|

市場調查報告書

商品編碼

1936512

電動汽車電池組件市場機會、成長要素、產業趨勢分析及2026年至2035年預測Electric Vehicle (EV) Battery Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

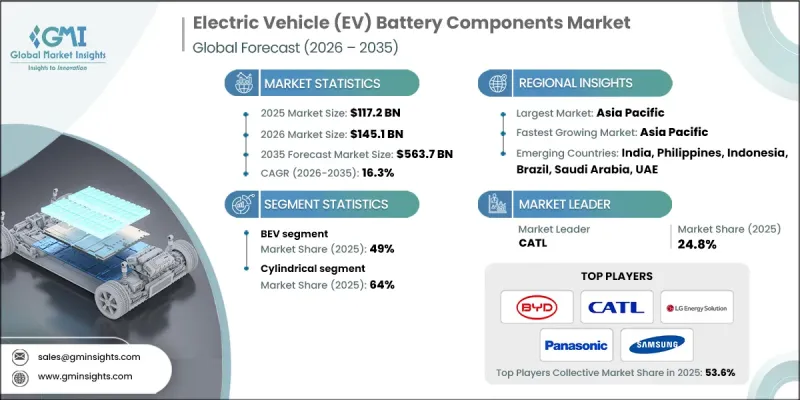

全球電動車電池組件市場預計到 2025 年將達到 1,172 億美元,到 2035 年將達到 5,637 億美元,年複合成長率為 16.3%。

全球電動車的快速普及正在改變汽車動力傳動系統設計,並重塑供應鏈。電池單元、模組、正極、陽極、電池管理系統 (BMS) 和溫度控管解決方案等組件如今已成為決定車輛續航里程、性能、安全性和成本效益的核心要素。隨著汽車製造商從內燃機轉向專用電動車架構,電池系統正日益被視為完全整合的平台,而非獨立的組件,這影響著營運可行性和全生命週期經濟性。汽車製造商、電池製造商、材料供應商和半導體公司之間的大規模投資和策略聯盟進一步推動了市場發展。垂直整合策略,例如內部電池組裝、本地化電池生產以及正負極材料的合資企業,使原始設備製造商 (OEM) 能夠確保供應、降低成本並提高品質。此外,廣泛的組件測試、全生命週期最佳化以及對國際安全標準的遵守,都提高了產品的可靠性、耐久性和熱安全性。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 1172億美元 |

| 預測金額 | 5637億美元 |

| 複合年成長率 | 16.3% |

預計到2025年,電池式電動車(BEV)市場佔有率將達到49%,並在2035年之前以17%的複合年成長率成長。純電動車完全依賴電池動力,因此對高容量電池、模組及相關系統有著強勁的需求,以確保長續航里程、快速充電和穩定的性能。全球範圍內支持零排放汽車的政策和獎勵正在進一步加速純電動車的普及,使其成為市場發展的關鍵驅動力。

預計到2025年,圓柱形電池市佔率將達到64%,並在2026年至2035年間以15.7%的複合年成長率成長。這些電池因其性能可靠、能量密度高、溫度控管出色以及循環壽命長而備受青睞。其模組化設計和標準化尺寸使其能夠無縫整合到電池組中,從而簡化組裝、維護和回收。此外,圓柱形電池還具有更高的安全性、可靠的散熱性能以及在高電流負載下的耐久性,使其成為乘用車和商用電動車應用的首選。

預計到2025年,中國電動車電池零件市場將佔據顯著佔有率。中國快速的工業化進程、強勁的國內電動車需求以及高度整合的供應鏈體系,都為市場的蓬勃發展提供了強力支撐。作為主要的電動車生產中心,中國對電池電芯、正極材料、負極材料、隔膜、電解和外殼等零件的需求持續強勁。中國對上游鋰精煉、正極材料製造和石墨負極材料生產的掌控,確保了成本效益、快速規模生產和穩定的供應。此外,透過與生產連結獎勵計畫和長期產業規劃等政策支持,進一步加速了電池零件各領域的技術應用和產能擴張。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 全球電動乘用車和商用車的普及率不斷提高

- 政府加大獎勵、補助和電動車基礎設施投資

- 電池超級工廠擴建及區域產能擴張

- 物流、公共運輸和車隊車輛電氣化進展

- 產業潛在風險與挑戰

- 關鍵電池原物料高成本且價格波動大

- 缺乏大規模電池回收和廢棄電池處理基礎設施

- 市場機遇

- 擴大新一代電池化學技術和固態電池組件的應用

- 電動車和電池國產化政策推動國內製造業成長。

- 對先進電池管理系統和電力電子產品的需求激增

- 二次利用和回收電池組件應用領域的成長

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國:NHTSA自動駕駛系統引導與自動駕駛車輛測試舉措

- 歐洲

- 歐盟電池法規(歐盟法規 2023/1542)

