|

市場調查報告書

商品編碼

1936527

機器人即服務 (RaaS) 市場機會、成長要素、產業趨勢分析及預測(2026-2035 年)Robotics as a Service (RaaS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

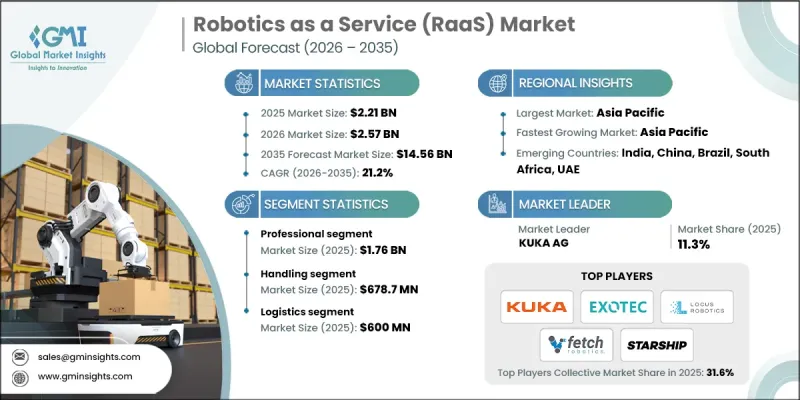

全球機器人即服務市場預計到 2025 年將達到 22.1 億美元,到 2035 年將達到 145.6 億美元,年複合成長率為 21.2%。

推動這一擴張的因素有很多,包括物流、製造和醫療保健行業嚴重的勞動力短缺,以及企業日益成長的從資本密集型投資模式轉向營運支出模式的需求。人工智慧、雲端機器人和自主導航技術的快速發展為遠端操控機器人集群奠定了實際的基礎,而遠端操控機器人集群正是機器人即服務 (RaaS) 模式的基石。即時效能追蹤、集中式軟體更新和自適應學習使服務供應商能夠有效管理分散式機器人,從而減少停機時間和維護成本,同時提高可靠性。基於訂閱、以結果為導向的方法為企業提供擴充性、柔軟性且隨選的自動化解決方案,使其具有商業性吸引力。企業越來越依賴 RaaS 來維持營運連續性、最佳化生產力,並在無需漫長招募週期的情況下執行重複性或高離職率的任務。人工智慧、互聯互通和智慧軟體整合的融合進一步強化了對自動化的關注,使 RaaS 成為現代工業效率的關鍵驅動力。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 22.1億美元 |

| 預測金額 | 145.6億美元 |

| 複合年成長率 | 21.2% |

預計2025年,專業機器人市場規模將達到17.6億美元。面對技術純熟勞工短缺和提高生產力的壓力,企業正在積極採用專業機器人。物流、醫療保健和製造業等行業尤其增加對機器人系統的投資,以維持業務連續性、提高效率並減少對專業人才的依賴。訂閱式機器人服務正成為管理勞力密集流程、確保穩定生產且不影響效能的實用解決方案。

預計到2025年,搬運設備市場規模將達到6.787億美元。物流自動化是推動這項需求的主要因素,倉庫和配銷中心擴大採用訂閱式機器人服務來運輸貨物、減少錯誤、提高吞吐量,並緩解高峰期的人員短缺問題。先進的感測器和軟體使自主移動機器人能夠安全且有效率地搬運更重的貨物,從而以較低的總成本為企業提供可靠的解決方案。

預計到2025年,北美將佔據機器人即服務(RaaS)市場36.8%的佔有率,成為RaaS領域競爭最激烈的地區。美國和加拿大已建立起完善的技術生態系統,促進了自主移動機器人的快速普及,從而降低勞動成本並提高營運效率。該地區擁有廣泛的數位基礎設施和創新網路,為服務導向的機器人技術提供支持,並可在物流、醫療保健和智慧工廠等商業應用中實現可擴展的訂閱式解決方案。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 物流、製造業和醫療領域勞動力短缺問題日益嚴重

