|

市場調查報告書

商品編碼

1936506

垂直農業自動化系統市場機會、成長要素、產業趨勢分析及2026年至2035年預測Vertical Farming Automation System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

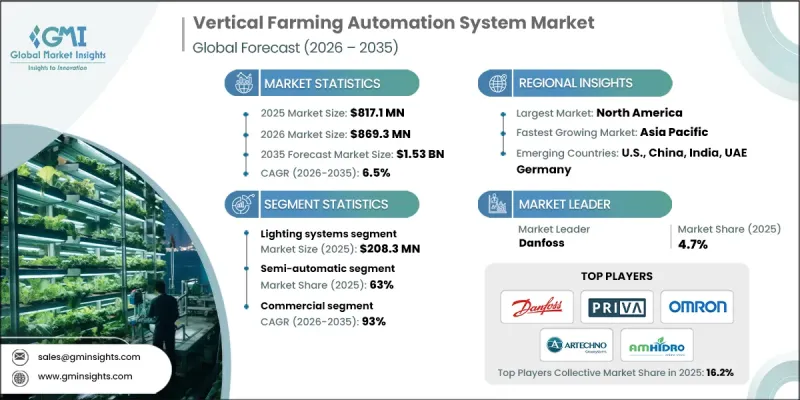

全球垂直農業自動化系統市場預計到 2025 年將達到 8.171 億美元,到 2035 年將達到 15.3 億美元,年複合成長率為 6.5%。

在有限的空間內,最大限度地提高作物產量並最大限度地減少資源消耗的需求是推動垂直農業成長的動力。垂直農業依靠堆疊式種植系統,能夠在實現高產量的同時減少用水量和對化學肥料的依賴。自動化技術在提高這些可控環境中的生產力、穩定性和營運效率方面發揮核心作用。政府支持和財政獎勵促進了永續農業實踐,也推動了市場擴張。人們對提高用水效率和減少土地利用等環境效益的認知不斷提高,正在推動垂直農業在各個地區的普及。先進的照明技術在垂直農業中仍然至關重要,因為它利用人工光源來模擬各種作物的最佳生長條件。現代LED解決方案能夠精確控制光照強度和頻譜,同時最大限度地減少發熱量,縮短與作物的安裝距離,並提高空間利用率。動態照明系統加速作物生長週期,提高產量質量,並在整個種植階段最佳化營養供給。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 8.171億美元 |

| 預測金額 | 15.3億美元 |

| 複合年成長率 | 6.5% |

預計到2025年,照明系統市場規模將達到2.083億美元,2026年至2035年的複合年成長率(CAGR)為6.7%。垂直農業對精準環境控制的需求是推動市場成長的主要因素。氣候控制解決方案能夠調節溫度、濕度和二氧化碳水平,確保作物均勻生長。智慧氣候控制技術的進步提高了系統效率,同時降低了營運成本。照明仍然是影響植物生長、產量和品質的關鍵因素。節能型LED技術因其對不同作物類型和生長階段的適應性而持續受到歡迎。

預計2026年至2035年間,商業領域將以93%的複合年成長率成長。商業營運越來越依賴自動化來支援大規模食品生產、降低勞動強度並維持作物品質的穩定性。機器人、人工智慧和互聯系統等技術有助於最佳化產量和提高營運可靠性。

到2025年,美國垂直農業自動化系統市場規模預計將達到3.201億美元,佔77%的市場。市場成長的主要驅動力是都市化加快、對永續食品體系的需求以及提高農業效率的必要性。城市農業解決方案的日益普及使得食品生產更貼近消費地,從而降低了物流複雜性,並提高了食品供應的新鮮度。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依系統類型

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依系統類型分類的市場估算與預測,2022-2035年

- 空調系統

- 暖通空調系統

- 除濕機

- 加濕系統

- 通風系統

- 其他(二氧化碳注入/濃縮系統等)

- 照明系統

- LED栽培照明系統

- 螢光照明系統

- 其他(照明和配電設備等)

- 灌溉和施肥系統

- 滴灌系統

- 自動加藥裝置

- 水過濾和處理系統

- 其他(營養液培養系統等)

- 感測器和監控硬體

- 環境感測器

- 光測量感測器

- 氣體感測器

- 其他(水質感測器等)

- 其他(機器人自動化系統等)

第6章 依技術類型分類的市場估算與預測,2022-2035年

- 水耕法

- 氣耕

- 水耕法

7. 依自動化程度分類的市場估算與預測,2022-2035 年

- 半自動

- 全自動

第8章 依作物類型分類的市場估算與預測,2022-2035年

- 綠葉蔬菜和香草

- 水果和蔬菜

- 花卉和觀賞植物

- 其他(藥用植物等)

第9章 依最終用戶分類的市場估算與預測,2022-2035年

- 供個人/住宅使用

- 商業的

- 零售和酒店業

- 餐廳

- 雜貨店

- 其他(研究機構、教育機構等)

第10章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接銷售

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- American Hydroponics

- Arianetech

- Artechno Growsystems

- AutoStore

- Danfoss

- Green Automation

- Heliospectra

- Jungheinrich

- Logiqs

- Modula USA

- OMRON Corporation

- Priva

- Signify Holding

- Swisslog

- TTA

The Global Vertical Farming Automation System Market was valued at USD 817.1 million in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 1.53 billion by 2035.

