|

市場調查報告書

商品編碼

1929002

鹼性電池市場機會、成長要素、產業趨勢分析及2026年至2035年預測Alkaline Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

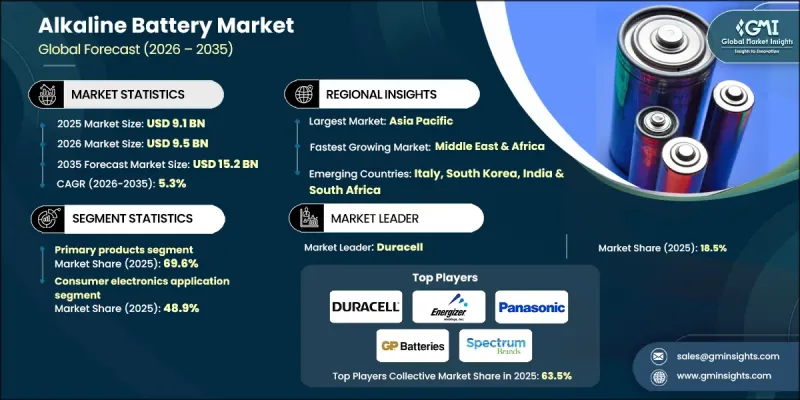

全球鹼性電池市場預計到 2025 年將達到 91 億美元,到 2035 年將達到 152 億美元,年複合成長率為 5.3%。

市場擴張的驅動力在於消費者對無需特殊處理、充電基礎設施或定期維護的低成本電池日益成長的需求。鹼性電池因其可靠性、能源效率和低洩漏風險,被廣泛認可為主要電源,其採用鹼性電解液系統,可提供穩定的電化學性能和較長的保存期限。鹼性電池的可靠性、能源效率和低洩漏風險使其在住宅和商業環境中廣泛應用。人們對攜帶式、高耗能電子設備的依賴性日益增強,推動了對能夠在長時間使用循環中提供穩定電力的電池的需求。隨著日常生活數位化,消費者越來越重視電池的耐用性、易用性和可靠性。不斷增強的環保意識也在影響產品開發,製造商正投資研發無汞鹼性電池,以滿足永續性預期和監管標準。旨在提高能量密度和安全性的持續技術創新正在增強長期需求,並支撐市場穩步成長。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 91億美元 |

| 預測金額 | 152億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,一次鹼性電池市佔率將達到69.6%,並在2035年之前以5.1%的複合年成長率成長。一次性電池無需額外設備即可立即使用,因其便利性和可靠性,市場需求不斷成長。終端用戶在需要快速更換和不間斷運行的應用場景中,尤其是在家庭和職場環境中,更傾向於選擇此類產品。

預計到2025年,家用電子電器應用領域將佔據48.9%的市場佔有率,並在2026年至2035年間以4.8%的複合年成長率成長。該領域的成長主要得益於現代電子產品對高能量密度、小巧便攜電源的需求。由於鹼性電池具有穩定的功率輸出和可靠的使用壽命,製造商和消費者仍然青睞此類電池。

預計到2025年,美國鹼性電池市佔率將達到95.9%,到2035年將成長至32億美元。消費者對價格實惠且可靠的電源解決方案的強勁需求持續推動著鹼性電池在美國的普及。較長的保存期限和穩定的性能也使其在美國不斷成長的電子產品市場中得以繼續使用。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系統

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 成長潛力分析

- 成本結構分析

- 波特分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL 分析

- 新的機會與趨勢

- 數位化和物聯網整合

- 拓展新興市場

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 戰略儀錶板

- 策略舉措

- 企業標竿管理

- 創新與科技趨勢

第5章 2022-2035年依產品分類的市場規模及預測

- 基本的

- 次要

第6章 依應用領域分類的市場規模及預測(2022-2035年)

- 家用電子電器

- 玩具

- 其他

第7章 2022-2035年各地區市場規模及預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第8章 公司簡介

- Camelion Batterien

- Duracell

- Energizer Holding

- FDK Corporation

- Geti.eu

- GPB International Limited

- ISKRA

- Kodak

- Maxell Holdings

- Nanfu

- Panasonic Corporation

- Sanyo

- Sony

- Spectrum Brands Holdings

- Tenergy

- Toshiba International

- Urban Electric Power

- VARTA Consumer Batteries

- Voniko Batteries

- Zhejiang Mustang Battery

The Global Alkaline Battery Market was valued at USD 9.1 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 15.2 billion by 2035.