- 從資本支出模式轉向營運支出模式

- 人工智慧、雲端機器人和自主導航技術的快速發展

- 對擴充性、柔軟性的自動化解決方案的需求

- 基於績效和訂閱的經營模式正日益普及

- 陷阱與挑戰

- 複雜用例的初始服務價格較高

- 資料安全、保障和合規性問題

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 永續發展計劃

- 供應鏈韌性

- 地緣政治分析

- 數位轉型

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 按地區分類的企業發展比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 產品系列比較

- 2022-2025 年主要發展動態

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張與投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競賽的趨勢

第5章 按類型分類的市場估算與預測,2022-2035年

- 面向專業人士

- 對於個人

第6章 按應用領域分類的市場估算與預測,2022-2035年

- 處理

- 組裝

- 自動販賣機

- 加工

- 焊接和釬焊

- 其他

7. 2022-2035年按最終用途產業分類的市場估算與預測

- 製造業

- 車

- 食品/飲料

- 後勤

- 衛生保健

- 零售

- 其他

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- 主要企業

- Locus Robotics

- Fetch Robotics

- Sarcos Robotics

- 6 River Systems

- Exotec

- 按地區分類的主要企業

- 北美洲

- Aethon

- Savioke

- Cobalt Robotics

- Knightscope

- 歐洲

- Starship Technologies

- Sofigate

- Marble

- 亞太地區

- Liquid Robotics

- inVia Robotics

- 北美洲

- 小眾/顛覆性公司

- Bossa Nova Robotics

- PrecisionHawk

- RedZone Robotics

- Hirebotics

- Fellow Robots

- Glomatriz

The Global Robotics as a Service Market was valued at USD 2.21 billion in 2025 and is estimated to grow at a CAGR of 21.2% to reach USD 14.56 billion by 2035.

The expansion is driven by multiple factors, including acute labor shortages across logistics, manufacturing, and healthcare sectors, and the increasing preference for shifting from capital-intensive investments to operating expenditure models. Rapid advancements in artificial intelligence, cloud robotics, and autonomous navigation technologies have created viable frameworks for remotely controlled robot fleets, which form the foundation of the RaaS model. Real-time performance tracking, centralized software updates, and adaptive learning not only reduce downtime and service costs but also improve reliability, enabling service providers to manage distributed robots efficiently. The subscription-based, outcome-oriented approach has become commercially attractive, offering businesses scalable, flexible, and on-demand automation solutions. Organizations increasingly rely on RaaS to maintain operational continuity, optimize productivity, and tackle repetitive or high-turnover tasks without the burden of long recruitment cycles. This growing emphasis on automation is reinforced by the convergence of AI, connectivity, and smart software integration, making RaaS a key driver of efficiency in modern industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.21 Billion |

| Forecast Value | $14.56 Billion |

| CAGR | 21.2% |

The professional segment was valued at USD 1.76 billion in 2025. Companies facing skilled labor shortages and productivity pressures are driving the adoption of professional robotics. Industries such as logistics, healthcare, and manufacturing are particularly invested in robotic systems to maintain operational continuity, improve efficiency, and reduce reliance on specialized personnel. Subscription-based robotic services are becoming a practical solution for managing labor-intensive processes and ensuring consistent output without compromising on performance.

The handling segment generated USD 678.7 million in 2025. Logistics automation is a significant driver of this demand, as warehouses and distribution centers increasingly deploy robots on a subscription basis to transport goods, minimize errors, increase throughput, and fill staffing gaps during peak periods. Advanced sensors and software enable autonomous mobile robots to move heavier loads safely and efficiently, offering businesses dependable solutions at a lower total cost.

North America Robotics as a Service Market held a 36.8% share in 2025, making it the most competitive region for RaaS. The U.S. and Canada have established technology ecosystems that facilitate the rapid adoption of autonomous mobile robots to reduce labor costs and enhance operational efficiency. The region benefits from extensive digital infrastructure and innovation networks that support service-oriented robotics and enable scalable subscription-based solutions in commercial applications across logistics, healthcare, and smart factories.

