|

市場調查報告書

商品編碼

1928979

祛水器市場機會、成長要素、產業趨勢分析及2026年至2035年預測Steam Trap Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

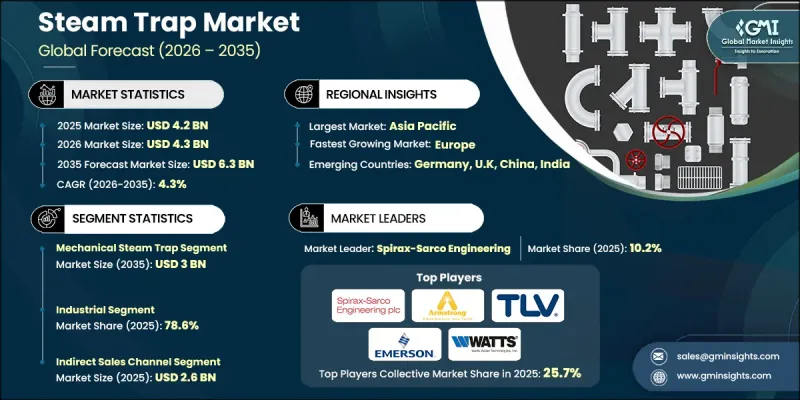

全球祛水器市場預計到 2025 年將達到 42 億美元,到 2035 年將達到 63 億美元,年複合成長率為 4.3%。

市場成長主要得益於節能技術的日益普及和工業蒸氣系統自動化程度的提升。祛水器在維持最佳蒸氣性能方面發揮關鍵作用,它能夠防止蒸氣網內的蒸氣損失並高效排出冷凝水。提高系統效率可直接轉化為減少能源浪費、降低營運成本和提高製程可靠性。對自動化監控和數據驅動型維護的日益重視正在變革時期蒸氣系統的管理方式,使操作人員能夠在最大限度地減少計劃外停機時間的同時提高系統性能。監管壓力和政策主導的節能措施不斷加速以先進解決方案取代傳統設備。提高蒸氣系統效率可降低10-15%的總能耗,進而提升安裝現代化蒸氣疏水閥的經濟價值。隨著各行業將永續性、營運最佳化和排放置於優先地位,蒸氣疏水閥仍然是各種工業環境中實現長期能源管理目標的關鍵組成部分。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 42億美元 |

| 預測金額 | 63億美元 |

| 複合年成長率 | 4.3% |

預計2025年,機械式祛水器的市場規模將達到19億美元,到2035年將達到30億美元。該細分市場憑藉其耐用性、運作可靠性和對嚴苛工業環境的適應性,保持著主導地位。這些疏水閥的設計旨在排放蒸氣的同時高效排出冷凝水,從而確保系統穩定運作。祛水器運作不當會導致高達20%的總蒸氣產量損失,凸顯了正確選擇和維護系統的重要性。

預計到2025年,工業應用將佔據78.6%的市場。這一領域的成長得益於嚴格的能源效率法規、對即時系統監控日益成長的需求以及預測性維護方法的廣泛應用。政府主導的永續性舉措也進一步推動了先進蒸氣管理解決方案在工業設施中的應用。

預計到2025年,美國蒸氣疏水閥市佔率將達到79.4%。強勁的工業現代化進程、高自動化普及率以及嚴格的能源效率標準持續推動市場需求。減少能源損耗和排放的持續努力也促使企業繼續投資先進的蒸氣疏水閥技術。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 對工業自動化和流程效率的需求日益成長

- 擴大製造業節能解決方案的應用

- 政府有關排放減排的法規

- 產業潛在風險與挑戰

- 較高的初始實施和維護成本

- 缺乏對蒸氣疏水閥維護的認知與專業知識

- 機會

- 擴展智慧和物聯網賦能的祛水器解決方案

- 工業發展和節能法規導致需求增加

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按類型

- 按地區

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 差距分析

- 風險評估與緩解

- 波特分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按類型分類的市場估算與預測,2022-2035年

- 機械式蒸氣疏水閥

- 動態蒸氣帶

- 恆溫蒸氣疏水閥

第6章 依功能分類的市場估計與預測,2022-2035年

- 蒸氣管道

- 冷凝油油回收

第7章 按材料分類的市場估算與預測,2022-2035年

- 鑄鐵/球墨鑄鐵

- 碳鋼

- 不銹鋼

- 合金/特殊鋼

第8章 市場估計與預測:依性別分類,2022-2035年

- 傳統的

- 智慧誘捕器/監測誘捕器

第9章 按應用領域分類的市場估算與預測,2022-2035年

- 住宅

- 商業的

- 工業的

第10章 依最終用途分類的市場估計與預測,2022-2035年

- 流程工業

- 發電

- 暖通空調和區域供暖

- 製藥和醫療保健

- 其他

第11章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接

第12章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- ARI-Armaturen

- Armstrong International

- Ayvaz

- Emerson Electric

- Forbes Marshall

- Hoffman Specialty

- Miura

- Miyawaki

- Spirax-Sarco Engineering

- Thermax

- TLV International

- Velan

- Watson-McDaniel

- Watts Water Technologies

- Yoshitake

The Global Steam Trap Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 6.3 billion by 2035.

