packaging solutions that ensure safety, convenience, and environmental responsibility across food, beverage, pharmaceutical, and consumer product applications. Increasing consumption of packaged liquids in both developed and emerging economies continues to drive demand, while regulatory pressure related to sustainability is reshaping material selection and packaging design. The market landscape is evolving rapidly as manufacturers respond to consumer preferences for lightweight, durable, and recyclable packaging formats. Advances in material science and production efficiency are enabling companies to reduce packaging weight while maintaining performance standards. The growth of e-commerce has further increased the need for protective liquid packaging capable of withstanding complex logistics and distribution networks. In parallel, packaging suppliers are adopting intelligent and traceable packaging solutions that enhance product transparency, improve supply chain monitoring, and reinforce brand trust. These developments, combined with cost optimization and sustainability goals, are accelerating global adoption and reshaping long-term market dynamics.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $409.2 Billion |

| Forecast Value | $727.8 Billion |

| CAGR | 6% |

The rigid packaging segment is expected to generate USD 463.8 billion by 2035. This segment continues to maintain a strong position due to its structural strength, long shelf-life protection, and strong consumer acceptance across premium and mass-market liquid products. Improvements in material engineering have enabled manufacturers to reduce overall packaging weight while preserving durability and performance. These characteristics support efficient filling processes, streamlined transportation, and consistent product quality, allowing rigid formats to remain a preferred choice for large-scale production and distribution.

The plastic segment held 28.7% share in 2025 and is growing at a CAGR of 6.5% through 2035. Its continued dominance is supported by cost efficiency, versatility, and compatibility with high-speed manufacturing systems. Manufacturers favor plastic-based solutions for their ability to support scalable production while maintaining consistent quality standards. These advantages contribute to widespread adoption across a broad range of liquid applications, reinforcing plastic's role as a core material in the global packaging ecosystem.

North America Liquid Packaging Market generated USD 88.1 billion in 2025. The region benefits from mature consumer markets, advanced manufacturing infrastructure, and sustained investment in packaging innovation. A robust network of packaging producers, material suppliers, and brand owners actively supports the development of sustainable designs, enhanced barrier performance, and efficient filling technologies. These factors collectively strengthen North America's contribution to global market expansion.

Key participants in the Global Liquid Packaging Industry include Tetra Pak International SA, Amcor plc, SIG Combibloc Group AG, Ball Corporation, Ardagh Group, Crown Holdings, Inc., ALPLA Group, O-I Glass (Owens-Illinois), WestRock Company, International Paper Company, Huhtamaki Oyj, Smurfit Kappa Group plc, Elopak AS, Evergreen Packaging Inc., Stora Enso Oyj, Greatview Aseptic Packaging Co., and Nippon Paper Industries Co., Ltd. Companies operating in the liquid packaging market are strengthening their competitive position through sustainability-driven innovation, capacity expansion, and strategic collaboration. Leading players are investing in recyclable and lightweight material technologies to align with regulatory requirements and consumer expectations. Many firms are enhancing production efficiency through automation and digitalization while expanding global manufacturing footprints to serve high-growth regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Material trends

- 2.2.3 End Use Industries trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of sustainable barrier coatings.

- 3.2.1.2 Growing consumer preference for smaller pack sizes.

- 3.2.1.3 E-commerce expansion is driving demand for advanced liquid packaging solutions.

- 3.2.1.4 Integration of IoT and real-time logistics sensors driving innovation in liquid packaging.

- 3.2.1.5 Customer experience enhancement driving adoption of user-friendly liquid packaging.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising costs of key raw materials impacting the liquid packaging market

- 3.2.2.2 Limited recycling infrastructure hindering growth of the liquid packaging market

- 3.2.3 Market opportunities

- 3.2.4 Leveraging real-time supply-chain insights and data-driven predictive planning to enhance distribution and efficiency.

- 3.2.5 Smart warehousing and robotics as a strategic opportunity to optimize safety and efficiency in liquid packaging.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2025)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability roi analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Liquid Packaging Market Estimates & Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends,

- 5.2 Flexible packaging

- 5.3 Rigid packaging

Chapter 6 Liquid Packaging Market Estimates and Forecast, By Materials, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Paper & boards

- 6.4 Glass

- 6.5 Metal

- 6.6 Others

Chapter 7 Liquid Packaging Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Personal care

- 7.4 Pharmaceutical

- 7.5 Household care

- 7.6 Industrial

- 7.7 Others

Chapter 8 Liquid Packaging Market Estimates & Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends, by region

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Rest of Europe

- 8.4 Asia-Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Rest of Asia-Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9

- 9.1 Amcor plc

- 9.2 Ball Corporation

- 9.3 Crown Holdings, Inc.

- 9.4 Tetra Pak International SA

- 9.5 Ardagh Group

- 9.6 O-I Glass (Owens-Illinois)

- 9.7 SIG Combibloc Group AG

- 9.8 Elopak AS

- 9.9 Greatview Aseptic Packaging Co.

- 9.10 Evergreen Packaging Inc.

- 9.11 Stora Enso Oyj

- 9.12 Nippon Paper Industries Co., Ltd.

- 9.13 Smurfit Kappa Group plc

- 9.14 WestRock Company

- 9.15 International Paper Company

- 9.16 ALPLA Group

- 9.17 Huhtamaki Oyj

- 9.18 Liqui-Box Corporation

- 9.19 Comar LLC

液體包裝市場分析及預測(至2035年):依類型、產品類型、材質、技術、應用、最終用戶、製程、功能、安裝類型、解決方案分類

液體包裝市場分析及預測(至2035年):依類型、產品類型、材質、技術、應用、最終用戶、製程、功能、安裝類型、解決方案分類 全球液體包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球立方體收納箱市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球液體包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球立方體收納箱市場規模、佔有率、趨勢和成長分析報告(2026-2034) 液體包裝市場規模、佔有率、趨勢及預測(按材料類型、包裝類型、技術、最終用戶和地區分類),2026-2034年

液體包裝市場規模、佔有率、趨勢及預測(按材料類型、包裝類型、技術、最終用戶和地區分類),2026-2034年 2026年全球液體包裝市場報告

2026年全球液體包裝市場報告 潤滑油包裝市場規模、佔有率和成長分析(按產品類型、包裝類型、材料、最終用途產業和地區分類)-2026-2033年產業預測

潤滑油包裝市場規模、佔有率和成長分析(按產品類型、包裝類型、材料、最終用途產業和地區分類)-2026-2033年產業預測 2025-2032 年全球預測:立方容器市場(按包裝袋類型、盒子材質、閥門類型、包裝袋材質、容量和應用)傑瑞罐市場材料類型、最終用途產業、應用、銷售管道和應用分類-2025-2030 年全球預測

2025-2032 年全球預測:立方容器市場(按包裝袋類型、盒子材質、閥門類型、包裝袋材質、容量和應用)傑瑞罐市場材料類型、最終用途產業、應用、銷售管道和應用分類-2025-2030 年全球預測 全球果凍市場液體包裝市場(依包裝、應用、材料、技術及地區)預測(2026-2032 年)

全球果凍市場液體包裝市場(依包裝、應用、材料、技術及地區)預測(2026-2032 年)