Key players in the Global Robotics as a Service Market include Fetch Robotics, Locus Robotics, Starship Technologies, 6 River Systems, Sarcos Robotics, Glomatriz, Savioke, Bossa Nova Robotics, Liquid Robotics, inVia Robotics, PrecisionHawk, Fellow Robots, Cobalt Robotics, Knightscope, RedZone Robotics, Marble, Hirebotics, Exotec, Sofigate, and Aethon. Companies in the Global Robotics as a Service (RaaS) Market strengthen their presence by focusing on advanced technology integration, service scalability, and strategic partnerships. Providers invest heavily in AI-driven navigation, cloud connectivity, and remote fleet management software to enhance robot efficiency and reduce downtime. They expand their footprint by collaborating with logistics, manufacturing, and healthcare operators to tailor solutions for industry-specific needs. Subscription-based pricing models, flexible deployment options, and outcome-oriented offerings attract cost-conscious clients.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Application trends

- 2.2.3 End-use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising labor shortages across logistics, manufacturing, and healthcare

- 3.2.1.2 Shift from capital expenditure to operating expenditure models

- 3.2.1.3 Rapid advancements in AI, cloud robotics, and autonomous navigation

- 3.2.1.4 Demand for scalable and flexible automation solutions

- 3.2.1.5 Growing adoption of outcome-based and subscription business models

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High initial service pricing for complex use cases

- 3.2.2.2 Data security, safety, and regulatory compliance concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Professional

- 5.3 Personal

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Handling

- 6.3 Assembling

- 6.4 Dispensing

- 6.5 Processing

- 6.6 Welding & Soldering

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Manufacturing

- 7.3 Automotive

- 7.4 Food & beverage

- 7.5 Logistics

- 7.6 Healthcare

- 7.7 Retail

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Locus Robotics

- 9.1.2 Fetch Robotics

- 9.1.3 Sarcos Robotics

- 9.1.4 6 River Systems

- 9.1.5 Exotec

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Aethon

- 9.2.1.2 Savioke

- 9.2.1.3 Cobalt Robotics

- 9.2.1.4 Knightscope

- 9.2.2 Europe

- 9.2.2.1 Starship Technologies

- 9.2.2.2 Sofigate

- 9.2.2.3 Marble

- 9.2.3 Asia Pacific

- 9.2.3.1 Liquid Robotics

- 9.2.3.2 inVia Robotics

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Bossa Nova Robotics

- 9.3.2 PrecisionHawk

- 9.3.3 RedZone Robotics

- 9.3.4 Hirebotics

- 9.3.5 Fellow Robots

- 9.3.6 Glomatriz

RaaS市場 - 全球預測,2026-2032年

RaaS市場 - 全球預測,2026-2032年 機器人即服務 (RaaS) 市場規模、佔有率和成長分析:按機器人類型、服務模式、應用、組織規模和地區分類—2026-2033 年產業預測

機器人即服務 (RaaS) 市場規模、佔有率和成長分析:按機器人類型、服務模式、應用、組織規模和地區分類—2026-2033 年產業預測 2026年機器人金融即服務全球市場報告

2026年機器人金融即服務全球市場報告 機器人即服務 (RaaS) 市場預測至 2034 年——按服務類型、機器人類型、應用、最終用戶和地區分類的全球分析

機器人即服務 (RaaS) 市場預測至 2034 年——按服務類型、機器人類型、應用、最終用戶和地區分類的全球分析 機器人即服務 (RaaS) 市場:按類型、最終用戶產業和地區分類2026年全球機器人即服務(RaaS)市場報告

機器人即服務 (RaaS) 市場:按類型、最終用戶產業和地區分類2026年全球機器人即服務(RaaS)市場報告 亞太地區機器人即服務 (RaaS) 市場按應用程式、最終用戶、類型和國家分類 - 分析與預測 (2025-2035)

亞太地區機器人即服務 (RaaS) 市場按應用程式、最終用戶、類型和國家分類 - 分析與預測 (2025-2035) 歐洲機器人即服務 (RaaS) 市場按應用程式、最終用戶、類型和國家/地區分類 - 分析和預測 (2025-2035)

歐洲機器人即服務 (RaaS) 市場按應用程式、最終用戶、類型和國家/地區分類 - 分析和預測 (2025-2035) 全球機器人即服務 (RaaS) 市場:按應用、最終用戶、產品和國家分類的分析和預測 (2025-2035)

全球機器人即服務 (RaaS) 市場:按應用、最終用戶、產品和國家分類的分析和預測 (2025-2035) 全球機器人即服務市場

全球機器人即服務市場