- 德國:電池法(Batteriegesetz-BattG)

- 英國:電池和蓄電池法規

- 法國:電池生產者延伸責任制(EPR)

- 亞太地區

- 中國:新能源汽車動力電池安全與回收管理條例

- 日本:經濟產業省鋰離子電池安全與回收指南

- 韓國:《電氣電子設備與車輛資源化回收法》

- 新加坡:環境保護與管理(電池廢棄物)條例

- 拉丁美洲

- 巴西:國家固態廢棄物政策(電力逆向物流法規)

- 墨西哥:官方標準 NOM-212-SEMARNAT(電池廢棄物管理)

- 智利:生產者延伸責任法(第20920號法律)

- 中東和非洲

- 阿拉伯聯合大公國:聯邦綜合廢棄物管理法(電池相關條款)

- 沙烏地阿拉伯:環境法和SASO電動車電池技術法規

- 南非:《國家環境管理法》-《廢棄物法》(電池合規性)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利分析

- 永續性和環境影響分析

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來前景與機遇

- OEM實施框架

- 垂直整合趨勢

- 長期供應合約及其對零件價格的影響

- 優選供應商模式和公開採購

- 共同開發和合資模式

- 使用案例和應用場景

- 全球產能與運轉率分析

- 運作能與公佈產能對比

- 各區域的運轉率

- 面臨產能過剩及供不應求風險的地區

- 識別組件中的瓶頸

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 依電池類型分類的市場估計與預測,2022-2035年

- 圓柱形

- 袋式

- 棱鏡電池

6. 2022-2035年按推進方式分類的市場估計與預測

- 電池式電動車(BEV)

- PHEV

- HEV

第7章 依車輛類型分類的市場估計與預測,2022-2035年

- 搭乘用車

- 轎車

- 掀背車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- MCV

- 重型商用車(HCV)

- 二輪車和三輪車

8. 2022-2035年按電池化學類型分類的市場估算與預測

- 磷酸鋰鐵

- 鎳鈷鋁合金

- 鎳、錳、鈷

- 錳酸鋰

- 其他

第9章 按組件分類的市場估算與預測,2022-2035年

- 細胞成分

- 陰極

- 陽極

- 電解質

- 其他

- 包裝零件

- 電池管理系統

- 溫度控管系統

- 外殼和圍護結構

- 其他

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 菲律賓

- 印尼

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- BASF SE

- BYD

- Contemporary Amperex Technology Co. Limited(CATL)

- Johnson

- LG Energy Solution

- Panasonic

- Samsung

- Umicore

- Arkema

- 當地公司

- Asahi Kasei

- BTR New Energy Materials

- Celgard

- EVE Energy

- Ganfeng Lithium

- Gotion High-Tech

- Huayou Cobalt

- JFE Chemical

- Mitsubishi Chemical

- SK Innovation

- Sumitomo Metal Mining

- Toray Industries

- 新興企業

- Amprius Technologies

- Anovion Technologies

- Ascend Elements

- FREYR Battery

- QuantumScape

- Redwood Materials

The Global Electric Vehicle Battery Components Market was valued at USD 117.2 billion in 2025 and is estimated to grow at a CAGR of 16.3% to reach USD 563.7 billion by 2035.

The rapid adoption of electric vehicles worldwide is transforming automotive powertrain design and reshaping supply chains. Components such as battery cells, modules, cathodes, anodes, battery management systems (BMS), and thermal management solutions are now central to determining vehicle range, performance, safety, and cost efficiency. As automakers shift from internal combustion engines to dedicated EV architectures, battery systems are increasingly treated as fully integrated platforms rather than individual parts, influencing both operational viability and lifecycle economics. The market is further boosted by large-scale investments and strategic collaborations among automakers, battery manufacturers, material suppliers, and semiconductor firms. Vertical integration strategies, including in-house battery assembly, localized cell production, and joint ventures for cathode and anode materials, are enabling OEMs to secure supplies, lower costs, and improve quality. Additionally, extensive component testing, lifecycle optimization, and adherence to global safety standards are enhancing product reliability, durability, and thermal safety.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $117.2 Billion |

| Forecast Value | $563.7 Billion |

| CAGR | 16.3% |

The battery electric vehicle (BEV) segment held 49% share in 2025 and is expected to grow at a CAGR of 17% through 2035. BEVs rely entirely on battery power, driving strong demand for high-capacity cells, modules, and associated systems to ensure long driving ranges, rapid charging, and consistent performance. Global policies and incentives supporting zero-emission vehicles further accelerate BEV adoption, positioning this segment as the primary growth driver for the market.

