|

市場調查報告書

商品編碼

1936520

奢侈皮革製品市場機會、成長要素、產業趨勢分析及2026年至2035年預測Luxury Leather Goods Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

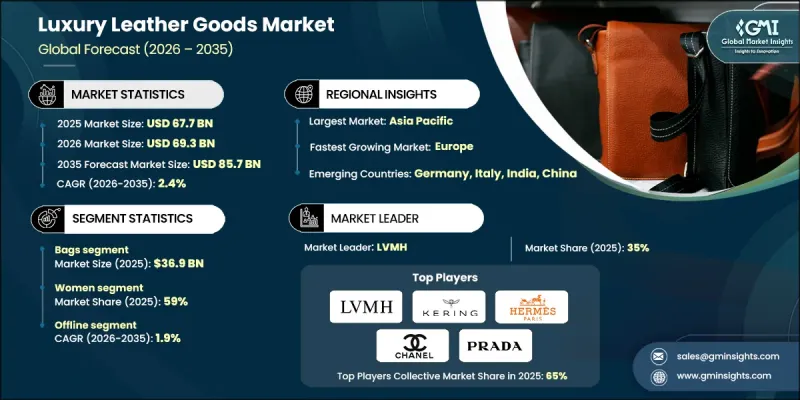

全球奢侈皮革製品市場預計到 2025 年將達到 677 億美元,到 2035 年將達到 857 億美元,年複合成長率為 2.4%。

市場成長主要受新興經濟體消費者對高階生活方式產品需求不斷成長和消費支出增加的推動。相關人員對環保生活方式的偏好轉變也影響著他們的購買決策,進而推動了對永續採購和負責任生產的皮革製品的需求。業內企業正積極投資於產品創新和品牌差異化,以滿足不斷變化的消費者期望。皮革加工和生產技術的進步提升了產品的耐用性、美觀性和整體品質,進一步促進了市場擴張。數位商務平台繼續發揮關鍵作用,擴大了品牌的覆蓋範圍,使其能夠進入先前服務不足的市場。線上通路帶來的便利性和消費者意識的提升正在增強全球需求。在供應方面,全球貿易持續強勁成長,印度作為皮革服裝、馬具、挽具和成品皮革製品的主要出口國,佔有重要地位。服裝佔印度皮革出口總額的6.84%。這些因素共同推動著奢侈皮革製品產業的長期穩定成長。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 677億美元 |

| 預測金額 | 857億美元 |

| 複合年成長率 | 2.4% |

預計到2025年,箱包市場規模將達到3,69億美元,到2035年將以2.7%的複合年成長率成長。該品類的成長主要得益於消費者對奢侈箱包設計的持續關注以及年輕消費群組強勁的需求。此外,數位平台上品牌知名度的不斷提升也持續影響該品類的購買行為。

預計到 2025 年,女性市場將佔 59% 的市場佔有率,並在 2026 年至 2035 年間以 2.6% 的複合年成長率成長。收入水準的提高、對奢侈時尚日益成長的興趣、個性化選擇的增加以及透過電子商務平台獲得的更便捷的購買管道,都是支撐女性消費者(尤其是在新興市場)持續需求的關鍵因素。

預計到2025年,美國奢侈皮具市場將佔77%的市場佔有率,銷售額將達到121億美元。該市場的成長動力主要來自較高的可支配收入水平、對奢侈材料的強勁需求以及有效的數位化品牌互動策略。永續性的產品開發和創新設計理念持續吸引具有環保意識的消費者。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 法律規範

- 標準與認證

- 環境法規

- 進出口限制

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務如何影響購買決策

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 行李箱

- 行李箱和隨身行李

- 背包

- 旅行袋

- 公事包

- 其他(例如週末等)

- 包包

- 手提包

- 托特包

- 離合器

- 斜背包

- 其他(流浪包等)

- 小皮具

- 錢包

- 卡包和卡片夾

- 零錢包

- 其他(重大案件等)

- 其他(服裝等)

第6章 依皮革類型分類的市場估算與預測,2022-2035年

- 真皮

- 珍稀皮革

- 合成皮革

- 混合材料

7. 按最終用戶分類的市場估計和預測,2022-2035 年

- 女士

- 男性

- 男女通用的

第8章 按分銷管道分類的市場估算與預測,2022-2035年

- 線上

- 電子商務

- 公司網站

- 離線

- 超級市場/大賣場

- 專賣店

- 其他(例如,獨立零售商)

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Aspinal of London

- Bottega Veneta

- Burberry

- Capri

- Chanel

- Hermes

- Hugo Boss

- Kering

- LVMH

- Moshi Leather Bag

- Mulberry

- Nappa Dori

- Prada

- Shinola

- Tapestry

The Global Luxury Leather Goods Market was valued at USD 67.7 billion in 2025 and is estimated to grow at a CAGR of 2.4% to reach USD 85.7 billion by 2035.

Market growth is supported by rising demand for premium lifestyle products and higher consumer spending across developing economies. Shifting preferences toward environmentally responsible lifestyles are also influencing purchasing decisions, encouraging demand for sustainably sourced and responsibly manufactured leather goods. Industry participants are actively investing in product innovation and brand differentiation to align with evolving consumer expectations. Advances in leather processing and production technologies have improved product durability, aesthetics, and overall quality, further supporting market expansion. Digital commerce platforms continue to play a critical role by expanding brand reach and enabling access to previously underserved markets. Improved convenience and visibility through online channels are strengthening global demand. On the supply side, global trade performance remains strong, with India holding a significant position as one of the world's leading exporters of leather garments, saddlery, harnesses, and finished leather goods, with garments contributing 6.84% of the country's total leather exports. These combined factors reinforce steady long-term growth across the luxury leather goods industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $67.7 Billion |

| Forecast Value | $85.7 Billion |

| CAGR | 2.4% |

The bags segment generated USD 36.9 billion in 2025 and is expected to grow at a CAGR of 2.7% through 2035. Growth in this category is supported by sustained interest in premium bag designs and strong demand among younger consumer groups. Brand visibility across digital platforms continues to influence purchasing behavior in this segment.

