|

市場調查報告書

商品編碼

1928983

汽車門模組市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Automotive Door Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

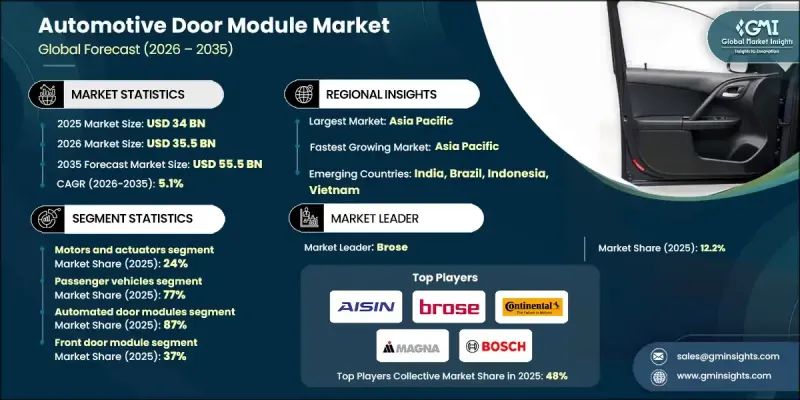

全球汽車門模組市場預計到 2025 年將達到 340 億美元,到 2035 年將達到 555 億美元,年複合成長率為 5.1%。

全球汽車產量穩定成長,以及現代汽車中舒適性、便利性和安全性技術的日益融合,推動了市場擴張。電動出行的加速發展正在重塑車門模組的設計,促使輕量化材料和先進電子系統的應用,從而提升效率並最佳化續航里程。汽車製造商正優先考慮模組化車輛架構,以縮短組裝時間、簡化生產流程並降低整體製造成本。將多個車門相關組件整合到單一模組中,可縮短安裝時間、提高品質一致性,並實現大規模生產的汽車平臺的可擴充性。消費者對更高安全性和易用性的日益成長的期望也進一步推動了市場成長。與門禁控制、乘員保護和自動化功能相關的特性正在各個車型類別中廣泛應用,推動了整車製造商大規模採用整合式車門模組解決方案。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 340億美元 |

| 預測金額 | 555億美元 |

| 複合年成長率 | 5.1% |

預計到 2025 年,馬達和致動器細分市場將佔 24% 的市場佔有率,並預計從 2026 年到 2035 年將以 6.1% 的複合年成長率成長。此細分市場需求的成長是由車輛電氣化程度的提高和自動化功能的日益普及所驅動的,這些都需要緊湊、節能的電子機械組件,這些組件可以無縫整合到車門系統中。

預計到2025年,自動門模組市佔率將達到87%。電子控制門禁和車窗系統在各類車型的普及率不斷提高,推動了該領域的強勁成長。電動車和豪華車的持續成長進一步提升了門模組的電子複雜性,從而支撐了對自動化解決方案的持續需求。

預計到 2025 年,中國汽車門模組市場將佔據 53% 的市場佔有率,達到 85 億美元。中國市場的主導地位得益於其龐大的汽車產量和廣泛的需求,從量產車到高階乘用車(包括電動車車型)。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 提高汽車產量

- 電動車和豪華車市場的成長

- 專注於模組化車輛架構

- 改進的安全性和舒適性功能

- 產業潛在風險與挑戰

- 高系統整合複雜性

- 原始設備製造商面臨成本壓力

- 市場機遇

- 使用輕質材料

- 智慧門禁技術

- 新興汽車市場的擴張

- 成長潛力分析

- 監管環境

- 北美洲

- 美國車輛安全措施

- FMVSS側面碰撞標準

- 加州車輛合規性

- 加拿大車輛指南

- 歐洲

- 歐盟車輛標準

- 歐洲新車安全評鑑協會(Euro NCAP)指南

- 遵守國內法規

- EN門模組標準

- 亞太地區

- 中國汽車法規

- 印度安全標準

- 日本模組指南

- 韓國標準

- 東協區域準則

- 拉丁美洲

- 巴西汽車標準

- 阿根廷合規性

- 墨西哥法規

- 區域安全指南

- 中東和非洲

- 阿拉伯聯合大公國(阿拉伯聯合大公國)車輛標準

- 沙烏地阿拉伯法規

- 南非合規性

- 區域汽車標準

- 北美洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產基地

- 消費基礎

- 進出口

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- OEM廠商採用情形及平台滲透率分析

- 定價、平均售價 (ASP) 和成本趨勢

- 電動車架構對車門模組設計的影響

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 按組件分類的市場估算與預測,2022-2035年

- 門閂和把手

- 車窗穩壓器

- 揚聲器

- 馬達和致動器

- 電氣連接器和線路

- 控制單元

- 密封系統

- 其他

第6章 依車輛類型分類的市場估計與預測,2022-2035年

- 搭乘用車

- 掀背車車

- 轎車

- SUV 與跨界車

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

7. 2022-2035年各模組市場估算與預測

- 手動門模組

- 自動門模組

第8章 2022-2035年按推進方式分類的市場估算與預測

- 內燃機(ICE)