The cylindrical cells segment held 64% share in 2025, with projected growth at a CAGR of 15.7% from 2026 to 2035. These cells are favored for their proven performance, high energy density, superior thermal management, and long lifecycle. Their modular design and standardized sizes allow seamless integration into battery packs, simplifying assembly, maintenance, and recycling. Cylindrical cells also provide enhanced safety, reliable heat dissipation, and durability under high current loads, making them a preferred choice for both passenger and commercial EV applications.

China Electric Vehicle (EV) Battery Components Market reached a significant share in 2025. The country's rapid industrialization, strong domestic EV demand, and extensive supply chain integration support robust market expansion. China's dominant EV production base drives ongoing demand for battery cells, cathodes, anodes, separators, electrolytes, and casings. Control over upstream lithium refining, cathode manufacturing, and graphite anode production ensures cost efficiency, rapid scaling, and stable supply. Policy support through production-linked incentives and long-term industrial planning further accelerates technology adoption and capacity expansion across battery component segments.

Key players shaping the Global Electric Vehicle Battery Components Market include CATL, BYD, Panasonic, Blue Line Battery, Johnson Matthey, Mitsubishi Chemical, LG Energy Solution, Samsung SDI, Sumitomo Metal Mining, and Umicore. Leading companies in the Electric Vehicle Battery Components Market are adopting multiple strategies to strengthen their market presence and competitive position. These include forming strategic alliances with automakers and material suppliers to secure raw material access, investing in localized manufacturing to reduce costs and improve supply chain resilience, and expanding R&D efforts to develop next-generation high-capacity, fast-charging, and longer-lasting battery systems. Companies are also enhancing production scalability, integrating advanced thermal management and battery management technologies, and pursuing mergers or joint ventures to enter new geographic markets. Focused testing, lifecycle optimization, and adherence to global safety and environmental standards further improve product reliability, building trust among OEMs and fleet operators and solidifying long-term market foothold.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery Form

- 2.2.3 Propulsion

- 2.2.4 Vehicle

- 2.2.5 Battery Chemistry

- 2.2.6 Component

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global adoption of electric passenger and commercial vehicles

- 3.2.1.2 Increase in government incentives, subsidies, and EV infrastructure investments

- 3.2.1.3 Expansion of battery giga factories and localized manufacturing capacity

- 3.2.1.4 Growing electrification of logistics, public transport, and fleet vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and price volatility of critical battery raw materials

- 3.2.2.2 Limited large-scale battery recycling and end-of-life infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in adoption of next-generation battery chemistries and solid-state components

- 3.2.3.2 Increase in domestic manufacturing supported by EV and battery localization policies

- 3.2.3.3 Surge in demand for advanced battery management systems and power electronics

- 3.2.3.4 Growth in second life and recycling-based battery component applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States: NHTSA ADS Guidance & AV TEST Initiative.

- 3.4.2 Europe

- 3.4.2.1 EU Battery Regulation (Regulation (EU) 2023/1542)

- 3.4.2.2 Germany: Battery Act (Batteriegesetz - BattG)

- 3.4.2.3 United Kingdom: Batteries and Accumulators Regulations

- 3.4.2.4 France: Extended Producer Responsibility (EPR) for Batteries

- 3.4.3 Asia Pacific

- 3.4.3.1 China: New Energy Vehicle Power Battery Safety & Recycling Regulations

- 3.4.3.2 Japan: METI Lithium-Ion Battery Safety & Recycling Guidelines

- 3.4.3.3 South Korea: Act on Resource Circulation of Electrical & Electronic Equipment and Vehicles

- 3.4.3.4 Singapore: Environmental Protection and Management (Battery Waste) Regulations

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Solid Waste Policy (Battery Reverse Logistics Rules)

- 3.4.4.2 Mexico: Official Standard NOM-212-SEMARNAT (Battery Waste Management)

- 3.4.4.3 Chile: Extended Producer Responsibility Law (Law No. 20,920)

- 3.4.5 MEA

- 3.4.5.1 United Arab Emirates: Federal Integrated Waste Management Law (Battery Provisions)

- 3.4.5.2 Saudi Arabia: Environmental Law & SASO EV Battery Technical Regulations

- 3.4.5.3 South Africa: National Environmental Management - Waste Act (Battery Compliance)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental impact analysis

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Future outlook & opportunities