The women segment accounted for 59% share in 2025, with the segment projected to grow at a CAGR of 2.6% from 2026 to 2035. Rising income levels, growing interest in luxury fashion, increased personalization options, and wider access through e-commerce platforms are key contributors to sustained demand among female consumers, particularly in emerging markets.

United States Luxury Leather Goods Market held 77% share and generated USD 12.1 billion in 2025. Market strength is supported by high disposable income levels, strong demand for premium materials, and effective digital brand engagement strategies. Sustainability-focused product development and innovative design approaches continue to attract environmentally aware consumers.

Major companies operating in the Global Luxury Leather Goods Market include LVMH, Chanel, Hermes, Prada, Kering, Burberry, Tapestry, Capri, Hugo Boss, Bottega Veneta, Mulberry, Aspinal of London, Shinola, Nappa Dori, and Moshi Leather Bag. Companies in the luxury leather goods market strengthen their competitive position through brand heritage, product innovation, and sustainability-led strategies. Many players invest in responsible sourcing, eco-friendly materials, and transparent supply chains to appeal to conscious consumers. Limited-edition collections and personalization options help create exclusivity and brand loyalty. Strong digital marketing, social media engagement, and direct-to-consumer channels enhance visibility and global reach. Firms also focus on expanding e-commerce capabilities while maintaining premium in-store experiences.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Leather Type

- 2.2.4 End User

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics (HS code)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Luggage

- 5.2.1 Suitcases & trolleys

- 5.2.2 Backpacks

- 5.2.3 Duffel bags

- 5.2.4 Briefcases

- 5.2.5 Others (weekenders etc.)

- 5.3 Bags

- 5.3.1 Handbags

- 5.3.2 Tote bags

- 5.3.3 Clutches

- 5.3.4 Messenger bags

- 5.3.5 Others (hobo bags etc.)

- 5.4 Small leather goods

- 5.4.1 Wallets

- 5.4.2 Cardholders & card cases

- 5.4.3 Coin purses

- 5.4.4 Others (key cases etc.)

- 5.5 Others (apparel etc.)

Chapter 6 Market Estimates & Forecast, By Leather Type, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Genuine leather

- 6.3 Exotic skins

- 6.4 Synthetic leather

- 6.5 Hybrid materials

Chapter 7 Market Estimates & Forecast, By End User, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Women

- 7.3 Men

- 7.4 Unisex

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Company websites

- 8.3 Offline

- 8.3.1 Supermarkets/hypermarket

- 8.3.2 Specialty retail stores

- 8.3.3 Others (independent retailer etc.)

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aspinal of London

- 10.2 Bottega Veneta

- 10.3 Burberry

- 10.4 Capri

- 10.5 Chanel

- 10.6 Hermes

- 10.7 Hugo Boss

- 10.8 Kering

- 10.9 LVMH

- 10.10 Moshi Leather Bag

- 10.11 Mulberry

- 10.12 Nappa Dori

- 10.13 Prada

- 10.14 Shinola

- 10.15 Tapestry

全粒面皮革市場:按類型、產品類型、應用和分銷管道分類-2026-2032年全球市場預測皮革製品市場:2026-2032年全球市場預測(依產品類型、製造流程、等級、材料類型、應用及分銷通路分類)

全粒面皮革市場:按類型、產品類型、應用和分銷管道分類-2026-2032年全球市場預測皮革製品市場:2026-2032年全球市場預測(依產品類型、製造流程、等級、材料類型、應用及分銷通路分類) 皮革製品市場:依產品類型、銷售管道和地區分類箱包及皮革製品市場:按類型、銷售管道及地區分類

皮革製品市場:依產品類型、銷售管道和地區分類箱包及皮革製品市場:按類型、銷售管道及地區分類 皮革製品市場報告:趨勢、預測及競爭分析(至2035年)

皮革製品市場報告:趨勢、預測及競爭分析(至2035年) 皮革製品市場分析及預測(至2035年):類型、產品類型、應用、材料類型、最終用戶、製造流程、技術、功能、安裝類型

皮革製品市場分析及預測(至2035年):類型、產品類型、應用、材料類型、最終用戶、製造流程、技術、功能、安裝類型 全球皮革製品市場規模、佔有率、成長率、按類型和應用分類的全球產業分析、區域趨勢以及 2026-2034 年預測。

全球皮革製品市場規模、佔有率、成長率、按類型和應用分類的全球產業分析、區域趨勢以及 2026-2034 年預測。 皮革製品市場報告:按產品、材料、價格範圍、分銷管道和地區分類,2026-2034年

皮革製品市場報告:按產品、材料、價格範圍、分銷管道和地區分類,2026-2034年 皮革清潔劑和護理劑市場 - 全球產業規模、佔有率、趨勢、機會和預測(按產品類型、應用、銷售管道、地區和競爭格局分類,2021-2031年)

皮革清潔劑和護理劑市場 - 全球產業規模、佔有率、趨勢、機會和預測(按產品類型、應用、銷售管道、地區和競爭格局分類,2021-2031年) 奢侈皮革製品市場規模、佔有率及成長分析(按產品、通路及地區分類)-2026-2033年產業預測

奢侈皮革製品市場規模、佔有率及成長分析(按產品、通路及地區分類)-2026-2033年產業預測