Growth is driven by the need to maximize crop output in constrained spaces while reducing resource consumption. Vertical farming relies on stacked cultivation systems that allow higher yields with lower water usage and reduced dependency on chemical inputs. Automation plays a central role in improving productivity, consistency, and operational efficiency across these controlled environments. Supportive government initiatives and financial incentives that encourage sustainable farming practices further contribute to market expansion. Awareness of environmental benefits, such as water efficiency and reduced land use, strengthens adoption across regions. Advanced lighting technologies remain essential to vertical farming, as artificial illumination replicates optimal growth conditions for different crops. Modern LED solutions enable precise control of light intensity and spectrum while minimizing heat output, allowing closer placement to crops and improved space utilization. Dynamic lighting systems enhance growth cycles, improve yield quality, and support nutrient optimization throughout cultivation stages.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $817.1 Million |

| Forecast Value | $1.53 Billion |

| CAGR | 6.5% |

The lighting systems segment generated USD 208.3 million in 2025 and is expected to grow at a CAGR of 6.7% during 2026-2035. Demand rises alongside the need for accurate environmental management within vertical farms. Climate control solutions regulate temperature, humidity, and carbon dioxide levels to ensure uniform crop development. Advancements in intelligent climate management improve system efficiency while lowering operating costs. Lighting remains a critical component because it directly influences plant development, productivity, and quality. Energy-efficient LED technologies continue gaining preference due to their adaptability across crop types and growth phases.

The commercial segment is projected to grow at a CAGR of 93% from 2026 to 2035. Commercial operations increasingly depend on automation to support large-scale food production, reduce labor intensity, and maintain consistent crop quality. Technologies such as robotics, artificial intelligence, and connected systems support yield optimization and operational reliability.

United States Vertical Farming Automation System Market held 77% share, generating USD 320.1 million in 2025. Growth is supported by rising urbanization, demand for sustainable food systems, and the need to enhance agricultural efficiency. Increased adoption of urban farming solutions brings food production closer to consumption centers, reducing logistical complexity and improving supply freshness.

Key companies operating in the Global Vertical Farming Automation System Market include Signify Holding, Danfoss, OMRON Corporation, Heliospectra, Swisslog, American Hydroponics, Priva, AutoStore, Jungheinrich, Artechno Growsystems, Green Automation, Modula USA, Logiqs, Arianetech, and TTA. Companies in the vertical farming automation system market strengthen their market position by investing in advanced automation technologies that improve precision, scalability, and energy efficiency. Many focus on integrating AI-driven monitoring systems to optimize growing conditions and reduce operational costs. Strategic partnerships with agricultural operators help accelerate system adoption and customization. Manufacturers emphasize modular system designs to support flexible deployment and future expansion. Continuous innovation in lighting, climate control, and data analytics enhances performance differentiation. Expanding global distribution networks and offering long-term technical support further reinforce customer confidence.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System Type

- 2.2.3 Technology Type

- 2.2.4 Automation Level

- 2.2.5 Crop Type

- 2.2.6 End Users

- 2.2.7 Distribution Channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By system type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By System Type, 2022 - 2035 ($Million, Thousand Units)

- 5.1 Key trends

- 5.2 Climate control systems

- 5.2.1 HVAC systems

- 5.2.2 Dehumidifiers

- 5.2.3 Humidification systems

- 5.2.4 Ventilation systems

- 5.2.5 Others (Co2 injection/enrichment systems etc.)

- 5.3 Lighting systems

- 5.3.1 LED grow light systems

- 5.3.2 Fluorescent light systems

- 5.3.3 Others (light distribution hardware etc.)

- 5.4 Irrigation & fertigation systems

- 5.4.1 Drip irrigation systems

- 5.4.2 Automated dosing equipment

- 5.4.3 Water filtration & treatment systems

- 5.4.4 Others (nutrient film technique systems etc.)

- 5.5 Sensor & monitoring hardware

- 5.5.1 Environmental sensors

- 5.5.2 Light measurement sensors

- 5.5.3 Gas sensors

- 5.5.4 Others (water quality sensors etc.)

- 5.6 Others (robotic automation systems etc.)

Chapter 6 Market Estimates & Forecast, By Technology Type, 2022 - 2035 ($Million, Thousand Units)

- 6.1 Key trends

- 6.2 Hydroponics

- 6.3 Aeroponics

- 6.4 Aquaponics

Chapter 7 Market Estimates & Forecast, By Automation Level, 2022 - 2035 ($Million, Thousand Units)

- 7.1 Key trends

- 7.2 Semi-automatic

- 7.3 Fully automatic

Chapter 8 Market Estimates & Forecast, By Crop Type, 2022 - 2035 ($Million, Thousand Units)

- 8.1 Key trends

- 8.2 Leafy greens & herbs

- 8.3 Fruiting vegetables

- 8.4 Flowers & ornamentals

- 8.5 Others (medicinal plants etc.)

Chapter 9 Market Estimates & Forecast, By End Users, 2022 - 2035 ($Million, Thousand Units)

- 9.1 Key trends

- 9.2 Individual/residential

- 9.3 Commercial

- 9.3.1 Retail & Hospitality

- 9.3.2 Restaurants

- 9.3.3 Grocery stores

- 9.3.4 Others (research & educational institutions etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Million, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Million, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 American Hydroponics

- 12.2 Arianetech

- 12.3 Artechno Growsystems

- 12.4 AutoStore

- 12.5 Danfoss

- 12.6 Green Automation

- 12.7 Heliospectra

- 12.8 Jungheinrich

- 12.9 Logiqs

- 12.10 Modula USA

- 12.11 OMRON Corporation

- 12.12 Priva

- 12.13 Signify Holding

- 12.14 Swisslog

- 12.15 TTA