Market expansion is driven by rising adoption of energy-efficient technologies and increased automation across industrial steam systems. Steam traps play a critical role in maintaining optimal steam performance by efficiently removing condensate while preventing steam loss within distribution networks. Improved system efficiency directly supports reduced energy waste, lower operating costs, and enhanced process reliability. Growing emphasis on automated monitoring and data-driven maintenance is reshaping how steam systems are managed, allowing operators to improve performance while minimizing unexpected downtime. Regulatory pressure and policy-driven energy conservation initiatives continue to accelerate the replacement of outdated equipment with advanced solutions. Efficiency improvements in steam systems can reduce overall energy consumption by 10% to 15%, reinforcing the economic value of modern steam trap deployment. As industries prioritize sustainability, operational optimization, and emissions reduction, steam traps remain essential components in achieving long-term energy management goals across a wide range of industrial environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 4.3% |

The mechanical steam traps generated USD 1.9 billion in 2025 and are projected to reach USD 3 billion by 2035. This segment maintains leadership due to its durability, operational reliability, and suitability for demanding industrial conditions. These traps are designed to discharge condensate efficiently while retaining steam, supporting consistent system performance. Inefficient steam trap operation can result in losses of up to 20% of total steam generation, highlighting the importance of proper system selection and maintenance.

The industrial applications accounted for 78.6% share in 2025. Growth in this segment is supported by stricter energy-efficiency regulations, increasing demand for real-time system monitoring, and wider adoption of predictive maintenance practices. Government-led sustainability initiatives further encourage the deployment of advanced steam management solutions across industrial facilities.

United States Steam Trap Market held 79.4% share in 2025. Strong industrial modernization efforts, high automation adoption, and rigorous efficiency standards continue to drive demand. Ongoing focus on reducing energy losses and emissions supports continued investment in advanced steam trap technologies.

Key companies operating in the Global Steam Trap Market include Armstrong International, Spirax-Sarco Engineering, Emerson Electric, Forbes Marshall, TLV International, ARI-Armaturen, Thermax, Ayvaz, Miura, Velan, Watson-McDaniel, Watts Water Technologies, Yoshitake, Miyawaki, and Hoffman Specialty. Companies active in the Steam Trap Market strengthen their competitive position through product innovation, digital integration, and service-oriented strategies. Investment in intelligent monitoring capabilities and predictive maintenance solutions enhances system reliability and customer value. Manufacturers focus on improving durability, efficiency, and ease of integration with automated control systems. Strategic partnerships with industrial operators and energy service providers support long-term adoption and recurring revenue. Geographic expansion into emerging industrial regions broadens market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Function

- 2.2.4 Material

- 2.2.5 Connectivity

- 2.2.6 Application

- 2.2.7 End use

- 2.2.8 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased industrial automation and process efficiency demands

- 3.2.1.2 Rising adoption of energy-efficient solutions in manufacturing

- 3.2.1.3 Government regulations on energy conservation and emissions reduction

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial installation and maintenance costs

- 3.2.2.2 Limited awareness and expertise in steam trap maintenance

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of smart & IoT-enabled steam trap solutions

- 3.2.3.2 Rising demand driven by industrial growth & energy-efficiency regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By type

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter';s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Mechanical steam trap

- 5.3 Thermodynamic steam strap

- 5.4 Thermostatic steam trap

Chapter 6 Market Estimates & Forecast, By Function, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Steam distribution

- 6.3 Condensate recovery

Chapter 7 Market Estimates & Forecast, By Material, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Cast/ductile iron

- 7.3 Carbon steel

- 7.4 Stainless steel

- 7.5 Alloy/specialty

Chapter 8 Market Estimates & Forecast, By Connectivity, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Conventional

- 8.3 Smart/monitored traps

Chapter 9 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By End Use, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Process industry

- 10.3 Power generation

- 10.4 HVAC & district heating

- 10.5 Pharmaceuticals & healthcare

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 France

- 12.3.3 UK

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 ARI-Armaturen

- 13.2 Armstrong International

- 13.3 Ayvaz

- 13.4 Emerson Electric

- 13.5 Forbes Marshall

- 13.6 Hoffman Specialty

- 13.7 Miura

- 13.8 Miyawaki

- 13.9 Spirax-Sarco Engineering

- 13.10 Thermax

- 13.11 TLV International

- 13.12 Velan

- 13.13 Watson-McDaniel

- 13.14 Watts Water Technologies

- 13.15 Yoshitake

2026年全球祛水器市場報告2026年全球祛水器監測市場報告

2026年全球祛水器市場報告2026年全球祛水器監測市場報告 蒸氣疏水閥市場規模、佔有率和成長分析(按類型、功能、材質、連接類型、應用、最終用途、通路和地區分類)—2026-2033年產業預測

蒸氣疏水閥市場規模、佔有率和成長分析(按類型、功能、材質、連接類型、應用、最終用途、通路和地區分類)—2026-2033年產業預測 蒸氣疏水閥市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品、應用、材質、產業、地區及競爭格局分類),2021-2031年

蒸氣疏水閥市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品、應用、材質、產業、地區及競爭格局分類),2021-2031年 祛水器市場-2025-2030年預測

祛水器市場-2025-2030年預測 祛水器市場(按技術類型、材料、連接、最終用途行業、分銷管道和應用)—2025-2030 年全球預測

祛水器市場(按技術類型、材料、連接、最終用途行業、分銷管道和應用)—2025-2030 年全球預測 全球祛水器市場 2025-2029

全球祛水器市場 2025-2029 全球祛水器市場:按產品類型、按連接、按閥體材質、按壓力、按尺寸、按應用、按最終用途行業、按地區 - 預測到 2029 年

全球祛水器市場:按產品類型、按連接、按閥體材質、按壓力、按尺寸、按應用、按最終用途行業、按地區 - 預測到 2029 年 全球蒸汽消音器市場(2024-2028)

全球蒸汽消音器市場(2024-2028) 祛水器市場規模、佔有率、趨勢分析報告:按產品、最終用途、按地區、細分市場預測,2024-2030 年

祛水器市場規模、佔有率、趨勢分析報告:按產品、最終用途、按地區、細分市場預測,2024-2030 年