|

市場調查報告書

商品編碼

1936491

工業排放監測與控制系統市場:機會、成長要素、產業趨勢分析及2026年至2035年預測Industrial Emission Monitoring and Control System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

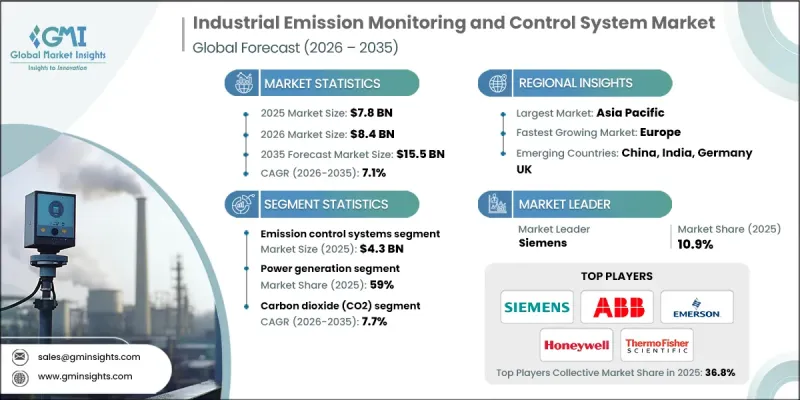

全球工業排放監測和控制系統市場預計到 2025 年將達到 78 億美元,到 2035 年將達到 155 億美元,年複合成長率為 7.1%。

由於旨在限制工業排放和減少環境污染的日益嚴格的環境法規,市場正在不斷擴張。該地區各國政府正在強制執行合規要求,鼓勵各行業採用先進的排放監控和控制技術。因此,製造商正在投資能夠提供準確、即時排放數據的先進系統。包括人工智慧 (AI) 和互聯監測平台在內的技術進步正在提高系統效能並促進其應用。能源和電力產業仍然是工業排放的主要來源,也是監控和控制解決方案需求的重要驅動力。向清潔能源發電的持續轉型以及發電設施中排放技術的應用,正在創造強勁的成長機會。儘管市場面臨高資本投資和升級舊有系統相關的技術複雜性等挑戰,但政府的激勵措施和財政支持計劃正在抵消這些障礙,並促進更廣泛的應用。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 78億美元 |

| 預測金額 | 155億美元 |

| 複合年成長率 | 7.1% |

預計2026年至2035年間,排放監測系統市場將以7.3%的複合年成長率成長。互聯感測器和先進數據分析技術的整合,實現了連續監測、即時報告和更高的合規準確性。工業界日益重視減少溫室氣體排放和空氣污染物,直接推動了對監測和控制解決方案的需求。監管機構正在加強環境框架並推廣更清潔的生產方式,進一步加速了現代排放控制技術在工業設施中的應用。

預計2026年至2035年間,二氧化碳排放市場將以7.7%的複合年成長率成長。人們對氣候變遷和全球暖化日益成長的關注,促使人們更加重視二氧化碳排放的測量和管理。世界各國政府正在實施碳定價機制和排放責任政策,強制要求各產業更嚴格追蹤和管理其二氧化碳排放。這種監管壓力使得二氧化碳監測成為工業排放管理策略的關鍵組成部分。

預計2025年,美國工業排放監控與控制系統市場規模將達到18億美元,佔77%的市佔率。美國市場的成長得益於聯邦政府制定的嚴格環境法規和執法架構。法律要求工業設施持續監測、報告並減少排放。此外,企業永續性舉措和日益增強的環境責任意識也正在加速各行業對排放監控解決方案的投資。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依系統類型

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依系統類型分類的市場估算與預測,2022-2035年

- 排放監測系統

- 連續排放監測系統(CEMS)

- 預測性排放監測系統(PEMS)

- 排放氣體控制系統

- 靜電除塵設備(ESP)

- 洗滌器(排煙脫硫設備)

- 催化劑體系

- 袋濾式集塵器/袋式除塵器

- 吸附劑注入系統

- 其他(熱氧化設備、旋風分離器等)

6. 按污染物類型分類的市場估計與預測,2022-2035 年

- 氮氧化物(NOx)

- 硫氧化物(SOx/SO2)

- 二氧化碳(CO2)

- 甲烷

- 顆粒物

- 其他成分(THC、汞等)

7. 2022-2035年按最終用途產業分類的市場估算與預測

- 發電

- 石油和天然氣

- 化工/石油化工

- 金屬和採礦

- 紙漿和造紙

- 製藥

- 其他(船等)

第8章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接銷售

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- ABB

- AMETEK

- Durag Group

- Emerson Electric

- Endress+Hauser

- Forbes Marshall

- Honeywell International

- Horiba

- Kawasaki Heavy Industries

- Kongsberg

- Mitsubishi Heavy Industries

- Siemens

- Teledyne Technologies

- Thermo Fisher Scientific

- Yokogawa Electric

The Global Industrial Emission Monitoring and Control System Market was valued at USD 7.8 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 15.5 billion by 2035.