Market expansion is supported by rising demand for cost-efficient batteries that do not require special handling, charging infrastructure, or routine maintenance. Alkaline batteries are widely recognized as primary power sources that operate through an alkaline electrolyte system, enabling stable electrochemical performance and extended shelf life. Their reputation for reliability, energy efficiency, and reduced leakage risk continues to support adoption across residential and commercial environments. Growing reliance on portable and energy-intensive electronic equipment is increasing the need for batteries capable of delivering consistent output over longer usage cycles. Consumers increasingly prioritize durability, ease of use, and dependable performance as daily routines become more digitally oriented. Environmental awareness is also shaping product development, with manufacturers investing in mercury-free alkaline batteries to meet sustainability expectations and regulatory standards. Continuous innovation aimed at improving energy density and safety is reinforcing long-term demand and supporting steady market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.1 Billion |

| Forecast Value | $15.2 Billion |

| CAGR | 5.3% |

The primary alkaline batteries segment accounted for 69.6% share in 2025 and is projected to grow at a CAGR of 5.1% through 2035. Demand for single-use batteries that are immediately functional without additional equipment is increasing due to their simplicity and reliability. End users favor these products for applications where quick replacement and uninterrupted performance are essential, particularly in household and workplace settings.

The consumer electronics application segment held a 48.9% share in 2025 and is anticipated to grow at a CAGR of 4.8% from 2026 to 2035. Growth in this segment is driven by the need for compact power sources with high energy density that can support consistent operation of modern electronic products. Manufacturers and consumers alike continue to favor alkaline batteries for their stable output and dependable lifespan.

United States Alkaline Battery Market held 95.9% share in 2025 and is expected to generate USD 3.2 billion by 2035. Strong demand for affordable and reliable power solutions continues to drive adoption nationwide. Long storage life and consistent performance support ongoing use as the domestic electronics market continues to expand.

Prominent companies operating in the Global Alkaline Battery Market include Duracell, Panasonic Corporation, Energizer Holding, VARTA Consumer Batteries, Toshiba International, Nanfu, Maxell Holdings, Spectrum Brands Holdings, Sony, Camelion Batterien, Kodak, GPB International Limited, FDK Corporation, Tenergy, Zhejiang Mustang Battery, Geti.eu, ISKRA, Sanyo, Urban Electric Power, and Voniko Batteries. Companies in the Alkaline Battery Market are strengthening their market position through product innovation, sustainability initiatives, and global distribution expansion. Many manufacturers are investing in mercury-free and environmentally responsible designs to meet regulatory requirements and align with consumer expectations. Brand differentiation through improved energy efficiency and longer shelf life remains a key focus. Firms are also expanding manufacturing capacity and optimizing supply chains to ensure consistent product availability. Strategic partnerships with retailers and private-label offerings are helping increase market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.2 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Porter';s analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Primary

- 5.3 Secondary

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Toys

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Camelion Batterien

- 8.2 Duracell

- 8.3 Energizer Holding

- 8.4 FDK Corporation

- 8.5 Geti.eu

- 8.6 GPB International Limited

- 8.7 ISKRA

- 8.8 Kodak

- 8.9 Maxell Holdings

- 8.10 Nanfu

- 8.11 Panasonic Corporation

- 8.12 Sanyo

- 8.13 Sony

- 8.14 Spectrum Brands Holdings

- 8.15 Tenergy

- 8.16 Toshiba International

- 8.17 Urban Electric Power

- 8.18 VARTA Consumer Batteries

- 8.19 Voniko Batteries

- 8.20 Zhejiang Mustang Battery

鹼性電池市場:全球市場預測,2026-2032年

鹼性電池市場:全球市場預測,2026-2032年 全球鹼性電池市場規模、佔有率、趨勢和成長分析報告(2026-2034年)鋰碳氟化物紐扣電池市場(按電池尺寸、應用、最終用戶和分銷管道分類)—2026-2032年全球預測全球鹼性電池市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球鹼性電池市場規模、佔有率、趨勢和成長分析報告(2026-2034年)鋰碳氟化物紐扣電池市場(按電池尺寸、應用、最終用戶和分銷管道分類)—2026-2032年全球預測全球鹼性電池市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 鹼性電池市場規模、佔有率和成長分析(按產品、規格、應用和地區分類):產業預測(2026-2033 年)鹼性電池市場-2025年至2030年預測

鹼性電池市場規模、佔有率和成長分析(按產品、規格、應用和地區分類):產業預測(2026-2033 年)鹼性電池市場-2025年至2030年預測 鹼性電池市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型(一次鹼性電池、二次鹼性電池)、按規模、按最終用途行業、按地區和競爭情況細分,2020 年至 2030 年

鹼性電池市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型(一次鹼性電池、二次鹼性電池)、按規模、按最終用途行業、按地區和競爭情況細分,2020 年至 2030 年 鹼性電池全球市場,2025-2029

鹼性電池全球市場,2025-2029 一次性薄膜電池市場機會、成長動力、產業趨勢分析及2025-2034年預測

一次性薄膜電池市場機會、成長動力、產業趨勢分析及2025-2034年預測 鹼性電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

鹼性電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)