- 3.11 OEM implementation framework

- 3.11.1 Vertical integration trends

- 3.11.2 Long-term offtake agreements & their impact on component pricing

- 3.11.3 Preferred supplier models vs open procurement

- 3.11.4 Co-development & joint venture models

- 3.12 Use Cases & application scenarios

- 3.13 Global capacity & utilization analysis

- 3.13.1 Installed vs announced component capacity

- 3.13.2 Regional utilization rates

- 3.13.3 Overcapacity & under-supply risk zones

- 3.13.4 Component bottleneck identification

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Battery Form, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Cylindrical

- 5.3 Pouch

- 5.4 Prismatic

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Sedan

- 7.2.2 Hatchback

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Two- & Three-Wheelers

Chapter 8 Market Estimates & Forecast, By Battery Chemistry, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lithium iron phosphate

- 8.3 Nickel cobalt aluminum

- 8.4 Nickel manganese cobalt

- 8.5 Lithium manganese oxide

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Cell Components

- 9.2.1 Cathode

- 9.2.2 Anode

- 9.2.3 Electrolyte

- 9.2.4 Others

- 9.3 Pack Components

- 9.3.1 Battery Management System

- 9.3.2 Thermal Management System

- 9.3.3 Housing & Enclosure

- 9.3.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Belgium

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.4.8 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BASF SE

- 11.1.2 BYD

- 11.1.3 Contemporary Amperex Technology Co. Limited (CATL)

- 11.1.4 Johnson

- 11.1.5 LG Energy Solution

- 11.1.6 Panasonic

- 11.1.7 Samsung

- 11.1.8 Umicore

- 11.1.9 Arkema

- 11.2 Regional Players

- 11.2.1 Asahi Kasei

- 11.2.2 BTR New Energy Materials

- 11.2.3 Celgard

- 11.2.4 EVE Energy

- 11.2.5 Ganfeng Lithium

- 11.2.6 Gotion High-Tech

- 11.2.7 Huayou Cobalt

- 11.2.8 JFE Chemical

- 11.2.9 Mitsubishi Chemical

- 11.2.10 SK Innovation

- 11.2.11 Sumitomo Metal Mining

- 11.2.12 Toray Industries

- 11.3 Emerging Players

- 11.3.1 Amprius Technologies

- 11.3.2 Anovion Technologies

- 11.3.3 Ascend Elements

- 11.3.4 FREYR Battery

- 11.3.5 QuantumScape

- 11.3.6 Redwood Materials

汽車金屬化薄膜電容器市場報告:趨勢、預測與競爭分析(至2035年)

汽車金屬化薄膜電容器市場報告:趨勢、預測與競爭分析(至2035年) 2026年全球電動車(EV)包裝運輸箱市場監測報告

2026年全球電動車(EV)包裝運輸箱市場監測報告 新能源診斷設備市場:按類型、技術、應用、最終用戶和分銷管道分類,全球預測,2026-2032年

新能源診斷設備市場:按類型、技術、應用、最終用戶和分銷管道分類,全球預測,2026-2032年 電動車保險桿市場規模、佔有率和成長分析:按材質、車輛類型、製造流程分析、通路和地區分類-2026-2033年產業預測

電動車保險桿市場規模、佔有率和成長分析:按材質、車輛類型、製造流程分析、通路和地區分類-2026-2033年產業預測 2026-2034年全球電動車工程塑膠市場規模、佔有率、趨勢及成長分析

2026-2034年全球電動車工程塑膠市場規模、佔有率、趨勢及成長分析 全球自我調整交通底盤市場預測(至2034年):按底盤類型、材料、車輛類型、技術、最終用戶和地區分類

全球自我調整交通底盤市場預測(至2034年):按底盤類型、材料、車輛類型、技術、最終用戶和地區分類 日本電動汽車零件市場規模、佔有率、趨勢及預測(按零件、分銷管道和地區分類),2026-2034年日本電動車電池組件市場:規模、佔有率、趨勢和預測:按組件類型、電池類型、車輛類型、推進系統、最終用戶和地區分類(2026-2034 年)

日本電動汽車零件市場規模、佔有率、趨勢及預測(按零件、分銷管道和地區分類),2026-2034年日本電動車電池組件市場:規模、佔有率、趨勢和預測:按組件類型、電池類型、車輛類型、推進系統、最終用戶和地區分類(2026-2034 年) 電動車零件市場-全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力類型、零件類型、地區和競爭格局分類,2021-2031年)新能源汽車保險絲市場按安裝類型、電壓等級、車輛類型、應用、額定電流、保險絲類型和分銷管道分類,全球預測(2026-2032年)

電動車零件市場-全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力類型、零件類型、地區和競爭格局分類,2021-2031年)新能源汽車保險絲市場按安裝類型、電壓等級、車輛類型、應用、額定電流、保險絲類型和分銷管道分類,全球預測(2026-2032年)