Market expansion is driven by increasingly strict environmental regulations aimed at limiting industrial emissions and reducing environmental pollution. Governments across regions are enforcing compliance requirements that encourage industries to adopt advanced emission monitoring and control technologies. As a result, manufacturers are investing in sophisticated systems capable of delivering accurate, real-time emission data. Technological advancements, including the integration of artificial intelligence and connected monitoring platforms, are enhancing system performance and driving adoption. The energy and power sector remains one of the largest contributors to industrial emissions, making it a key demand generator for monitoring and control solutions. Ongoing transitions toward cleaner energy generation and the implementation of emission reduction technologies in power facilities are creating strong growth opportunities. While the market faces challenges such as high capital investment requirements and technical complexity in upgrading legacy systems, supportive government incentives and financial assistance programs are helping offset these barriers and encouraging broader adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.8 Billion |

| Forecast Value | $15.5 Billion |

| CAGR | 7.1% |

The emission monitoring systems segment will grow at a CAGR of 7.3% during 2026 to 2035. The incorporation of connected sensors and advanced data analytics is improving continuous monitoring, real-time reporting, and compliance accuracy. Industries are placing greater emphasis on reducing greenhouse gas emissions and airborne pollutants, which is directly increasing demand for monitoring and control solutions. Regulatory authorities are strengthening environmental frameworks and promoting cleaner production practices, further accelerating the deployment of modern emission control technologies across industrial facilities.

The carbon dioxide segment is projected to grow at a CAGR of 7.7% from 2026 to 2035. Heightened awareness around climate change and global temperature rise has intensified the focus on carbon dioxide emission measurement and management. Governments worldwide are implementing carbon pricing mechanisms and emission accountability policies, compelling industries to track and control CO2 output more rigorously. This regulatory pressure is making CO2 monitoring a critical component of industrial emission management strategies.

United States Industrial Emission Monitoring and Control System Market accounted for 77% share and generated USD 1.8 billion in 2025. Market growth in the country is supported by stringent environmental regulations and enforcement frameworks established by federal authorities. Legislative mandates require industrial facilities to measure, report, and reduce emissions consistently. Additionally, rising corporate focus on sustainability initiatives and environmental responsibility is accelerating investment in emission monitoring solutions across multiple industries.

Key companies operating in the Global Industrial Emission Monitoring and Control System Market include Siemens, ABB, Emerson Electric, Honeywell International, Yokogawa Electric, Thermo Fisher Scientific, Endress+Hauser, Mitsubishi Heavy Industries, Horiba, Teledyne Technologies, AMETEK, Kongsberg, Kawasaki Heavy Industries, Durag Group, and Forbes Marshall. Companies in the Industrial Emission Monitoring and Control System Market are strengthening their market position through technology innovation, strategic partnerships, and geographic expansion. Leading players are investing heavily in research and development to enhance system accuracy, automation, and digital integration. Many are expanding their product portfolios to offer customized solutions tailored to specific industrial applications.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System Type

- 2.2.3 Pollutant Type

- 2.2.4 End Use Industry

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By system type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By System Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Emission monitoring systems

- 5.2.1 Continuous emission monitoring system (CEMS)

- 5.2.2 Predictive emission monitoring system (PEMS)

- 5.3 Emission control systems

- 5.3.1 Electrostatic precipitators (ESP)

- 5.3.2 Scrubbers (FGD systems)

- 5.3.3 Catalytic systems

- 5.3.4 Fabric filters/baghouses

- 5.3.5 Sorbent injection systems

- 5.3.6 Others (thermal oxidizers, cyclones etc.)

Chapter 6 Market Estimates & Forecast, By Pollutant Type, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Nitrogen Oxides (NOx)

- 6.3 Sulfur Oxides (SOx/SO2)

- 6.4 Carbon Dioxide (CO2)

- 6.5 Methane

- 6.6 Particulate Matter

- 6.7 Others (THC, mercury etc.)

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Power Generation

- 7.3 Oil & Gas

- 7.4 Chemical & Petrochemical

- 7.5 Metals & Mining

- 7.6 Pulp & Paper

- 7.7 Pharmaceuticals

- 7.8 Others (marine etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 AMETEK

- 10.3 Durag Group

- 10.4 Emerson Electric

- 10.5 Endress+Hauser

- 10.6 Forbes Marshall

- 10.7 Honeywell International

- 10.8 Horiba

- 10.9 Kawasaki Heavy Industries

- 10.10 Kongsberg

- 10.11 Mitsubishi Heavy Industries

- 10.12 Siemens

- 10.13 Teledyne Technologies

- 10.14 Thermo Fisher Scientific

- 10.15 Yokogawa Electric

全球連續排放氣體監測系統(CEMS)市場報告:2021-2032年歷史表現及預測

全球連續排放氣體監測系統(CEMS)市場報告:2021-2032年歷史表現及預測 排放氣體監測系統市場:按類型、組件、部署方式和最終用戶分類-2026-2032年全球市場預測

排放氣體監測系統市場:按類型、組件、部署方式和最終用戶分類-2026-2032年全球市場預測 2026年全球連續排放監測系統市場報告

2026年全球連續排放監測系統市場報告 排放氣體監測系統市場:按類型、應用、組件、技術、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2026-2033 年)

排放氣體監測系統市場:按類型、應用、組件、技術、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2026-2033 年) 2026-2030年全球海事排放監測系統市場

2026-2030年全球海事排放監測系統市場 排放監測系統 (EMS) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和安裝類型分類連續排放監測系統市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類2026年全球排放監測系統市場報告

排放監測系統 (EMS) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和安裝類型分類連續排放監測系統市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類2026年全球排放監測系統市場報告 連續排放監測系統市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034年)

連續排放監測系統市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034年) 排放監測系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(依排放類型、監測技術、終端用戶產業、地區及競爭格局分類,2021-2031年)

排放監測系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(依排放類型、監測技術、終端用戶產業、地區及競爭格局分類,2021-2031年)