- 電池式電動車(BEV)

- 混合動力汽車

第9章 按門類型分類的市場估算與預測,2022-2035年

- 入口大門模組

- 後門模組

- 滑動門模組

- 升降尾門模組

第10章 依銷售管道分類的市場估計與預測,2022-2035年

- OEM

- 售後市場

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

第12章:公司簡介

- 世界玩家

- Aisin

- Brose

- Continental

- Denso

- Forvia

- Hyundai Mobis

- Magna International

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- 區域玩家

- Flex-N-Gate

- Grupo Antolin

- Hi-Lex

- Inteva Products

- PHA Korea

- 新興企業/顛覆者

- CIE Automotive

- DaikyoNishikawa

- Dura Automotive Systems

- Hirotec

- Kiekert

The Global Automotive Door Module Market was valued at USD 34 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 55.5 billion by 2035.

Market expansion is driven by steady growth in global vehicle production along with the rising integration of comfort, convenience, and safety technologies in modern vehicles. The accelerating shift toward electric mobility is reshaping door module design, encouraging the adoption of lightweight materials and advanced electronic systems to support efficiency and range optimization. Vehicle manufacturers are increasingly prioritizing modular vehicle architectures to reduce assembly time, streamline production workflows, and lower overall manufacturing costs. Integrating multiple door-related components into a single module allows faster installation, improved quality consistency, and scalability across high-volume vehicle platforms. Growing consumer expectations for enhanced safety and ease of use are further supporting market growth. Features related to access control, occupant protection, and automated functionality are becoming widely adopted across vehicle categories, encouraging higher-volume deployment of integrated door module solutions by original equipment manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $34 Billion |

| Forecast Value | $55.5 Billion |

| CAGR | 5.1% |

The motors and actuators segment held a 24% share in 2025 and is projected to grow at a CAGR of 6.1% from 2026 to 2035. Demand growth in this segment is being supported by rising vehicle electrification and increased use of automated functions, which require compact and energy-efficient electromechanical components that can be seamlessly integrated into door systems.

The automated door modules segment accounted for 87% share in 2025. Strong adoption is being driven by the widespread installation of electronically controlled access and window systems across vehicle segments. The continued growth of electric and premium vehicles is further increasing the electronic complexity of door modules, supporting sustained demand for automated solutions.

China Automotive Door Module Market held a 53% share and generated USD 8.5 billion in 2025. The country's dominance is supported by high vehicle production volumes and strong demand across both mass-market and premium passenger vehicles, including electric models.

Key companies operating in the automotive door module market include Magna International, Brose, Hyundai Mobis, Continental, ZF Friedrichshafen, Aisin, Inteva Products, Denso, Robert Bosch, and Hi-Lex. Companies active in the Global Automotive Door Module Market are strengthening their market position through continuous innovation, lightweight design development, and increased electronics integration. Many players are investing in research to improve module efficiency, reduce weight, and support electrified vehicle platforms. Expanding modular product portfolios that can be adapted across multiple vehicle architectures is a key strategy. Manufacturers are also forming long-term supply agreements with automakers to secure consistent demand. Enhancements in manufacturing automation and digital quality control systems are improving cost efficiency and scalability.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Module

- 2.2.5 Propulsion

- 2.2.6 Door

- 2.2.7 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising vehicle production volumes

- 3.2.1.3 Growth of electric and premium vehicles

- 3.2.1.4 Focus on modular vehicle architectures

- 3.2.1.5 Increasing safety and comfort features

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system integration complexity

- 3.2.2.2 Cost pressure on OEMs

- 3.2.3 Market opportunities

- 3.2.3.1 Lightweight material adoption

- 3.2.3.2 Smart door and access technologies

- 3.2.3.3 Expansion in emerging automotive markets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States Vehicle Safety

- 3.4.1.2 FMVSS Side Impact Standards

- 3.4.1.3 California Vehicle Compliance

- 3.4.1.4 Canada Vehicle Guidelines

- 3.4.2 Europe

- 3.4.2.1 EU Vehicle Standards

- 3.4.2.2 Euro NCAP Guidelines

- 3.4.2.3 National Compliance

- 3.4.2.4 EN Door Module Standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China Vehicle Regulations

