|

市場調查報告書

商品編碼

1928994

取放設備市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Pick and Place Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

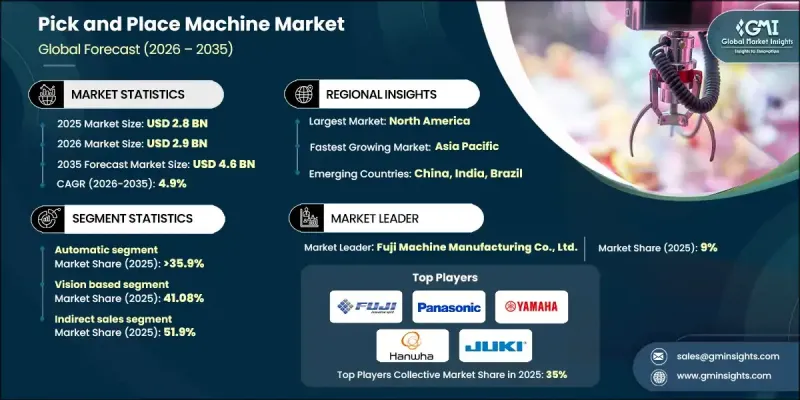

全球取放設備市場預計到 2025 年將達到 28 億美元,到 2035 年將達到 46 億美元,年複合成長率為 4.9%。

市場擴張的驅動力在於對高速、高精度表面黏著技術(SMT) 貼片系統日益成長的需求,而這些系統對於現代電子製造至關重要。對更高效率、精度和穩定品質的不斷提升的需求正在推動行業整合,主要企業透過併購競爭對手來擴展自身能力。這種整合帶來了更豐富的產品系列、更高的研發投入以及更強大的全球市場地位。傳統的手動貼片機和半自動貼片機越來越難以滿足小型化電子產品(尤其是在 5G、汽車和電動車領域)對精度和速度的要求。採用節能伺服馬達和熱穩定性材料的全自動系統可降低運作過程中的功率損耗,並符合永續的高科技製造實務。採用這些先進設備能夠幫助製造商在保持精度和運作效率的同時,實現大批量生產目標。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 28億美元 |

| 預測金額 | 46億美元 |

| 複合年成長率 | 4.9% |

預計到2025年,自動化貼片設備將佔據35.9%的市場佔有率,並創造10億美元的收入。自動化貼片機正逐漸成為主流,因為它們能夠提供現代電子製造所需的亞微米級貼片精度、高速運作和擴充性。這些系統對於工業4.0的普及至關重要,能夠與機器人、智慧工廠網路和預測性維護平台無縫整合。智慧型手機、電動車(EV)以及汽車和航太產業電控系統(ECU)產量的不斷成長,進一步推動了對高性能自動化貼片系統的需求。它們能夠減少人為錯誤、最佳化生產效率並確保產品品質的穩定性,使其成為大規模生產不可或缺的工具。

到2025年,基於視覺的取放系統將佔據41.08%的市場佔有率,市場規模將達到12億美元。視覺系統能夠對小型、高密度零件進行即時光學辨識、對準和缺陷檢測,從而確保極高的產量比率。這項技術對於放置小間距零件和處理複雜組件至關重要,並能達到極高的精確度。檢測和放置的同步整合能夠減少返工和廢棄物,從而提高整體生產效率。在航太、醫療設備組裝和汽車電子等行業,製造商越來越依賴基於視覺的系統來滿足嚴格的品質標準、縮短生產週期並降低錯誤率。

截至2025年,美國貼片設備市場佔據了全球84.5%的市場。這一主導地位得益於先進機器人技術、人工智慧組裝系統和高精度製造技術的早期應用。汽車和航太產業的強勁需求推動了市場成長,在這些產業中,貼片設備對於組裝複雜的電控系統、感測器和高密度基板至關重要。此外,對運作環境和極高精度要求的醫療設備產業也促進了市場成長。在北美,完善的電子製造生態系統、高額的研發投入以及智慧工廠理念的普及,持續推動市場發展。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 電子元件小型化

- 向工業4.0和智慧工廠轉型

- 電動汽車電子設備的需求不斷成長

- 產業潛在風險與挑戰

- 高初始投資

- 高混合小批量生產中的程式設計複雜度

- 機會

- 人工智慧驅動的預測性維護

- 5G和衛星通訊的擴展

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按類型分類的市場估算與預測,2022-2035年

- 手動輸入

- 半自動

- 自動的

第6章 按技術分類的市場估計與預測,2022-2035年

- 基於視覺

- 部隊基地

- 雷射法

- 混合

第7章 依產能分類的市場估計與預測,2022-2035年

- 主要趨勢

- 每小時 10,000 杯或更少

- 10,000~20,000 CPH

- 每小時 20,000 杯或更多

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 家用電子電器

- 車

- 包裝產業

- 製藥

- 後勤

- 其他

9. 2022-2035年按分銷管道分類的市場估算與預測

- 直接地

- 間接

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章 公司簡介

- ASM Assembly Systems GmbH &Co. KG

- Fuji Machine Manufacturing Co., Ltd.

- Juki Corporation

- Panasonic Corporation

- Yamaha Motor Co., Ltd.

- Hanwha Corporation

- Mycronic AB

- Nordson Corporation

- Hanwha Techwin

- ASM Pacific Technology Ltd.