- 3.4.3.2 India Safety Standards

- 3.4.3.3 Japan Module Guidelines

- 3.4.3.4 South Korea Standards

- 3.4.3.5 ASEAN Regional Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil Vehicle Standards

- 3.4.4.2 Argentina Compliance

- 3.4.4.3 Mexico Regulations

- 3.4.4.4 Regional Safety Guidelines

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Vehicle Standards

- 3.4.5.2 Saudi Arabia Regulations

- 3.4.5.3 South Africa Compliance

- 3.4.5.4 Regional Automotive Standards

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 OEM adoption & platform penetration analysis

- 3.14 Pricing, ASP & Cost Evolution

- 3.15 Impact of EV architectures on door module design

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Latches & handles

- 5.3 Window regulators

- 5.4 Speakers

- 5.5 Motors & actuators

- 5.6 Electrical connectors & wiring

- 5.7 Control units

- 5.8 Sealing systems

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUVs & crossovers

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCVs)

- 6.3.2 Medium Commercial Vehicles (MCVs)

- 6.3.3 Heavy Commercial Vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Module, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Manual door modules

- 7.3 Automated door modules

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 BEVs

- 8.4 Hybrid Vehicles

Chapter 9 Market Estimates & Forecast, By Door, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Front door modules

- 9.3 Rear door modules

- 9.4 Sliding door modules

- 9.5 Liftgate door modules

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Netherlands

- 11.3.9 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Turkey

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Aisin

- 12.1.2 Brose

- 12.1.3 Continental

- 12.1.4 Denso

- 12.1.5 Forvia

- 12.1.6 Hyundai Mobis

- 12.1.7 Magna International

- 12.1.8 Robert Bosch

- 12.1.9 Valeo

- 12.1.10 ZF Friedrichshafen

- 12.2 Regional Players

- 12.2.1 Flex-N-Gate

- 12.2.2 Grupo Antolin

- 12.2.3 Hi-Lex

- 12.2.4 Inteva Products

- 12.2.5 PHA Korea

- 12.3 Emerging Players/Disruptors

- 12.3.1 CIE Automotive

- 12.3.2 DaikyoNishikawa

- 12.3.3 Dura Automotive Systems

- 12.3.4 Hirotec

- 12.3.5 Kiekert

汽車門模組市場:按類型、門類型、組件、材料、應用和銷售管道分類-2026年至2032年全球市場預測汽車智慧門系統市場:依產品、技術、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測

汽車門模組市場:按類型、門類型、組件、材料、應用和銷售管道分類-2026年至2032年全球市場預測汽車智慧門系統市場:依產品、技術、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測 汽車門鉸鏈市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

汽車門鉸鏈市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 汽車外殼市場 - 全球產業規模、佔有率、趨勢、機會、預測:應用資訊、按組件、按類型、按地區和競爭對手分類,2021-2031 年汽車智慧門系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按技術、需求類別、車輛類型、地區和競爭格局分類,2021-2031年)車門控制模組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、車輛類型、銷售管道、地區和競爭格局分類,2021-2031年)

汽車外殼市場 - 全球產業規模、佔有率、趨勢、機會、預測:應用資訊、按組件、按類型、按地區和競爭對手分類,2021-2031 年汽車智慧門系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按技術、需求類別、車輛類型、地區和競爭格局分類,2021-2031年)車門控制模組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、車輛類型、銷售管道、地區和競爭格局分類,2021-2031年) 汽車側門防撞梁市場規模、佔有率及成長分析(按安裝位置、車輛類型、材質及地區分類)-2026-2033年產業預測

汽車側門防撞梁市場規模、佔有率及成長分析(按安裝位置、車輛類型、材質及地區分類)-2026-2033年產業預測 多用途汽車(MPV)電動滑動門系統:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

多用途汽車(MPV)電動滑動門系統:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 汽車用智慧型門系統的全球市場的評估:車輛類別,各元件類型,各技術類型,各地區,機會,預測(2018年~2032年)

汽車用智慧型門系統的全球市場的評估:車輛類別,各元件類型,各技術類型,各地區,機會,預測(2018年~2032年) 2032 年汽車門鉸鏈市場預測:按產品類型、材質、車輛類型、銷售管道、應用和地區進行的全球分析

2032 年汽車門鉸鏈市場預測:按產品類型、材質、車輛類型、銷售管道、應用和地區進行的全球分析