- Universal Instruments Corporation

- Europlacer Group

- Essemtec AG

- Viscom AG

- Speedline Technologies, Inc.

The Global Pick and Place Machine Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 4.6 billion by 2035.

The market's expansion is driven by the increasing demand for high-speed, precise surface-mount technology (SMT) placement systems, which are essential for modern electronics manufacturing. Efficiency gains, accuracy, and the need for consistent quality have encouraged industry consolidation, as leading companies merge or acquire competitors to expand their capabilities. This consolidation has resulted in broader product portfolios, increased R&D investments, and stronger global market presence. Traditional manual component placement or semi-automatic machines are increasingly unable to meet the precision and speed requirements of miniaturized electronics, especially in the 5G, automotive, and EV sectors. Fully automated systems with energy-efficient servo motors and thermally stable materials offer reduced operational power loss and align with sustainable, high-tech manufacturing practices. Adoption of these advanced machines allows manufacturers to meet high-volume production targets while maintaining precision and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 4.9% |

The automatic pick and place segment accounted for 35.9% share in 2025, generating USD 1 billion. Automatic machines dominate because they provide sub-micron placement accuracy, high-speed operation, and scalability required by modern electronics manufacturing. These systems are integral to Industry 4.0 implementations, enabling seamless integration with robotics, smart factory networks, and predictive maintenance platforms. The increasing production of smartphones, EVs, and electronic control units in the automotive and aerospace industries further drives the demand for high-performance automated placement systems. Their ability to reduce human error, optimize throughput, and ensure consistent quality makes them essential for high-volume manufacturing.

Vision-based pick and place systems held 41.08% share, generating USD 1.2 billion in 2025. Vision systems provide real-time optical recognition, alignment, and defect detection for small, high-density components, ensuring extremely high yield rates. This technology is critical for placing fine-pitch components and handling complex assemblies with exceptional accuracy. Its ability to integrate inspection and placement simultaneously reduces rework and waste, improving overall production efficiency. Manufacturers increasingly rely on vision-based systems to achieve faster cycle times, lower error rates, and compliance with stringent quality standards required in aerospace, medical device assembly, and automotive electronics.

U.S. Pick and Place Machine Market held 84.5% share in 2025. This dominance is fueled by early adoption of advanced robotics, AI-integrated assembly systems, and high-precision manufacturing technologies. Strong demand comes from the automotive and aerospace sectors, where pick and place machines are essential for assembling complex electronic control units, sensors, and high-density boards. Additionally, the medical device segment is contributing to growth, requiring specialized machines capable of cleanroom operation and extreme precision. North America's well-established electronics manufacturing ecosystem, combined with high R&D investment and adoption of smart factory concepts, continues to propel the market forward.

Major players operating in the Global Pick and Place Machine Market include ASM Pacific Technology Ltd., Yamaha Motor Co., Ltd., ASM Assembly Systems GmbH & Co. KG, Juki Corporation, Panasonic Corporation, Hanwha Techwin, Mycronic AB, Nordson Corporation, Universal Instruments Corporation, Speedline Technologies, Inc., Europlacer Group, Essemtec AG, Viscom AG, Hanwha Corporation, and others. These companies lead through continuous innovation, global expansion, and the development of automated, vision-integrated systems that meet evolving electronics manufacturing needs. Companies in the Pick and Place Machine Market are adopting multiple strategies to strengthen their market position. They focus heavily on mergers and acquisitions to consolidate technological expertise and expand regional reach. Product innovation, including AI-assisted placement, vision-based defect detection, and energy-efficient servo motors, enhances performance and sustainability. Firms invest in Industry 4.0 solutions to integrate machines into smart factories and provide connected, data-driven platforms for predictive maintenance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Capacity

- 2.2.5 Application

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Miniaturization of electronic components

- 3.2.1.2 Transition to industry 4.0 and smart factories

- 3.2.1.3 Rise in electric vehicle (EV) electronics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital expenditure

- 3.2.2.2 Complexity of programming for high-mix production

- 3.2.3 Opportunities

- 3.2.3.1 Ai-driven predictive maintenance

- 3.2.3.2 Expansion of 5G and satellite communication

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter';s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Semi-automatic

- 5.4 Automatic

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Vision based

- 6.3 Force based

- 6.4 Laser based

- 6.5 Hybrid

Chapter 7 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trend

- 7.2 Upto 10,000 CPH

- 7.3 10,000-20,000 CPH

- 7.4 Above 20,000 CPH

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Automotive

- 8.4 Packaging industry

- 8.5 Pharmaceutical

- 8.6 Logistics

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ASM Assembly Systems GmbH & Co. KG

- 11.2 Fuji Machine Manufacturing Co., Ltd.

- 11.3 Juki Corporation

- 11.4 Panasonic Corporation

- 11.5 Yamaha Motor Co., Ltd.

- 11.6 Hanwha Corporation

- 11.7 Mycronic AB

- 11.8 Nordson Corporation

- 11.9 Hanwha Techwin

- 11.10 ASM Pacific Technology Ltd.

- 11.11 Universal Instruments Corporation

- 11.12 Europlacer Group

- 11.13 Essemtec AG

- 11.14 Viscom AG

- 11.15 Speedline Technologies, Inc.